What is Global Microporous PTFE Membrane Market?

The Global Microporous PTFE Membrane Market is a specialized segment within the broader membrane technology industry, focusing on the production and application of microporous polytetrafluoroethylene (PTFE) membranes. These membranes are known for their exceptional chemical resistance, thermal stability, and unique microporous structure, which allows them to filter particles while permitting the passage of gases and vapors. The market encompasses a wide range of industries, including medical, industrial filtration, electronics, textiles, and automotive, where these membranes are used for various applications such as filtration, separation, and protective barriers. The demand for microporous PTFE membranes is driven by their superior performance in harsh environments, their ability to enhance product longevity, and their contribution to energy efficiency and sustainability. As industries continue to seek advanced materials that offer both high performance and environmental benefits, the Global Microporous PTFE Membrane Market is poised for growth, driven by technological advancements and increasing awareness of the benefits of these versatile membranes.

Hydrophobic Microporous PTFE Membrane, Hydrophilic Microporous PTFE Membrane in the Global Microporous PTFE Membrane Market:

Hydrophobic and hydrophilic microporous PTFE membranes are two distinct types of membranes within the Global Microporous PTFE Membrane Market, each offering unique properties and applications. Hydrophobic microporous PTFE membranes are characterized by their ability to repel water while allowing the passage of air and gases. This makes them ideal for applications where moisture control is critical, such as in venting systems, protective clothing, and electronic enclosures. These membranes prevent water ingress while maintaining breathability, ensuring that sensitive components remain dry and functional. In contrast, hydrophilic microporous PTFE membranes are designed to attract and absorb water, making them suitable for applications that require efficient liquid filtration and separation. These membranes are often used in medical devices, water treatment systems, and laboratory filtration processes, where their ability to filter out impurities while allowing the passage of water is essential. The choice between hydrophobic and hydrophilic membranes depends on the specific requirements of the application, with each type offering distinct advantages in terms of performance and functionality. The Global Microporous PTFE Membrane Market continues to evolve as manufacturers develop new formulations and technologies to enhance the properties of these membranes, catering to the diverse needs of industries worldwide. As the demand for high-performance filtration and separation solutions grows, the market for both hydrophobic and hydrophilic microporous PTFE membranes is expected to expand, driven by innovations in material science and a growing emphasis on sustainability and efficiency.

Industrial Filtration, Electric & Electronics, Medical, Textile, Automotive, Others in the Global Microporous PTFE Membrane Market:

The Global Microporous PTFE Membrane Market finds extensive usage across various industries, each leveraging the unique properties of these membranes to enhance performance and efficiency. In industrial filtration, microporous PTFE membranes are used to filter out particulates and contaminants from air and liquids, ensuring clean and safe environments in manufacturing processes. Their chemical resistance and durability make them ideal for harsh industrial settings, where they contribute to improved product quality and reduced maintenance costs. In the electronics sector, these membranes are employed to protect sensitive components from moisture and dust, enhancing the reliability and longevity of electronic devices. The medical industry utilizes microporous PTFE membranes in applications such as surgical masks, wound dressings, and drug delivery systems, where their biocompatibility and ability to filter out pathogens are critical. In the textile industry, these membranes are used to create breathable and waterproof fabrics, offering comfort and protection in outdoor and performance apparel. The automotive industry benefits from the use of microporous PTFE membranes in fuel filtration systems, cabin air filters, and protective covers, where they help improve vehicle performance and passenger comfort. Other applications include environmental protection, where these membranes are used in air and water purification systems, contributing to sustainability and public health. The versatility and adaptability of microporous PTFE membranes make them a valuable component in a wide range of applications, driving their demand across multiple sectors.

Global Microporous PTFE Membrane Market Outlook:

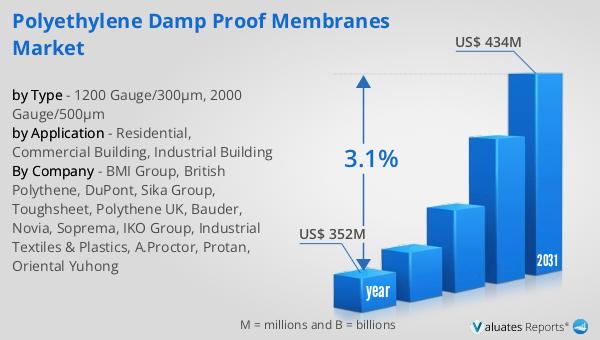

In 2024, the global market for Microporous PTFE Membranes was valued at approximately $1,364 million. Looking ahead, this market is anticipated to grow, reaching an estimated value of $1,776 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.9% over the forecast period. This steady increase in market size reflects the rising demand for microporous PTFE membranes across various industries, driven by their unique properties and wide range of applications. As industries continue to seek advanced materials that offer both high performance and environmental benefits, the market for these membranes is expected to expand. The growth is supported by technological advancements and increasing awareness of the benefits of these versatile membranes. As the demand for high-performance filtration and separation solutions grows, the market for microporous PTFE membranes is poised for continued expansion, driven by innovations in material science and a growing emphasis on sustainability and efficiency.

| Report Metric | Details |

| Report Name | Microporous PTFE Membrane Market |

| Accounted market size in year | US$ 1364 million |

| Forecasted market size in 2031 | US$ 1776 million |

| CAGR | 3.9% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Gore, Saint-Gobain Performance Plastics, Donaldson, Sumitomo Electric, Zeus, Nitto Denko, Shanghai JINYOU Fluorine Materials, Ningbo Dengyue New Material Technology, Ningbo Changqi Porous Membrane Technology, MicroVENT, Dongyang Jinlong Filter |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |