What is Global Duckbill Valves Market?

The Global Duckbill Valves Market is a specialized segment within the broader industrial valves industry, focusing on a unique type of valve known for its flexible, rubber-like construction. These valves are designed to allow fluid to flow in one direction while preventing backflow, making them essential in various applications where maintaining a unidirectional flow is crucial. The market for duckbill valves is driven by their versatility and efficiency in handling different types of fluids, including water, sewage, and chemicals. They are particularly valued for their ability to operate without the need for mechanical parts, which reduces maintenance requirements and enhances reliability. The global market for these valves is expanding as industries seek cost-effective and durable solutions for fluid control. With increasing urbanization and industrialization, the demand for efficient drainage and wastewater management systems is on the rise, further propelling the growth of the duckbill valves market. As environmental regulations become more stringent, the need for effective and sustainable fluid management solutions is expected to drive further innovation and adoption of duckbill valves across various sectors.

Flanged Type Duckbill Valves, Slip-on Type Duckbill Valves, Others in the Global Duckbill Valves Market:

Flanged Type Duckbill Valves are a prominent category within the Global Duckbill Valves Market, known for their robust design and ease of installation. These valves feature a flange that allows them to be bolted directly to a pipeline, providing a secure and leak-proof connection. This design makes them ideal for applications where a strong and reliable seal is necessary, such as in municipal water systems and industrial processes. The flanged type is particularly favored in scenarios where the valve needs to be frequently inspected or replaced, as the flange allows for easy removal and reinstallation. Slip-on Type Duckbill Valves, on the other hand, offer a more flexible installation option. These valves are designed to slip over the end of a pipe and are secured with clamps or bands. This design is advantageous in situations where space is limited or where the pipeline configuration does not allow for the use of flanged connections. Slip-on valves are often used in temporary or emergency applications due to their ease of installation and removal. They are also a cost-effective solution for systems that require frequent changes or adjustments. Other types of duckbill valves in the market include inline and custom-designed valves, which cater to specific industry needs. Inline duckbill valves are integrated directly into the pipeline, providing a seamless flow path and minimizing potential leak points. Custom-designed valves are tailored to meet unique application requirements, offering solutions for challenging environments or specialized fluid control needs. The diversity of duckbill valve types reflects the wide range of applications and industries that rely on these versatile components. From water treatment facilities to chemical processing plants, duckbill valves play a critical role in ensuring efficient and reliable fluid management. As industries continue to evolve and face new challenges, the demand for innovative and adaptable valve solutions is expected to grow, driving further advancements in the design and functionality of duckbill valves.

Municipal Drainage, Dam Drainage, Wastewater Treatment Plant Drainage, Others in the Global Duckbill Valves Market:

The usage of Global Duckbill Valves Market in municipal drainage systems is a testament to their effectiveness in managing large volumes of water and preventing backflow. In urban areas, where stormwater and sewage systems are often interconnected, duckbill valves are essential in preventing the reverse flow of contaminated water into clean water supplies. Their ability to handle varying flow rates and pressures makes them ideal for municipal applications, where conditions can change rapidly during heavy rainfall or flooding events. In dam drainage systems, duckbill valves play a crucial role in maintaining the structural integrity of the dam by allowing controlled release of water while preventing backflow that could compromise the dam's stability. Their robust construction and ability to withstand harsh environmental conditions make them a reliable choice for such critical applications. In wastewater treatment plants, duckbill valves are used to manage the flow of treated and untreated water, ensuring that effluent is discharged safely and efficiently. Their resistance to corrosion and ability to handle abrasive materials make them well-suited for the challenging conditions often found in wastewater treatment processes. Other applications of duckbill valves include industrial processes where precise fluid control is necessary, such as in chemical manufacturing or food processing. In these settings, the valves' ability to provide a tight seal and prevent contamination is crucial for maintaining product quality and safety. The versatility and reliability of duckbill valves make them an indispensable component in a wide range of fluid management systems, contributing to their growing popularity in the global market. As industries continue to prioritize efficiency and sustainability, the demand for innovative valve solutions like duckbill valves is expected to increase, driving further growth and development in this dynamic market.

Global Duckbill Valves Market Outlook:

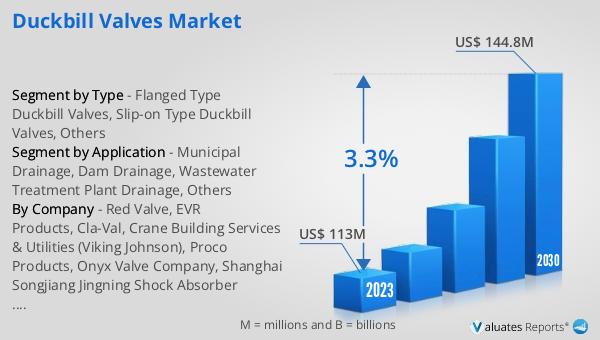

The global market for Duckbill Valves was valued at $123 million in 2024 and is anticipated to expand to a revised size of $154 million by 2031, reflecting a compound annual growth rate (CAGR) of 3.3% over the forecast period. The market is characterized by a significant concentration, with the top four manufacturers collectively holding a market share exceeding 40%. North America emerges as the leading producer of duckbill valves, accounting for over 40% of the market share, followed by Europe, China, and Japan. In terms of product segmentation, Flanged Type Duckbill Valves dominate the market, representing a substantial 50% share of the global duckbill valves market. This dominance can be attributed to their robust design and ease of installation, making them a preferred choice in various industrial and municipal applications. The market dynamics are influenced by factors such as increasing urbanization, industrialization, and the growing need for efficient fluid management systems. As industries continue to seek cost-effective and reliable solutions for fluid control, the demand for duckbill valves is expected to rise, driving further innovation and growth in this sector. The market outlook suggests a positive trajectory for the duckbill valves market, with opportunities for expansion and development in emerging markets and industries.

| Report Metric | Details |

| Report Name | Duckbill Valves Market |

| Accounted market size in year | US$ 123 million |

| Forecasted market size in 2031 | US$ 154 million |

| CAGR | 3.3% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Red Valve, EVR Products, Cla-Val, Crane Building Services & Utilities (Viking Johnson), Proco Products, Onyx Valve Company, Shanghai Songjiang Jingning Shock Absorber Co.,Ltd., J & S Valve, General Rubber (Flex-Valve), HiwaFlex, Jindex Pty Ltd, Prime Composites |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |