What is Global HJT Low Temperature Silver Paste Market?

The Global HJT Low Temperature Silver Paste Market is a specialized segment within the broader field of materials used in solar cell manufacturing. HJT, or Heterojunction Technology, is a type of solar cell technology that combines different types of silicon layers to enhance efficiency. The low-temperature silver paste is a critical component in this technology, as it is used to create the electrical contacts on the solar cells. This paste is specifically designed to function effectively at lower temperatures, which is crucial for maintaining the integrity and performance of the HJT cells. The market for this paste is driven by the increasing demand for high-efficiency solar cells, as well as the growing emphasis on renewable energy sources globally. As countries strive to meet their energy needs sustainably, the demand for advanced solar technologies like HJT is expected to rise, thereby boosting the market for low-temperature silver paste. This market is characterized by continuous innovation and development, as manufacturers seek to improve the performance and cost-effectiveness of their products to meet the evolving needs of the solar industry.

Front Side Silver Paste, Back Side Silver Paste in the Global HJT Low Temperature Silver Paste Market:

Front Side Silver Paste and Back Side Silver Paste are two critical components in the Global HJT Low Temperature Silver Paste Market, each serving distinct roles in the manufacturing of solar cells. The Front Side Silver Paste is primarily used to form the grid lines on the front surface of the solar cell. These grid lines are essential for collecting and conducting the electricity generated by the cell. The paste must have excellent conductivity and adhesion properties to ensure efficient energy transfer and long-term durability. It is also designed to be applied at low temperatures to prevent damage to the delicate silicon layers of the HJT cells. On the other hand, the Back Side Silver Paste is used on the rear surface of the solar cell. Its primary function is to create a conductive layer that facilitates the flow of electricity out of the cell. This paste also needs to have high conductivity and strong adhesion, but it is typically formulated to be more robust to withstand the different environmental conditions that the back side of the cell may encounter. Both types of paste are crucial for the overall efficiency and performance of HJT solar cells. The development of these pastes involves a delicate balance of chemistry and engineering to achieve the desired properties. Manufacturers are constantly researching and testing new formulations to improve the performance of their products. This includes experimenting with different silver particle sizes, binders, and additives to enhance conductivity, adhesion, and thermal stability. The market for these pastes is highly competitive, with numerous companies vying for a share of the growing demand for high-efficiency solar cells. As the solar industry continues to evolve, the requirements for silver pastes are also changing. There is a growing emphasis on reducing the silver content in these pastes to lower costs and minimize the environmental impact of silver mining. This has led to the development of new formulations that use alternative materials or innovative designs to achieve similar performance with less silver. Additionally, the trend towards thinner and more flexible solar cells is driving the need for pastes that can be applied in thinner layers without compromising performance. The Global HJT Low Temperature Silver Paste Market is thus a dynamic and rapidly evolving field, with ongoing research and development efforts aimed at meeting the changing needs of the solar industry.

Photovoltaic(PV), Building Integrated Photovoltaic(BIPV) in the Global HJT Low Temperature Silver Paste Market:

The usage of Global HJT Low Temperature Silver Paste Market in the areas of Photovoltaic (PV) and Building Integrated Photovoltaic (BIPV) is significant, as these sectors are at the forefront of the renewable energy revolution. In the photovoltaic sector, HJT technology is gaining traction due to its superior efficiency compared to traditional solar cell technologies. The low-temperature silver paste is a key enabler of this technology, as it allows for the creation of high-quality electrical contacts without damaging the sensitive silicon layers. This is particularly important in the PV sector, where maximizing energy output and efficiency is crucial for the economic viability of solar installations. The use of low-temperature silver paste in HJT cells helps to reduce energy losses and improve the overall performance of solar panels, making them more attractive to consumers and businesses looking to invest in renewable energy. In the BIPV sector, the integration of solar cells into building materials presents unique challenges and opportunities. BIPV systems are designed to seamlessly blend with the architecture of buildings, providing both aesthetic and functional benefits. The use of HJT technology in BIPV applications is particularly advantageous due to its high efficiency and ability to perform well in a variety of lighting conditions. The low-temperature silver paste used in these applications must be carefully formulated to ensure strong adhesion and conductivity while maintaining the visual appeal of the building materials. This requires a high degree of precision in the manufacturing process, as well as ongoing research and development to optimize the performance of the paste. The demand for BIPV systems is expected to grow as more architects and builders seek to incorporate renewable energy solutions into their designs. The Global HJT Low Temperature Silver Paste Market is thus poised to play a critical role in the expansion of both the PV and BIPV sectors. As the world continues to transition towards cleaner energy sources, the importance of advanced materials like low-temperature silver paste will only increase. This market is characterized by rapid innovation and a strong focus on sustainability, as manufacturers strive to develop products that meet the evolving needs of the solar industry while minimizing their environmental impact.

Global HJT Low Temperature Silver Paste Market Outlook:

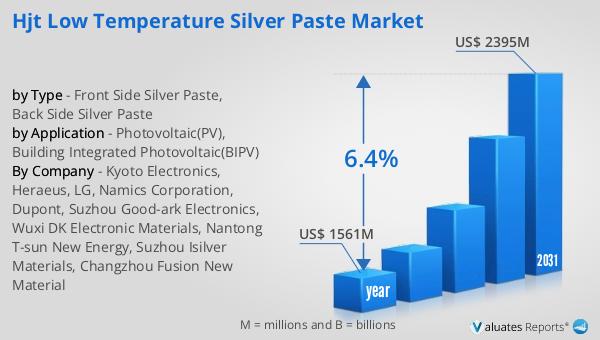

The global market for HJT Low Temperature Silver Paste was valued at $1,561 million in 2024 and is anticipated to grow significantly over the coming years. By 2031, it is projected to reach a revised size of $2,395 million, reflecting a compound annual growth rate (CAGR) of 6.4% during the forecast period. This growth is indicative of the increasing demand for high-efficiency solar technologies and the critical role that low-temperature silver paste plays in the production of HJT solar cells. As the market expands, manufacturers are likely to focus on enhancing the performance and cost-effectiveness of their products to capture a larger share of this growing market. The projected growth of the market underscores the importance of ongoing research and development efforts aimed at improving the properties of silver paste, such as conductivity, adhesion, and thermal stability. Additionally, the trend towards reducing the silver content in these pastes to lower costs and minimize environmental impact is expected to drive further innovation in the field. As countries around the world continue to invest in renewable energy solutions, the demand for advanced materials like low-temperature silver paste is likely to increase, supporting the overall growth of the market.

| Report Metric | Details |

| Report Name | HJT Low Temperature Silver Paste Market |

| Accounted market size in year | US$ 1561 million |

| Forecasted market size in 2031 | US$ 2395 million |

| CAGR | 6.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Kyoto Electronics, Heraeus, LG, Namics Corporation, Dupont, Suzhou Good-ark Electronics, Wuxi DK Electronic Materials, Nantong T-sun New Energy, Suzhou Isilver Materials, Changzhou Fusion New Material |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |