What is Seatbelt Gas Generator - Global Market?

The seatbelt gas generator is a crucial component in modern automotive safety systems, specifically designed to enhance the effectiveness of seatbelts during a collision. This device is responsible for the rapid inflation of the seatbelt pretensioner, which tightens the seatbelt instantly upon impact, thereby reducing the forward movement of the passenger and minimizing the risk of injury. The global market for seatbelt gas generators is driven by the increasing emphasis on vehicle safety standards and the growing awareness among consumers about the importance of advanced safety features in automobiles. As automotive manufacturers continue to innovate and integrate more sophisticated safety technologies, the demand for seatbelt gas generators is expected to rise. This market encompasses a wide range of applications across different vehicle types, including passenger cars and commercial vehicles, and is influenced by various factors such as regulatory requirements, technological advancements, and consumer preferences. The ongoing developments in the automotive industry, coupled with the rising production of vehicles in key regions, are likely to shape the future trajectory of the seatbelt gas generator market.

OEMs, Aftermarket in the Seatbelt Gas Generator - Global Market:

In the context of the seatbelt gas generator market, Original Equipment Manufacturers (OEMs) and the aftermarket play significant roles in the distribution and application of these safety components. OEMs are the companies that produce vehicles and integrate seatbelt gas generators as part of the original safety systems in new cars. These manufacturers are pivotal in driving the demand for seatbelt gas generators as they strive to meet stringent safety regulations and enhance the overall safety profile of their vehicles. OEMs work closely with suppliers of seatbelt gas generators to ensure that the components meet the required standards and specifications. The collaboration between OEMs and suppliers is crucial for the development of innovative and efficient safety solutions that cater to the evolving needs of the automotive industry. On the other hand, the aftermarket segment refers to the market for replacement parts and accessories for vehicles after they have been sold. In the context of seatbelt gas generators, the aftermarket provides opportunities for the replacement and upgrading of these components in existing vehicles. This segment is driven by factors such as the increasing lifespan of vehicles, the need for maintenance and repair, and the growing awareness among consumers about the importance of maintaining safety features in their vehicles. The aftermarket for seatbelt gas generators is characterized by a diverse range of products and services, catering to different vehicle models and consumer preferences. Both OEMs and the aftermarket are integral to the growth and development of the seatbelt gas generator market, as they address the needs of new vehicle production and the maintenance of existing vehicles. The interplay between these two segments is essential for ensuring the widespread adoption and effectiveness of seatbelt gas generators in enhancing vehicle safety.

Passenger Vehicle, Commercial Vehicle in the Seatbelt Gas Generator - Global Market:

The usage of seatbelt gas generators in passenger vehicles and commercial vehicles highlights the critical role these components play in ensuring occupant safety across different types of automobiles. In passenger vehicles, seatbelt gas generators are an integral part of the safety systems designed to protect occupants in the event of a collision. These vehicles, which include sedans, hatchbacks, SUVs, and other personal cars, are equipped with seatbelt pretensioners that utilize gas generators to tighten the seatbelts instantly during an impact. This rapid tightening helps to secure the passengers in their seats, reducing the risk of injury by minimizing the forward movement of the body. The emphasis on safety features in passenger vehicles is driven by consumer demand for safer cars and regulatory requirements that mandate the inclusion of advanced safety technologies. As a result, the adoption of seatbelt gas generators in passenger vehicles is widespread and continues to grow as manufacturers strive to enhance the safety profile of their cars. In commercial vehicles, which include trucks, buses, and other vehicles used for transporting goods and passengers, seatbelt gas generators play a similar role in enhancing safety. These vehicles often operate in challenging environments and are subject to different safety standards compared to passenger vehicles. The integration of seatbelt gas generators in commercial vehicles is crucial for protecting drivers and passengers, especially in high-risk situations such as long-distance travel and heavy-duty operations. The demand for seatbelt gas generators in commercial vehicles is influenced by factors such as the increasing focus on road safety, the need to comply with safety regulations, and the growing awareness among fleet operators about the importance of equipping their vehicles with advanced safety features. Overall, the usage of seatbelt gas generators in both passenger and commercial vehicles underscores the importance of these components in enhancing vehicle safety and protecting occupants across different types of automobiles.

Seatbelt Gas Generator - Global Market Outlook:

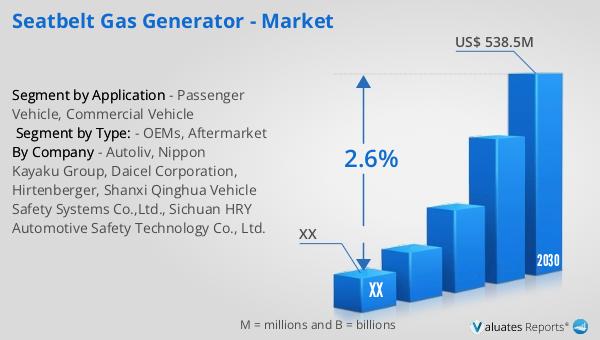

The global market for seatbelt gas generators was valued at approximately $450.4 million in 2023, with projections indicating a growth to around $538.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 2.6% during the forecast period from 2024 to 2030. This market growth is driven by the increasing demand for advanced safety features in vehicles and the continuous efforts by automotive manufacturers to enhance the safety standards of their products. Currently, more than 90% of the world's automobiles are concentrated in Asia, Europe, and North America. Asia leads the global automobile production, accounting for 56% of the world's output, followed by Europe with 20%, and North America with 16%. This concentration of automobile production in these regions significantly influences the demand for seatbelt gas generators, as manufacturers in these areas are at the forefront of integrating advanced safety technologies into their vehicles. The growth of the seatbelt gas generator market is also supported by the rising awareness among consumers about the importance of vehicle safety and the increasing adoption of safety regulations by governments worldwide. As the automotive industry continues to evolve, the demand for seatbelt gas generators is expected to rise, driven by the need for safer vehicles and the ongoing advancements in safety technologies.

| Report Metric | Details |

| Report Name | Seatbelt Gas Generator - Market |

| Forecasted market size in 2030 | US$ 538.5 million |

| CAGR | 2.6% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | Autoliv, Nippon Kayaku Group, Daicel Corporation, Hirtenberger, Shanxi Qinghua Vehicle Safety Systems Co.,Ltd., Sichuan HRY Automotive Safety Technology Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |