What is Global Potassium Metabisulfite Sales Market?

The Global Potassium Metabisulfite Sales Market refers to the worldwide trade and distribution of potassium metabisulfite, a chemical compound widely used as a preservative and antioxidant. This market encompasses the production, sales, and consumption of potassium metabisulfite across various regions and industries. Potassium metabisulfite is primarily used in the food and beverage industry, particularly in winemaking and brewing, to prevent oxidation and preserve the freshness of products. It is also utilized in the textile industry for dyeing and printing processes, as well as in the pharmaceutical sector for its antioxidant properties. The market is driven by the increasing demand for processed and packaged foods, as well as the growing popularity of wine and beer consumption globally. Additionally, the expanding textile and pharmaceutical industries contribute to the market's growth. The market is characterized by the presence of several key players who compete based on product quality, pricing, and distribution networks. Overall, the Global Potassium Metabisulfite Sales Market plays a crucial role in supporting various industries by providing a reliable and effective solution for preservation and antioxidant needs.

in the Global Potassium Metabisulfite Sales Market:

Potassium metabisulfite is available in various types, each catering to the specific needs of different customers in the Global Potassium Metabisulfite Sales Market. One of the most common types is food-grade potassium metabisulfite, which is extensively used in the food and beverage industry. This type is preferred for its high purity and effectiveness in preserving the quality and freshness of food products. It is particularly popular in winemaking, where it helps prevent oxidation and spoilage, ensuring the wine retains its intended flavor and aroma. Another type is industrial-grade potassium metabisulfite, which is used in various industrial applications such as textile processing, water treatment, and chemical manufacturing. This type is valued for its ability to act as a reducing agent and its effectiveness in removing excess chlorine from water. Additionally, pharmaceutical-grade potassium metabisulfite is used in the pharmaceutical industry for its antioxidant properties, helping to stabilize and preserve the efficacy of certain medications. The choice of potassium metabisulfite type depends on the specific requirements of the application and the industry in which it is used. Customers in the food and beverage industry prioritize food-grade potassium metabisulfite for its safety and compliance with regulatory standards. In contrast, industrial customers may opt for industrial-grade potassium metabisulfite for its cost-effectiveness and suitability for large-scale applications. The pharmaceutical industry, on the other hand, demands high-purity pharmaceutical-grade potassium metabisulfite to ensure the safety and effectiveness of their products. The availability of different types of potassium metabisulfite allows customers to select the most appropriate option for their specific needs, ensuring optimal performance and results. The market for potassium metabisulfite is highly competitive, with manufacturers focusing on product innovation and quality to meet the diverse demands of customers. As the demand for processed foods, beverages, and pharmaceuticals continues to rise, the market for potassium metabisulfite is expected to grow, driven by the need for effective preservation and antioxidant solutions. Overall, the availability of various types of potassium metabisulfite caters to the diverse needs of customers across different industries, ensuring the continued growth and success of the Global Potassium Metabisulfite Sales Market.

in the Global Potassium Metabisulfite Sales Market:

Potassium metabisulfite finds applications in a wide range of industries, each benefiting from its unique properties and effectiveness. In the food and beverage industry, potassium metabisulfite is primarily used as a preservative and antioxidant. It is commonly added to wines and beers to prevent oxidation and spoilage, ensuring the products maintain their intended flavor and aroma. The compound is also used in the preservation of dried fruits, juices, and other processed foods, helping to extend their shelf life and maintain their quality. In the textile industry, potassium metabisulfite is used in dyeing and printing processes. It acts as a reducing agent, helping to remove excess dye and improve the colorfastness of fabrics. The compound is also used in the bleaching of wool and silk, ensuring the fibers retain their natural softness and luster. In the water treatment industry, potassium metabisulfite is used to remove excess chlorine from water, making it safe for consumption and use in various applications. The compound is also used in the treatment of wastewater, helping to reduce the environmental impact of industrial processes. In the pharmaceutical industry, potassium metabisulfite is used for its antioxidant properties. It helps stabilize and preserve the efficacy of certain medications, ensuring they remain effective throughout their shelf life. The compound is also used in the production of certain vitamins and supplements, helping to maintain their potency and effectiveness. Overall, the diverse applications of potassium metabisulfite highlight its versatility and importance in various industries. Its ability to act as a preservative, antioxidant, and reducing agent makes it a valuable component in the production and preservation of a wide range of products. As the demand for processed foods, beverages, textiles, and pharmaceuticals continues to grow, the applications of potassium metabisulfite are expected to expand, driving the growth of the Global Potassium Metabisulfite Sales Market.

Global Potassium Metabisulfite Sales Market Outlook:

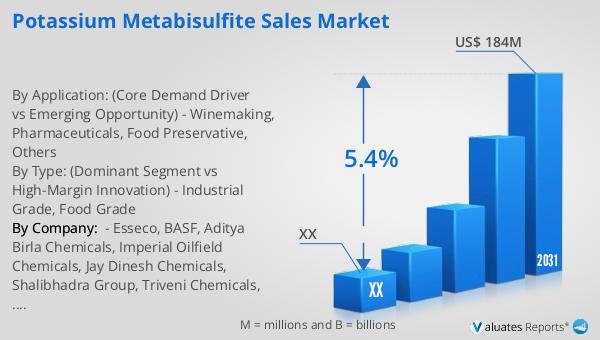

In 2024, the global market for Potassium Metabisulfite was valued at approximately $128 million. Projections indicate that by 2031, this market is expected to grow to a revised size of around $184 million, reflecting a compound annual growth rate (CAGR) of 5.4% during the forecast period from 2025 to 2031. This growth is indicative of the increasing demand for potassium metabisulfite across various industries, driven by its effectiveness as a preservative and antioxidant. Notably, the top five manufacturers in the global market hold a significant share, collectively accounting for over 60% of the market. This concentration of market share among leading manufacturers underscores the competitive nature of the industry, where companies strive to maintain their dominance through product innovation and strategic partnerships. In terms of product segmentation, food-grade potassium metabisulfite emerges as the largest segment, commanding a substantial share of approximately 80%. This dominance is attributed to the widespread use of food-grade potassium metabisulfite in the food and beverage industry, where it is valued for its high purity and compliance with regulatory standards. The market outlook for potassium metabisulfite reflects the growing importance of this compound in supporting various industries, ensuring the preservation and quality of products, and meeting the evolving needs of consumers.

| Report Metric | Details |

| Report Name | Potassium Metabisulfite Sales Market |

| Forecasted market size in 2031 | US$ 184 million |

| CAGR | 5.4% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Esseco, BASF, Aditya Birla Chemicals, Imperial Oilfield Chemicals, Jay Dinesh Chemicals, Shalibhadra Group, Triveni Chemicals, Shakti Chemicals, Ultramarines India, Advance Chemical Sales, Ram-Nath & Co., Pat Impex, Shandong Minde Chemical, Zibo Baida Chemical |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |