What is Global Cosmetic Grade Ubiquinone Market?

The Global Cosmetic Grade Ubiquinone Market is a specialized segment within the broader cosmetics industry, focusing on the use of ubiquinone, also known as Coenzyme Q10, in beauty and skincare products. Ubiquinone is a naturally occurring antioxidant found in the human body, playing a crucial role in cellular energy production and protection against oxidative damage. In the cosmetics industry, it is valued for its anti-aging properties, as it helps to reduce the appearance of fine lines and wrinkles, improve skin elasticity, and promote a youthful complexion. The market for cosmetic grade ubiquinone is driven by increasing consumer awareness of skincare benefits, a growing demand for anti-aging products, and advancements in formulation technologies. Manufacturers are focusing on developing high-quality, stable, and effective ubiquinone formulations to meet the rising consumer expectations. The market is characterized by a diverse range of products, including creams, lotions, serums, and other skincare formulations, catering to various skin types and concerns. As consumers continue to prioritize skincare and wellness, the demand for cosmetic grade ubiquinone is expected to grow, offering opportunities for innovation and expansion in the market.

Purity <98%, Purity 98%-99%, Purity >99% in the Global Cosmetic Grade Ubiquinone Market:

In the Global Cosmetic Grade Ubiquinone Market, the purity levels of ubiquinone play a significant role in determining the quality and efficacy of the final product. Purity levels are typically categorized into three main segments: Purity <98%, Purity 98%-99%, and Purity >99%. Each of these purity levels has distinct characteristics and applications within the cosmetics industry. Products with a purity of less than 98% are generally considered to be of lower quality, often containing impurities that can affect the stability and performance of the ubiquinone in cosmetic formulations. These products may be more affordable, but they may not deliver the same level of efficacy as higher purity options. On the other hand, ubiquinone with a purity level of 98%-99% is considered to be of high quality, offering a good balance between cost and performance. This level of purity ensures that the ubiquinone is effective in delivering its antioxidant and anti-aging benefits, making it a popular choice for mid-range cosmetic products. Finally, ubiquinone with a purity level greater than 99% is regarded as the highest quality available, often used in premium and luxury skincare products. This level of purity ensures maximum efficacy and stability, providing consumers with the best possible results. Manufacturers of cosmetic grade ubiquinone must carefully consider the purity level of their products, as it directly impacts the performance, cost, and consumer perception of the final product. As the demand for high-quality skincare products continues to grow, the importance of purity in ubiquinone formulations is expected to become increasingly significant.

Toner, Lotion, Serum, Sun Care, Others in the Global Cosmetic Grade Ubiquinone Market:

The Global Cosmetic Grade Ubiquinone Market finds its application in various skincare products, including toners, lotions, serums, sun care products, and others. In toners, ubiquinone is used for its antioxidant properties, helping to protect the skin from environmental damage and improve its overall appearance. Toners containing ubiquinone can help to balance the skin's pH levels, tighten pores, and prepare the skin for the application of other skincare products. In lotions, ubiquinone is valued for its ability to hydrate and nourish the skin, providing a smooth and supple texture. Lotions with ubiquinone can help to reduce the appearance of fine lines and wrinkles, making them a popular choice for anti-aging skincare routines. Serums, which are highly concentrated formulations, often contain ubiquinone for its potent anti-aging benefits. Ubiquinone in serums can penetrate deeply into the skin, delivering powerful antioxidants that help to combat free radicals and promote a youthful complexion. Sun care products also benefit from the inclusion of ubiquinone, as it helps to protect the skin from the harmful effects of UV radiation. By incorporating ubiquinone into sun care formulations, manufacturers can offer products that not only shield the skin from sun damage but also provide additional anti-aging benefits. Other skincare products, such as masks and eye creams, may also contain ubiquinone to enhance their efficacy and provide targeted benefits. As consumers continue to seek out effective and multifunctional skincare products, the use of ubiquinone in various formulations is expected to grow, offering opportunities for innovation and differentiation in the market.

Global Cosmetic Grade Ubiquinone Market Outlook:

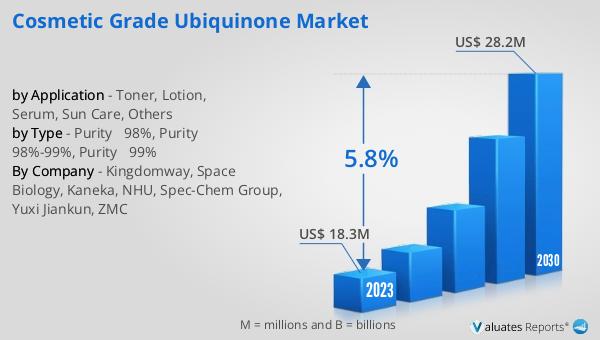

The outlook for the Global Cosmetic Grade Ubiquinone Market indicates a promising growth trajectory, with the market expected to expand from $20.1 million in 2024 to $29.7 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.8% from 2025 to 2031. This growth is driven by the increasing demand for anti-aging and skincare products, as well as the diverse applications of ubiquinone in various cosmetic formulations. The market is characterized by critical product segments, including different purity levels of ubiquinone, which cater to a wide range of consumer preferences and price points. However, the evolving U.S. tariff policies introduce an element of trade cost volatility and supply chain uncertainty, which could impact the market dynamics. Manufacturers and suppliers must navigate these challenges by optimizing their supply chains and exploring new markets to ensure continued growth. Despite these challenges, the market's potential for expansion remains strong, as consumers increasingly prioritize skincare and wellness. The growing awareness of the benefits of ubiquinone in cosmetic products is expected to drive demand, offering opportunities for innovation and differentiation in the market. As the market evolves, companies that can effectively address the challenges and capitalize on the opportunities are likely to succeed in this competitive landscape.

| Report Metric | Details |

| Report Name | Cosmetic Grade Ubiquinone Market |

| Accounted market size in 2024 | US$ 20.1 million |

| Forecasted market size in 2031 | US$ 29.7 million |

| CAGR | 5.8% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Kingdomway, Space Biology, Kaneka, NHU, Spec-Chem Group, Yuxi Jiankun, ZMC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |