What is Global Car Navigation Sales Market?

The global car navigation sales market is a dynamic and rapidly evolving sector that plays a crucial role in the automotive industry. This market encompasses the production, distribution, and sale of car navigation systems, which are essential tools for modern drivers. These systems provide real-time directions, traffic updates, and other location-based services, enhancing the driving experience and improving road safety. The market is driven by technological advancements, increasing consumer demand for advanced in-car technologies, and the growing trend of connected vehicles. As more consumers prioritize convenience and safety, the demand for sophisticated navigation systems continues to rise. Additionally, the integration of features such as voice recognition, real-time traffic data, and connectivity with smartphones has further fueled the market's growth. The global car navigation sales market is characterized by intense competition among manufacturers, with companies constantly innovating to offer more advanced and user-friendly products. As a result, the market is expected to witness significant growth in the coming years, driven by the increasing adoption of these systems in both new and existing vehicles.

in the Global Car Navigation Sales Market:

The global car navigation sales market caters to a diverse range of customers, each with unique preferences and requirements. One of the most popular types of car navigation systems is the built-in or factory-installed system. These systems are integrated into the vehicle's dashboard and are often included as a standard feature in many new cars. They offer seamless integration with the car's other systems, such as audio and climate control, providing a cohesive user experience. Built-in systems are favored by customers who prioritize convenience and are willing to invest in a vehicle with advanced features. Another type is the portable navigation device (PND), which is a standalone unit that can be easily mounted on the dashboard or windshield. PNDs are popular among customers who prefer a cost-effective solution that can be transferred between vehicles. They offer flexibility and are often equipped with features such as touchscreens, voice guidance, and real-time traffic updates. Additionally, smartphone-based navigation apps have gained significant popularity in recent years. These apps, such as Google Maps and Waze, offer a convenient and affordable alternative to traditional navigation systems. They leverage the smartphone's GPS capabilities and provide real-time traffic information, route optimization, and other features. Customers who prefer smartphone-based navigation appreciate the familiarity and ease of use, as well as the ability to receive regular updates and new features. Another emerging type of car navigation system is the aftermarket in-dash navigation system. These systems are installed in vehicles that did not come with a factory-installed navigation system. They offer similar features to built-in systems and are often chosen by customers who want to upgrade their existing vehicles with modern technology. Aftermarket systems provide a cost-effective way to enhance a vehicle's capabilities without purchasing a new car. Furthermore, some customers opt for hybrid navigation systems, which combine the features of built-in and portable systems. These systems offer the convenience of a factory-installed system with the flexibility of a portable device. They are particularly popular among customers who frequently travel and require a reliable navigation solution that can be used in multiple vehicles. In addition to these types, there are also specialized navigation systems designed for specific customer segments. For example, fleet management systems are tailored for businesses that operate a large number of vehicles. These systems provide advanced features such as vehicle tracking, route optimization, and driver behavior monitoring, helping businesses improve efficiency and reduce operational costs. Similarly, navigation systems for commercial vehicles, such as trucks and buses, are designed to meet the unique needs of these vehicles, offering features such as route planning for oversized loads and compliance with transportation regulations. Overall, the global car navigation sales market offers a wide range of options to cater to the diverse needs of customers. Whether it's a built-in system for a new car, a portable device for flexibility, or a smartphone app for convenience, there is a navigation solution for every type of driver.

in the Global Car Navigation Sales Market:

The global car navigation sales market serves a variety of applications, each designed to enhance the driving experience and improve road safety. One of the primary applications is in passenger vehicles, where navigation systems provide drivers with real-time directions, traffic updates, and points of interest. These systems help drivers navigate unfamiliar areas, avoid traffic congestion, and find the quickest routes to their destinations. In addition to providing directions, navigation systems in passenger vehicles often include features such as voice recognition, Bluetooth connectivity, and integration with other in-car systems, offering a seamless and convenient user experience. Another significant application of car navigation systems is in commercial vehicles, such as trucks and buses. These systems are designed to meet the specific needs of commercial drivers, offering features such as route planning for oversized loads, compliance with transportation regulations, and vehicle tracking. By providing accurate and up-to-date information, navigation systems help commercial drivers optimize their routes, reduce fuel consumption, and improve overall efficiency. Additionally, navigation systems in commercial vehicles often include features such as driver behavior monitoring and fleet management tools, enabling businesses to enhance their operations and reduce costs. Car navigation systems are also widely used in rental vehicles, providing renters with a convenient and reliable way to navigate unfamiliar areas. Rental companies often equip their vehicles with portable navigation devices or offer smartphone-based navigation apps to enhance the customer experience. These systems help renters find their way around new cities, locate points of interest, and avoid getting lost, ultimately improving customer satisfaction. Furthermore, navigation systems are increasingly being integrated into electric vehicles (EVs), where they play a crucial role in managing range anxiety and optimizing charging. EV navigation systems provide drivers with information on charging station locations, availability, and compatibility, helping them plan their routes and ensure they have enough charge to reach their destinations. By offering real-time data on charging infrastructure, these systems help alleviate range anxiety and encourage the adoption of electric vehicles. In addition to these applications, car navigation systems are also used in emergency vehicles, such as ambulances and fire trucks, where they provide critical information to first responders. These systems offer features such as real-time traffic updates, route optimization, and integration with dispatch systems, enabling emergency personnel to reach their destinations quickly and efficiently. By providing accurate and timely information, navigation systems help improve response times and enhance public safety. Overall, the global car navigation sales market offers a wide range of applications that cater to the diverse needs of drivers and businesses. Whether it's providing directions in passenger vehicles, optimizing routes in commercial vehicles, or enhancing the customer experience in rental cars, navigation systems play a vital role in modern transportation.

Global Car Navigation Sales Market Outlook:

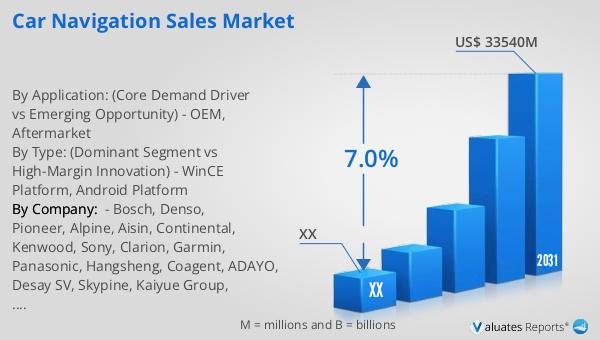

In 2024, the global car navigation market was valued at approximately $21,020 million. Looking ahead, it is projected to grow to an estimated $33,540 million by 2031, reflecting a compound annual growth rate (CAGR) of 7.0% during the forecast period from 2025 to 2031. This growth is indicative of the increasing demand for advanced navigation systems across the globe. The market is dominated by the top four manufacturers, who collectively hold about 35% of the market share. This concentration of market power highlights the competitive nature of the industry, with leading companies continuously innovating to maintain their positions. Among the various product segments, the Android platform stands out as the largest, accounting for over 50% of the market share. This dominance can be attributed to the widespread adoption of Android-based systems, which offer a user-friendly interface, extensive app compatibility, and regular updates. The preference for Android platforms is driven by their ability to integrate seamlessly with other devices and services, providing a comprehensive and connected user experience. As the market continues to evolve, manufacturers are likely to focus on enhancing the capabilities of Android-based systems, further solidifying their position as the leading segment in the global car navigation market.

| Report Metric | Details |

| Report Name | Car Navigation Sales Market |

| Forecasted market size in 2031 | US$ 33540 million |

| CAGR | 7.0% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Bosch, Denso, Pioneer, Alpine, Aisin, Continental, Kenwood, Sony, Clarion, Garmin, Panasonic, Hangsheng, Coagent, ADAYO, Desay SV, Skypine, Kaiyue Group, Roadrover, FlyAudio, Soling |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |