What is Industrial Butt Fusion Machines - Global Market?

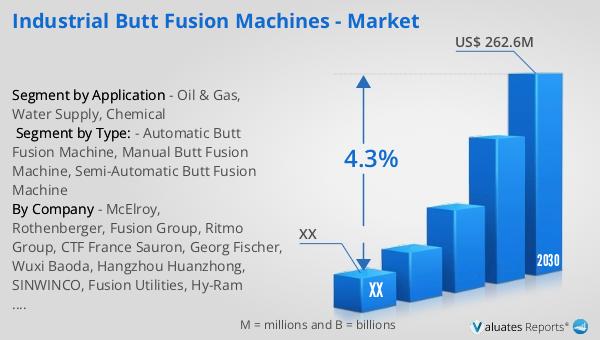

The global market for Industrial Butt Fusion Machines, a cornerstone in the infrastructure of various industries, is a dynamic and evolving sector. In 2023, it was valued at approximately US$ 194.9 million, showcasing the critical role these machines play in modern industrial applications. These devices are pivotal for the welding of thermoplastic pipes, a process essential in numerous sectors such as water supply, gas distribution, and chemical industries. The forecast for this market is optimistic, with expectations to reach around US$ 262.6 million by 2030, growing at a compound annual growth rate (CAGR) of 4.3% from 2024 to 2030. This growth trajectory is underpinned by the increasing demand for efficient and reliable pipe joining methods. Leading the charge in market dominance are companies like McElroy, Fusion Group, Rothenberger, and RITMO, which together have seized significant revenue shares, with McElroy at the forefront with a 22 percent share. Europe emerges as the largest market, holding about 32% of the global share, followed closely by Asia and North America. This geographical distribution underscores the widespread adoption and reliance on these machines across various global industries.

Automatic Butt Fusion Machine, Manual Butt Fusion Machine, Semi-Automatic Butt Fusion Machine in the Industrial Butt Fusion Machines - Global Market:

Diving into the specifics, the Industrial Butt Fusion Machines market is segmented into Automatic, Manual, and Semi-Automatic machines, each catering to distinct operational needs and efficiency levels. Automatic Butt Fusion Machines represent the pinnacle of convenience and precision, designed for operations requiring consistent and high-volume pipe welding with minimal human intervention. These machines are equipped with advanced technology that automates the welding process, ensuring high-quality joints and optimal productivity, making them a preferred choice for large-scale projects. On the other hand, Manual Butt Fusion Machines are tailored for environments where control and flexibility are paramount. These machines are operated manually, giving the operator direct control over the welding process. This allows for adjustments and fine-tuning in real-time, making it suitable for projects where precision and adaptability are crucial. Lastly, Semi-Automatic Butt Fusion Machines strike a balance between automation and manual control. They automate certain aspects of the welding process while allowing for human intervention when necessary. This hybrid approach combines the efficiency of automation with the precision of manual control, making these machines versatile and adaptable to a wide range of welding scenarios. Together, these three types of machines form a comprehensive portfolio that addresses the diverse needs of the global market, from high-volume industrial applications to specialized, custom projects.

Oil & Gas, Water Supply, Chemical in the Industrial Butt Fusion Machines - Global Market:

In the realm of Industrial Butt Fusion Machines, their application spans across critical sectors such as Oil & Gas, Water Supply, and Chemical industries, each with its unique demands and challenges. In the Oil & Gas sector, these machines are indispensable for creating durable and leak-proof pipelines, a necessity for the safe and efficient transport of oil and gas resources. The precision and reliability of butt fusion welding ensure that pipelines can withstand the harsh conditions and pressures encountered in this industry. Moving to the Water Supply sector, the role of Industrial Butt Fusion Machines is equally vital. They are used to join water pipes that deliver clean water to communities and dispose of wastewater, requiring joints that are both hygienic and robust to prevent leaks and contamination. Lastly, in the Chemical industry, the integrity of pipe welds is paramount. The pipes carry hazardous and corrosive substances, and any failure in the welding could lead to catastrophic leaks and environmental damage. Here, the high-quality welds produced by butt fusion machines are crucial for maintaining safety and operational efficiency. Across these sectors, the use of Industrial Butt Fusion Machines underscores their importance in building and maintaining the infrastructure that supports modern society.

Industrial Butt Fusion Machines - Global Market Outlook:

The outlook for the Industrial Butt Fusion Machines market is promising, with a projected growth from US$ 194.9 million in 2023 to US$ 262.6 million by 2030, reflecting a CAGR of 4.3% during the forecast period. This growth is indicative of the increasing reliance on these machines across various industries for their critical welding needs. The market is led by key players such as McElroy, Fusion Group, Rothenberger, and RITMO, with McElroy taking the lead with a significant 22 percent revenue share. Europe stands as the largest market, holding a 32% share, which is a testament to the region's robust industrial activities and the adoption of advanced welding technologies. Following Europe, Asia and North America are also significant markets, highlighting the global demand for efficient and reliable butt fusion welding solutions. This market outlook underscores the importance of Industrial Butt Fusion Machines in supporting the infrastructure needs of diverse industries worldwide, from oil and gas to water supply and chemical sectors, driving forward their growth and operational efficiency.

| Report Metric | Details |

| Report Name | Industrial Butt Fusion Machines - Market |

| Forecasted market size in 2030 | US$ 262.6 million |

| CAGR | 4.3% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | McElroy, Rothenberger, Fusion Group, Ritmo Group, CTF France Sauron, Georg Fischer, Wuxi Baoda, Hangzhou Huanzhong, SINWINCO, Fusion Utilities, Hy-Ram Engineering, Hiweld, Acuster Bahisa |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |