What is Global Rock Drilling Jumbo Market?

The Global Rock Drilling Jumbo Market is a specialized segment within the construction and mining equipment industry, focusing on machines designed for drilling holes in rock formations. These machines, known as rock drilling jumbos, are essential for creating tunnels, mining operations, and other large-scale construction projects. They are equipped with one or more arms that hold the drilling equipment, allowing for precise and efficient drilling in various rock types. The market for these machines is driven by the increasing demand for infrastructure development, mining activities, and the need for efficient and safe drilling solutions. As urbanization and industrialization continue to expand globally, the demand for rock drilling jumbos is expected to grow, providing opportunities for manufacturers and suppliers in this niche market. The market is characterized by technological advancements, with manufacturers focusing on developing more efficient, automated, and environmentally friendly machines to meet the evolving needs of the industry.

Single Arm Rock Drilling Jumbo, Double Arm Rock Drilling Jumbo, Multi Arm Rock Drilling Jumbo in the Global Rock Drilling Jumbo Market:

In the Global Rock Drilling Jumbo Market, there are different types of machines designed to cater to various drilling needs, primarily categorized into Single Arm, Double Arm, and Multi Arm Rock Drilling Jumbos. Single Arm Rock Drilling Jumbos are typically used in smaller projects or where space is limited. These machines are equipped with one drilling arm, making them ideal for narrow tunnels or smaller mining operations. They offer the advantage of being more maneuverable and easier to operate in confined spaces, which can be crucial in certain construction or mining environments. Despite their smaller size, they are built to deliver precise and efficient drilling, ensuring that even the most challenging rock formations can be penetrated effectively. On the other hand, Double Arm Rock Drilling Jumbos are designed for larger projects that require more extensive drilling capabilities. With two arms, these machines can cover a larger area in a shorter amount of time, making them suitable for medium to large-scale mining operations or tunnel construction projects. The dual arms allow for simultaneous drilling, which significantly enhances productivity and reduces the time required to complete a project. This type of jumbo is often favored in projects where time efficiency and increased output are critical. Multi Arm Rock Drilling Jumbos represent the pinnacle of drilling technology, designed for the most demanding and large-scale projects. These machines are equipped with multiple drilling arms, allowing them to tackle extensive drilling tasks with unmatched efficiency. They are commonly used in massive infrastructure projects, such as the construction of large tunnels for railways or highways, where the scale of the project demands high productivity and precision. The multiple arms enable these jumbos to perform complex drilling patterns and cover vast areas quickly, making them indispensable in projects where time and precision are of the essence. The choice between Single Arm, Double Arm, and Multi Arm Rock Drilling Jumbos depends largely on the specific requirements of the project, including the scale, complexity, and the type of rock formations involved. Each type of jumbo offers unique advantages, and understanding these can help project managers and engineers select the most appropriate machine for their needs. As the Global Rock Drilling Jumbo Market continues to evolve, manufacturers are focusing on enhancing the capabilities of these machines, incorporating advanced technologies such as automation, remote control, and data analytics to improve efficiency, safety, and environmental sustainability.

Mining, Railway and Highway Construction, Other in the Global Rock Drilling Jumbo Market:

The Global Rock Drilling Jumbo Market finds its applications in various sectors, including mining, railway and highway construction, and other infrastructure projects. In the mining industry, rock drilling jumbos are indispensable tools for extracting minerals and ores from the earth. They are used to drill precise holes in rock formations, which are then filled with explosives to break the rock apart, allowing for the extraction of valuable resources. The efficiency and precision of rock drilling jumbos make them essential for modern mining operations, where safety and productivity are paramount. These machines are designed to operate in harsh and challenging environments, ensuring that mining companies can maximize their output while minimizing risks to workers. In railway and highway construction, rock drilling jumbos play a crucial role in the creation of tunnels and other underground structures. As urban areas expand and the demand for efficient transportation networks increases, the need for tunnels to accommodate railways and highways has grown significantly. Rock drilling jumbos are used to drill the initial holes required for tunnel construction, providing the foundation for these critical infrastructure projects. Their ability to drill through various rock types with precision and speed makes them invaluable in ensuring that projects are completed on time and within budget. Additionally, the use of rock drilling jumbos in these projects helps to minimize the environmental impact of construction activities, as they allow for more controlled and efficient drilling processes. Beyond mining and transportation infrastructure, rock drilling jumbos are also used in other construction projects that require precise and efficient drilling capabilities. This includes the construction of underground facilities, such as storage spaces, water reservoirs, and utility tunnels. The versatility of rock drilling jumbos makes them suitable for a wide range of applications, providing construction companies with the tools they need to tackle complex projects with confidence. As the demand for infrastructure development continues to rise globally, the role of rock drilling jumbos in facilitating these projects is expected to grow, driving further innovation and advancements in the market.

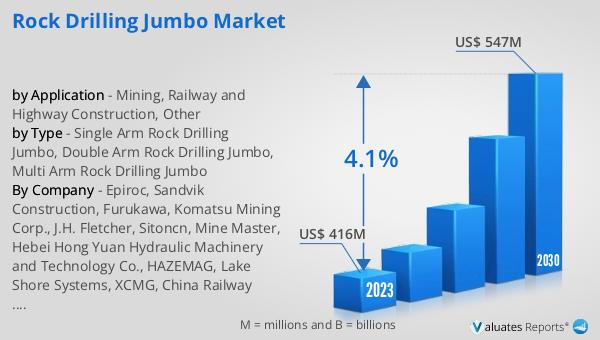

Global Rock Drilling Jumbo Market Outlook:

In 2024, the global market size for Rock Drilling Jumbos was valued at approximately US$ 431 million, with projections indicating a growth to around US$ 567 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.1% during the forecast period from 2025 to 2031. In 2023, the market size was recorded at US$415.71 million, with expectations to reach US$546.91 million by 2030, reflecting a CAGR of 4.05%. The market is dominated by the top five manufacturers, who collectively hold about 56% of the market share. This indicates a competitive landscape where a few key players have significant influence over market trends and developments. The steady growth in the market size reflects the increasing demand for efficient and advanced rock drilling solutions across various industries, including mining, construction, and infrastructure development. As these sectors continue to expand, the need for reliable and high-performance rock drilling jumbos is expected to drive further growth in the market. The focus on technological advancements and the development of more sustainable and automated drilling solutions are likely to play a crucial role in shaping the future of the Global Rock Drilling Jumbo Market.

| Report Metric | Details |

| Report Name | Rock Drilling Jumbo Market |

| CAGR | 4.1% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Epiroc, Sandvik Construction, Furukawa, Komatsu Mining Corp., J.H. Fletcher, Sitoncn, Mine Master, Hebei Hong Yuan Hydraulic Machinery and Technology Co., HAZEMAG, Lake Shore Systems, XCMG, China Railway Engineering Equipment Group Co., Ltd., Zhangjiakou Xuanhua Huatai Mining&Metallurgical Machinery Co., Ltd., Shandong China Coal Industrial&Mining Supplies Group Co.,Ltd, Cocental - CMM, Sichuan Zuanshen Intelligent Machinery Manufacturing Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |