What is Liquid Rocket Engine - Global Market?

Liquid rocket engines are a crucial component in the global aerospace and defense industries, serving as the primary propulsion system for various applications. These engines operate by burning liquid propellants, typically a combination of liquid oxygen and a fuel such as kerosene or liquid hydrogen, to produce thrust. The global market for liquid rocket engines is driven by the increasing demand for space exploration, satellite deployment, and defense applications. As countries and private companies invest more in space missions and satellite technologies, the need for reliable and efficient propulsion systems grows. Liquid rocket engines are favored for their high efficiency and ability to be throttled, shut down, and restarted, making them versatile for different mission profiles. The market is characterized by technological advancements aimed at improving engine performance, reducing costs, and enhancing safety. Key players in the industry are focusing on research and development to innovate and meet the evolving demands of the market. The global market for liquid rocket engines is poised for growth as new space ventures and defense strategies continue to emerge, highlighting the importance of these engines in achieving ambitious aerospace goals.

Heavy Size, Middle Size, Small Size in the Liquid Rocket Engine - Global Market:

The liquid rocket engine market is segmented based on the size of the engines, which can be broadly categorized into heavy, middle, and small sizes. Heavy-size liquid rocket engines are typically used in large launch vehicles and heavy-lift rockets. These engines are designed to generate significant thrust to propel massive payloads into space, such as large satellites, space station modules, or interplanetary missions. The demand for heavy-size engines is driven by the need for powerful propulsion systems capable of carrying substantial loads over long distances. Middle-size liquid rocket engines, on the other hand, are often used in medium-lift launch vehicles and are suitable for launching smaller satellites or payloads into low Earth orbit (LEO). These engines offer a balance between power and efficiency, making them ideal for missions that require moderate thrust levels. The market for middle-size engines is expanding as more countries and private companies seek to deploy constellations of small satellites for communication, Earth observation, and scientific research. Small-size liquid rocket engines are used in small launch vehicles and upper stages of larger rockets. These engines are designed for precision and efficiency, often used for final orbital insertion or maneuvering satellites once they are in space. The growing interest in small satellite launches and the development of dedicated small launch vehicles are driving the demand for small-size liquid rocket engines. Each size category presents unique challenges and opportunities for manufacturers, as they strive to optimize engine performance, reduce costs, and meet the specific requirements of different missions. The global market for liquid rocket engines is dynamic, with advancements in materials, manufacturing techniques, and propulsion technologies shaping the future of space exploration and defense capabilities. As the industry evolves, the focus remains on enhancing engine reliability, reducing environmental impact, and achieving greater cost-effectiveness to support the increasing number of space missions and defense applications worldwide.

Spacecraft, Ballistic Missiles in the Liquid Rocket Engine - Global Market:

Liquid rocket engines play a vital role in the global market, particularly in the areas of spacecraft and ballistic missiles. In the realm of spacecraft, these engines are essential for launching satellites, space probes, and crewed missions into space. The ability of liquid rocket engines to provide precise thrust control and high efficiency makes them ideal for a wide range of space missions. They are used in the initial launch phase to propel spacecraft out of Earth's atmosphere and into orbit. Once in space, liquid rocket engines are often employed for orbital maneuvers, such as adjusting a satellite's position or changing its orbit. The versatility of these engines allows for complex mission profiles, including interplanetary travel and deep space exploration. In the defense sector, liquid rocket engines are a critical component of ballistic missiles. These engines provide the necessary thrust to propel missiles over long distances, delivering payloads with precision and speed. The ability to throttle and restart liquid rocket engines offers strategic advantages in missile deployment, allowing for controlled flight paths and target adjustments. The global market for liquid rocket engines in defense is influenced by geopolitical factors and the need for advanced missile technologies. As countries seek to enhance their defense capabilities, the demand for reliable and efficient propulsion systems continues to grow. The development of new materials and technologies is driving innovation in liquid rocket engines, improving their performance and reducing costs. This progress is essential for meeting the increasing demands of both space exploration and defense applications. The global market for liquid rocket engines is poised for growth as new opportunities and challenges arise in the aerospace and defense industries. The focus remains on enhancing engine performance, reducing environmental impact, and achieving greater cost-effectiveness to support the expanding number of space missions and defense applications worldwide.

Liquid Rocket Engine - Global Market Outlook:

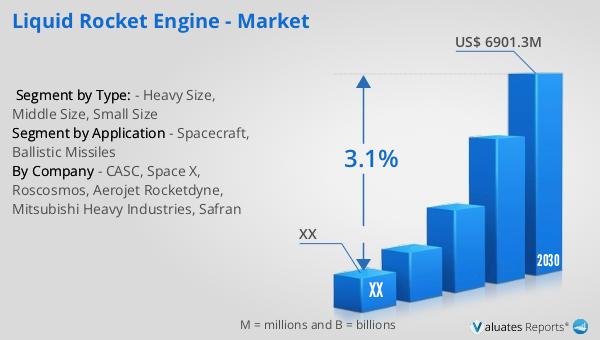

The global market for liquid rocket engines was valued at approximately $5,590.2 million in 2023, with projections indicating a growth to around $6,901.3 million by 2030. This represents a compound annual growth rate (CAGR) of 3.1% over the forecast period from 2024 to 2030. The North American market, a significant player in the industry, was valued at an undisclosed amount in 2023, with expectations of reaching a higher value by 2030, although specific figures and growth rates for this region were not provided. The growth in the global market is driven by increasing investments in space exploration, satellite deployment, and defense applications, which require advanced propulsion systems like liquid rocket engines. Technological advancements and innovations in engine design, materials, and manufacturing processes are also contributing to market expansion. As countries and private companies continue to invest in space missions and defense capabilities, the demand for efficient and reliable liquid rocket engines is expected to rise. The market outlook suggests a positive trajectory for the industry, with opportunities for growth and development in various regions worldwide. The focus remains on enhancing engine performance, reducing costs, and meeting the evolving demands of the aerospace and defense sectors.

| Report Metric | Details |

| Report Name | Liquid Rocket Engine - Market |

| Forecasted market size in 2030 | US$ 6901.3 million |

| CAGR | 3.1% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | CASC, Space X, Roscosmos, Aerojet Rocketdyne, Mitsubishi Heavy Industries, Safran |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |