What is Global Military Vehicle Intercom System Market?

The Global Military Vehicle Intercom System Market is a specialized segment within the defense industry that focuses on communication systems used in military vehicles. These intercom systems are crucial for ensuring seamless communication among crew members within a vehicle and with other units. They are designed to operate in harsh environments and under extreme conditions, providing reliable and secure communication channels. The market for these systems is driven by the increasing need for advanced communication solutions in military operations, as well as the modernization of military vehicles. With the rise in global defense budgets and the ongoing development of new military technologies, the demand for sophisticated intercom systems is expected to grow. These systems not only enhance operational efficiency but also improve situational awareness and safety for military personnel. As military operations become more complex and technology-driven, the role of intercom systems in ensuring effective communication and coordination becomes increasingly vital. The market is characterized by a mix of established players and new entrants, all striving to offer innovative solutions that meet the evolving needs of military forces worldwide.

Wired Vehicle Intercom System, Wireless Vehicle Intercom System in the Global Military Vehicle Intercom System Market:

The Global Military Vehicle Intercom System Market is broadly categorized into two main types: Wired Vehicle Intercom Systems and Wireless Vehicle Intercom Systems. Wired Vehicle Intercom Systems have been the traditional choice for military vehicles due to their reliability and robustness. These systems use physical cables to connect various communication devices within a vehicle, ensuring a stable and secure communication channel. They are less susceptible to interference and provide consistent performance even in challenging environments. However, the installation and maintenance of wired systems can be complex and time-consuming, especially in vehicles with intricate designs. On the other hand, Wireless Vehicle Intercom Systems offer greater flexibility and ease of installation. These systems use radio frequencies to transmit communication signals, eliminating the need for extensive cabling. This makes them ideal for modern military vehicles that require quick and easy integration of communication systems. Wireless systems also allow for greater mobility and adaptability, as they can be easily reconfigured to meet changing operational needs. However, they may be more susceptible to interference and require robust encryption to ensure secure communication. Despite these challenges, the demand for wireless systems is growing, driven by the need for more agile and adaptable communication solutions in modern military operations. Both wired and wireless intercom systems play a crucial role in enhancing communication and coordination within military vehicles, contributing to the overall effectiveness and efficiency of military operations.

Ground Vehicles, Air Vehicles, Watercraft Vehicles in the Global Military Vehicle Intercom System Market:

The usage of Global Military Vehicle Intercom Systems extends across various types of military vehicles, including Ground Vehicles, Air Vehicles, and Watercraft Vehicles. In Ground Vehicles, such as tanks, armored personnel carriers, and military trucks, intercom systems are essential for maintaining communication among crew members and coordinating with other units. These systems enable real-time information sharing, which is critical for making quick decisions in combat situations. They also enhance situational awareness by allowing crew members to communicate with external sources, such as command centers and other vehicles. In Air Vehicles, including helicopters and military transport aircraft, intercom systems facilitate communication between pilots, co-pilots, and other crew members. These systems are designed to operate effectively at high altitudes and in noisy environments, ensuring clear and uninterrupted communication. They also integrate with other avionics systems to provide comprehensive communication solutions for air operations. In Watercraft Vehicles, such as naval ships and submarines, intercom systems are vital for coordinating operations and ensuring the safety of crew members. These systems support communication between different sections of a vessel and with other ships and command centers. They are designed to withstand harsh maritime conditions and provide reliable communication channels in both surface and underwater operations. Overall, the use of intercom systems in military vehicles enhances operational efficiency, improves safety, and supports effective communication and coordination in various military operations.

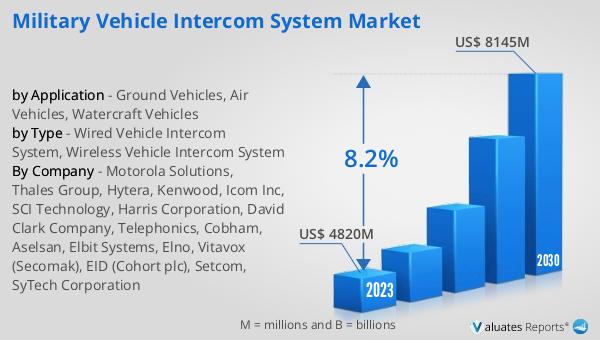

Global Military Vehicle Intercom System Market Outlook:

The outlook for the Global Military Vehicle Intercom System Market indicates significant growth, with projections showing an increase from $5,076 million in 2024 to $8,746 million by 2031, reflecting a compound annual growth rate (CAGR) of 8.2% from 2025 to 2031. This growth is driven by critical product segments and diverse end-use applications. However, evolving U.S. tariff policies introduce trade-cost volatility and supply-chain uncertainty, which could impact market dynamics. As of 2019, the wired vehicle intercom system segment dominates the market, contributing more than 90% of the total market share. The vehicle intercom system market is relatively concentrated, with key players including Motorola Solutions, Thales Group, Hytera, Kenwood, Icom Inc, SCI Technology, Harris Corporation, David Clark Company, Telephonics, Cobham, Aselsan, Elbit Systems, Elno, Vitavox (Secomak), EID (Cohort plc), Setcom, and SyTech Corporation. The revenue of the top ten manufacturers accounts for about 62% of the total revenue in 2019. These companies are focused on developing innovative solutions to meet the evolving needs of military forces worldwide, ensuring reliable and secure communication in various operational environments.

| Report Metric | Details |

| Report Name | Military Vehicle Intercom System Market |

| Accounted market size in 2024 | US$ 5076 in million |

| Forecasted market size in 2031 | US$ 8746 million |

| CAGR | 8.2% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | Motorola Solutions, Thales Group, Hytera, Kenwood, Icom Inc, SCI Technology, Harris Corporation, David Clark Company, Telephonics, Cobham, Aselsan, Elbit Systems, Elno, Vitavox (Secomak), EID (Cohort plc), Setcom, SyTech Corporation |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |