What is Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market?

The Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market is a specialized segment within the broader MDF industry, focusing on panels that are treated with fire-retardant chemicals to enhance their resistance to fire. These panels are engineered to slow down the spread of flames and reduce smoke production, making them a safer choice for construction and interior applications where fire safety is a priority. The market for these panels is driven by stringent building codes and regulations that mandate the use of fire-retardant materials in certain types of buildings, such as public and commercial structures. Additionally, the growing awareness of fire safety among consumers and builders has contributed to the increased demand for these panels. The market is characterized by a variety of products that differ in thickness, density, and fire-retardant properties, catering to diverse applications and customer needs. Manufacturers in this market are continually innovating to improve the performance and sustainability of their products, often incorporating eco-friendly materials and processes. As urbanization and construction activities continue to rise globally, the demand for fire-retardant MDF panels is expected to grow, offering opportunities for both established players and new entrants in the market.

Thickness: 6mm, Thickness: 9mm, Thickness: 12mm, Thickness: 15mm, Thickness: 18mm, Thickness: 25mm, Other in the Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market:

When it comes to the Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market, thickness plays a crucial role in determining the suitability of panels for various applications. Starting with the 6mm thickness, these panels are typically used in applications where lightweight and flexibility are essential. They are ideal for decorative purposes, such as wall paneling and furniture components, where the primary requirement is not structural strength but rather aesthetic appeal and ease of installation. Moving up to the 9mm thickness, these panels offer a bit more rigidity and are often used in applications that require a balance between weight and strength. They are suitable for use in cabinetry, shelving, and partitions, providing a good compromise between durability and ease of handling. The 12mm thickness panels are more robust and are commonly used in applications that demand greater structural integrity, such as flooring underlayment and more substantial furniture pieces. These panels provide a solid base while still being relatively easy to work with. At 15mm thickness, the panels are even sturdier and are often employed in more demanding applications, such as load-bearing furniture and structural components in buildings. They offer enhanced strength and stability, making them suitable for use in areas where durability is a primary concern. The 18mm thickness panels are among the most commonly used in construction and furniture manufacturing, offering a high level of strength and versatility. They are ideal for use in heavy-duty furniture, countertops, and other applications where a robust and reliable material is required. Finally, the 25mm thickness panels are the thickest and most durable, often used in specialized applications that require maximum strength and fire resistance. These panels are suitable for use in industrial settings, heavy-duty construction projects, and other areas where the highest level of performance is necessary. In addition to these standard thicknesses, the market also offers other thickness options to cater to specific customer needs and applications. Manufacturers continue to innovate and develop new products to meet the evolving demands of the market, ensuring that there is a suitable fire-retardant MDF panel for every application.

Public Buildings, Commercial Buildings in the Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market:

The usage of Global Fire Retardant Medium Density Fiberboard (MDF) Panels in public buildings is primarily driven by the need for enhanced fire safety and compliance with building codes and regulations. Public buildings, such as schools, hospitals, and government offices, are often subject to stringent fire safety standards to protect occupants and minimize the risk of fire-related incidents. Fire retardant MDF panels are an ideal choice for these settings, as they provide an added layer of protection by slowing down the spread of flames and reducing smoke production. In schools, for example, these panels can be used in classrooms, libraries, and auditoriums to ensure a safe environment for students and staff. Hospitals also benefit from the use of fire-retardant MDF panels, as they help to create a safer environment for patients and healthcare workers. In government offices, these panels can be used in meeting rooms, offices, and public areas to enhance fire safety and comply with regulations. In commercial buildings, the use of fire-retardant MDF panels is equally important. These buildings, which include shopping malls, office complexes, and hotels, often have high occupancy levels and require robust fire safety measures to protect occupants and assets. Fire retardant MDF panels are used in a variety of applications within commercial buildings, such as wall paneling, ceilings, and partitions, to enhance fire safety and meet regulatory requirements. In shopping malls, for example, these panels can be used in common areas, retail spaces, and food courts to ensure a safe environment for shoppers and staff. Office complexes benefit from the use of fire-retardant MDF panels in meeting rooms, workspaces, and common areas, providing a safer environment for employees and visitors. Hotels also rely on these panels to enhance fire safety in guest rooms, lobbies, and conference facilities, ensuring the safety and comfort of guests. Overall, the use of fire-retardant MDF panels in public and commercial buildings is a critical component of fire safety strategies, helping to protect occupants and assets while ensuring compliance with regulations.

Global Fire Retardant Medium Density Fiberboard (MDF) Panels Market Outlook:

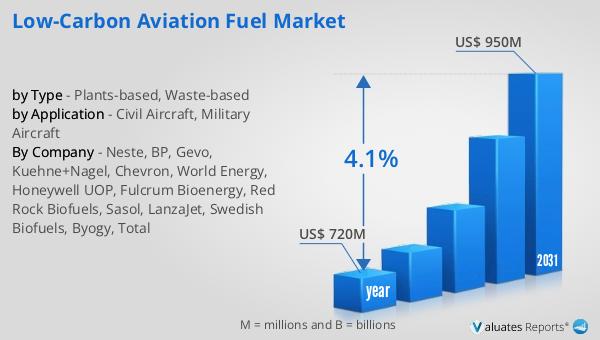

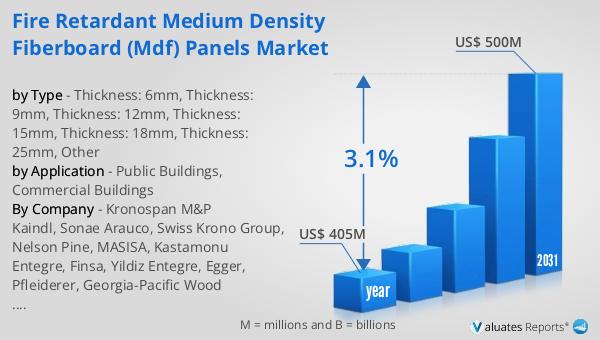

The global market for Fire Retardant Medium Density Fiberboard (MDF) Panels was valued at approximately $405 million in 2024, and it is anticipated to grow to a revised size of around $500 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.1% over the forecast period. This steady growth can be attributed to several factors, including the increasing emphasis on fire safety in construction and interior design, as well as the implementation of stricter building codes and regulations that mandate the use of fire-retardant materials. The demand for these panels is also driven by the rising awareness among consumers and builders about the importance of fire safety, leading to a preference for materials that offer enhanced protection against fire hazards. Additionally, the ongoing urbanization and construction activities across the globe are contributing to the increased demand for fire-retardant MDF panels, as they are widely used in both residential and commercial applications. As the market continues to evolve, manufacturers are focusing on innovation and sustainability, developing new products that not only meet fire safety standards but also address environmental concerns. This includes the use of eco-friendly materials and processes, which are becoming increasingly important to consumers and regulatory bodies alike. Overall, the global market for fire-retardant MDF panels is poised for steady growth, offering opportunities for both established players and new entrants to capitalize on the increasing demand for fire-safe building materials.

| Report Metric | Details |

| Report Name | Fire Retardant Medium Density Fiberboard (MDF) Panels Market |

| Accounted market size in year | US$ 405 million |

| Forecasted market size in 2031 | US$ 500 million |

| CAGR | 3.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Kronospan M&P Kaindl, Sonae Arauco, Swiss Krono Group, Nelson Pine, MASISA, Kastamonu Entegre, Finsa, Yildiz Entegre, Egger, Pfleiderer, Georgia-Pacific Wood Products, Dongwha, Medite, Unilin, Dare Wood-Based Panels Group Co., Ltd, ALFA WOOD GROUP |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |