What is Global Self-Adhesive Eyelashes Market?

The global self-adhesive eyelashes market is a dynamic and rapidly evolving segment within the beauty and cosmetics industry. These innovative eyelashes are designed to offer a convenient and hassle-free alternative to traditional false eyelashes, which typically require glue for application. Self-adhesive eyelashes come with a pre-applied adhesive strip, making them easy to apply and remove, thus appealing to consumers seeking quick and efficient beauty solutions. The market for these products is expanding as more people become aware of their benefits, including ease of use, time-saving application, and reduced risk of irritation from lash glue. Additionally, the growing trend of enhancing personal appearance and the increasing influence of social media beauty trends are driving demand. As a result, manufacturers are focusing on product innovation, offering a variety of styles, lengths, and materials to cater to diverse consumer preferences. This market is also witnessing increased competition, with both established brands and new entrants striving to capture market share by offering high-quality, affordable, and innovative products. The global self-adhesive eyelashes market is poised for significant growth as it continues to attract a broad consumer base seeking convenience and style in their beauty routines.

Simple Cluster, Multiple Cluster in the Global Self-Adhesive Eyelashes Market:

In the global self-adhesive eyelashes market, the concept of clustering can be understood through two primary types: simple clusters and multiple clusters. Simple clusters refer to a straightforward grouping of products or consumer segments based on specific characteristics or preferences. For instance, within the self-adhesive eyelashes market, a simple cluster might consist of consumers who prefer natural-looking lashes for everyday wear. This group is typically characterized by individuals who prioritize subtlety and ease of application, often opting for lashes that blend seamlessly with their natural lashes. These consumers are likely to be drawn to products that offer a natural appearance, are lightweight, and provide comfort for extended wear. On the other hand, multiple clusters involve a more complex segmentation of the market, taking into account a wider range of factors such as demographics, psychographics, and purchasing behavior. In the context of self-adhesive eyelashes, multiple clusters might include segments such as fashion-forward individuals who seek bold and dramatic lash styles for special occasions or social media influencers who require high-impact lashes for photo shoots and video content. These consumers are often willing to experiment with different styles, colors, and materials to achieve a standout look. Additionally, multiple clusters can also encompass regional preferences, where cultural influences and beauty standards play a significant role in shaping consumer choices. For example, in some regions, there may be a preference for fuller, more voluminous lashes, while in others, a more understated look might be favored. Understanding these clusters allows manufacturers and marketers to tailor their product offerings and marketing strategies to meet the specific needs and preferences of each segment. By doing so, they can effectively target their audience, enhance customer satisfaction, and ultimately drive sales growth. Furthermore, the use of data analytics and consumer insights is crucial in identifying and understanding these clusters, enabling companies to make informed decisions about product development, pricing, and distribution. As the self-adhesive eyelashes market continues to evolve, the ability to recognize and respond to these diverse consumer segments will be key to achieving success in this competitive landscape.

Online, Offline in the Global Self-Adhesive Eyelashes Market:

The usage of self-adhesive eyelashes in the global market can be categorized into two main areas: online and offline. In the online realm, e-commerce platforms have become a significant channel for the distribution and sale of self-adhesive eyelashes. The convenience of online shopping, coupled with the ability to reach a global audience, has made it an attractive option for both consumers and manufacturers. Online platforms offer a wide range of products, allowing consumers to easily compare different brands, styles, and prices. Additionally, the presence of customer reviews and ratings provides valuable insights into product quality and performance, aiding consumers in making informed purchasing decisions. Social media also plays a crucial role in the online market, with beauty influencers and makeup artists showcasing self-adhesive eyelashes in tutorials and reviews, thereby driving consumer interest and demand. On the other hand, the offline market for self-adhesive eyelashes primarily consists of brick-and-mortar retail stores, including beauty supply shops, department stores, and specialty cosmetics stores. These physical locations offer consumers the opportunity to see and feel the products before purchasing, which can be a significant advantage for those who prefer a tactile shopping experience. In-store promotions, product demonstrations, and personalized customer service further enhance the offline shopping experience, encouraging consumers to explore and purchase self-adhesive eyelashes. Moreover, offline channels often cater to impulse buyers who may not have initially intended to purchase eyelashes but are enticed by attractive displays and promotions. Despite the growing popularity of online shopping, the offline market remains a vital component of the self-adhesive eyelashes industry, particularly in regions where internet access is limited or where consumers prefer traditional shopping methods. Both online and offline channels have their unique advantages and challenges, and successful brands often adopt an omnichannel approach to maximize their reach and cater to diverse consumer preferences. By leveraging the strengths of each channel, companies can effectively engage with their target audience, build brand loyalty, and drive sales growth in the competitive self-adhesive eyelashes market.

Global Self-Adhesive Eyelashes Market Outlook:

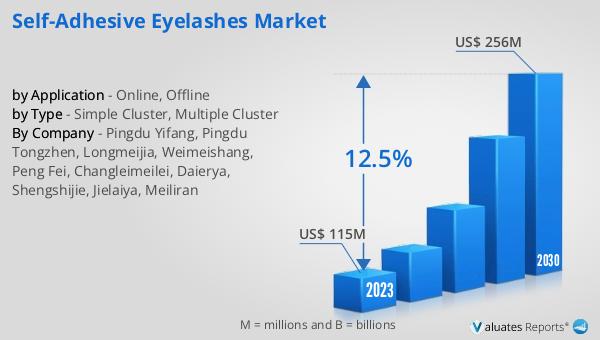

The outlook for the global self-adhesive eyelashes market indicates a promising trajectory, with expectations of growth from $127 million in 2024 to $285 million by 2031. This expansion is anticipated to occur at a compound annual growth rate (CAGR) of 12.5% between 2025 and 2031. The market's growth is largely driven by key product segments and a variety of end-use applications that cater to a broad spectrum of consumer needs. As consumers increasingly seek convenient and efficient beauty solutions, self-adhesive eyelashes are gaining popularity for their ease of use and time-saving benefits. However, the market is not without its challenges. Evolving U.S. tariff policies are introducing volatility in trade costs and creating uncertainty within the supply chain. These factors could potentially impact the pricing and availability of raw materials, thereby affecting production costs and profit margins for manufacturers. Despite these challenges, the market's growth prospects remain strong, as companies continue to innovate and adapt to changing consumer preferences and market conditions. By focusing on product development, strategic partnerships, and effective marketing strategies, businesses can navigate the complexities of the global self-adhesive eyelashes market and capitalize on the opportunities it presents.

| Report Metric | Details |

| Report Name | Self-Adhesive Eyelashes Market |

| Accounted market size in 2024 | US$ 127 million |

| Forecasted market size in 2031 | US$ 285 million |

| CAGR | 12.5% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Sales by Region |

|

| By Company | Pingdu Yifang, Pingdu Tongzhen, Longmeijia, Weimeishang, Peng Fei, Changleimeilei, Daierya, Shengshijie, Jielaiya, Meiliran |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |