What is Global Scleroderma Therapeutics Market?

The Global Scleroderma Therapeutics Market refers to the worldwide industry focused on developing and providing treatments for scleroderma, a chronic connective tissue disease characterized by skin thickening and hardening. This market encompasses a range of therapeutic options aimed at managing the symptoms and progression of the disease, which can affect not only the skin but also internal organs. The market is driven by increasing awareness of the disease, advancements in medical research, and the growing demand for effective treatments. Pharmaceutical companies, research institutions, and healthcare providers are key players in this market, working collaboratively to develop innovative therapies. The market's growth is also influenced by the rising prevalence of autoimmune diseases and the need for personalized medicine approaches. As the understanding of scleroderma's underlying mechanisms improves, the market is expected to expand, offering new hope for patients through targeted therapies and improved quality of life. The Global Scleroderma Therapeutics Market is a dynamic and evolving sector, reflecting the broader trends in healthcare innovation and patient-centered care.

Immunosuppressors, Phosphodiesterase 5 Inhibitors - PHA, Endothelin Receptor Antagonists, Prostacyclin Analogues, Calcium Channel Blockers, Analgesics, Others in the Global Scleroderma Therapeutics Market:

Immunosuppressors are a cornerstone in the treatment of scleroderma, particularly for systemic forms of the disease. These drugs work by dampening the immune system's activity, which is crucial in a condition where the immune system mistakenly attacks the body's own tissues. Common immunosuppressors used in scleroderma include methotrexate, mycophenolate mofetil, and cyclophosphamide. These medications help reduce inflammation and slow down the progression of skin thickening and organ involvement. Phosphodiesterase 5 Inhibitors (PDE5 inhibitors) like sildenafil are used primarily to manage pulmonary arterial hypertension (PAH), a serious complication of scleroderma. By relaxing blood vessels and improving blood flow, these drugs help alleviate symptoms such as shortness of breath and fatigue. Endothelin Receptor Antagonists (ERAs) are another class of drugs used to treat PAH in scleroderma patients. These medications, including bosentan and ambrisentan, work by blocking the effects of endothelin, a substance that causes blood vessels to constrict. Prostacyclin Analogues, such as epoprostenol and treprostinil, are potent vasodilators that help improve blood flow and reduce PAH symptoms. They mimic the effects of prostacyclin, a naturally occurring substance in the body that dilates blood vessels and inhibits platelet aggregation. Calcium Channel Blockers are often prescribed to manage Raynaud's phenomenon, a common symptom of scleroderma characterized by reduced blood flow to the fingers and toes. These drugs, including nifedipine and amlodipine, help relax and widen blood vessels, improving circulation. Analgesics are used to manage pain associated with scleroderma, providing relief from joint and muscle discomfort. Other treatments in the scleroderma therapeutics market include antifibrotic agents, which aim to reduce fibrosis or scarring of tissues, and lifestyle modifications that support overall health and well-being. The diverse range of therapeutic options reflects the complexity of scleroderma and the need for a multifaceted approach to treatment. Each class of medication plays a specific role in managing different aspects of the disease, highlighting the importance of personalized treatment plans tailored to individual patient needs. As research continues to advance, new therapies are likely to emerge, offering additional hope for those affected by this challenging condition.

Systemic, Localized in the Global Scleroderma Therapeutics Market:

The usage of Global Scleroderma Therapeutics Market in systemic and localized scleroderma varies significantly due to the distinct nature of these two forms of the disease. Systemic scleroderma, also known as systemic sclerosis, affects not only the skin but also internal organs such as the lungs, heart, and kidneys. In this form, the therapeutic approach is more comprehensive and often involves a combination of medications to address the wide range of symptoms and complications. Immunosuppressors are frequently used in systemic scleroderma to control the overactive immune response and prevent further organ damage. For patients with pulmonary arterial hypertension, PDE5 inhibitors and ERAs are critical in managing this life-threatening complication. Prostacyclin analogues may also be used to improve blood flow and reduce symptoms. In addition to these medications, systemic scleroderma treatment may include antifibrotic agents to reduce tissue scarring and lifestyle interventions to support overall health. Localized scleroderma, on the other hand, primarily affects the skin and sometimes the underlying tissues but does not involve internal organs. The treatment focus for localized scleroderma is often on managing skin symptoms and preventing progression. Topical treatments, such as corticosteroids and moisturizers, are commonly used to reduce inflammation and maintain skin health. In some cases, phototherapy or laser treatments may be employed to improve skin appearance and texture. While systemic medications are less commonly used in localized scleroderma, they may be considered in severe cases or when the disease significantly impacts quality of life. The therapeutic strategies for systemic and localized scleroderma highlight the importance of a tailored approach to treatment, taking into account the specific needs and challenges of each patient. As the Global Scleroderma Therapeutics Market continues to evolve, ongoing research and innovation are expected to enhance the effectiveness and accessibility of treatments for both forms of the disease, ultimately improving patient outcomes and quality of life.

Global Scleroderma Therapeutics Market Outlook:

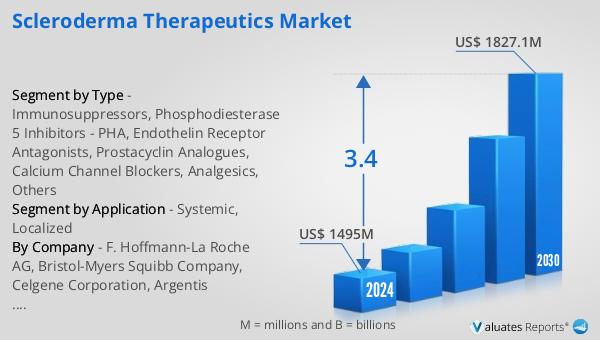

The outlook for the Global Scleroderma Therapeutics Market indicates a steady growth trajectory, with projections suggesting an increase from $1,495 million in 2024 to $1,827.1 million by 2030, reflecting a Compound Annual Growth Rate (CAGR) of 3.4% during this period. This growth is indicative of the rising demand for effective treatments and the ongoing advancements in therapeutic options for scleroderma. In the broader context, the global pharmaceutical market was valued at $1,475 billion in 2022 and is expected to grow at a CAGR of 5% over the next six years. This growth underscores the expanding landscape of pharmaceutical innovations and the increasing focus on addressing complex diseases like scleroderma. Comparatively, the chemical drug market has shown a steady increase from $1,005 billion in 2018 to $1,094 billion in 2022, highlighting the sustained demand for chemical-based therapies. The growth in the Scleroderma Therapeutics Market is driven by factors such as increased awareness of the disease, advancements in medical research, and the development of targeted therapies. As the market continues to expand, it is expected to offer new opportunities for pharmaceutical companies, healthcare providers, and patients alike, contributing to improved treatment outcomes and quality of life for those affected by scleroderma.

| Report Metric | Details |

| Report Name | Scleroderma Therapeutics Market |

| Accounted market size in 2024 | US$ 1495 in million |

| Forecasted market size in 2030 | US$ 1827.1 million |

| CAGR | 3.4 |

| Base Year | 2024 |

| Forecasted years | 2025 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | F. Hoffmann-La Roche AG, Bristol-Myers Squibb Company, Celgene Corporation, Argentis Pharmaceuticals, LLC, Bayer AG, Boehringer Ingelheim International GmbH, Akashi Therapeutics, Prometic Life Sciences, Inc., Emerald Health Pharmaceuticals, Kadmon Holdings, Inc., Seattle Genetics, Inc., Cytori Therapeutics, Inc., Fibrocell Science, Inc., Chemomab, Corbus Pharmaceuticals Holdings, Inc., Genkyotex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |