What is Modular Kitchen Appliances - Global Market?

Modular kitchen appliances represent a significant segment of the global market, characterized by their innovative design and functionality that cater to modern living spaces. These appliances are designed to seamlessly integrate into kitchen cabinetry, offering a sleek and cohesive look while maximizing space efficiency. The global market for modular kitchen appliances is driven by the increasing demand for smart and efficient kitchen solutions that cater to the evolving lifestyle of consumers. With urbanization and the rise of compact living spaces, there is a growing need for appliances that not only perform well but also fit into limited spaces without compromising on aesthetics. The market encompasses a wide range of products, including built-in hobs, ovens, microwaves, dishwashers, barbeques, and refrigerators, each designed to enhance the cooking experience while maintaining a clutter-free environment. As consumers become more conscious of design and functionality, the demand for modular kitchen appliances continues to grow, making it a dynamic and rapidly evolving market. The integration of technology and design in these appliances is a testament to the industry's commitment to meeting the needs of modern consumers.

Built-in Hobs, Built-in Oven, Built-in Microwaves, Built-in Dishwasher, Built-in Barbeque, Built-in Refrigerator in the Modular Kitchen Appliances - Global Market:

Built-in hobs are a staple in modular kitchens, offering a seamless cooking experience with their sleek design and efficient functionality. These hobs are integrated into the kitchen countertop, providing a streamlined look that complements the overall kitchen design. They come in various configurations, including gas, electric, and induction, catering to different cooking preferences and needs. Built-in ovens, on the other hand, are designed to fit into kitchen cabinetry, offering a space-saving solution without compromising on performance. These ovens come with advanced features such as convection cooking, self-cleaning, and programmable settings, making them a versatile addition to any kitchen. Built-in microwaves are another essential component of modular kitchens, providing quick and efficient cooking solutions. These microwaves are designed to be installed within the cabinetry, freeing up valuable counter space and maintaining a clean and organized kitchen environment. Built-in dishwashers are designed to blend seamlessly with kitchen cabinetry, offering a discreet and efficient solution for cleaning dishes. These dishwashers come with various features, including multiple wash cycles, energy efficiency, and noise reduction, making them a practical choice for modern kitchens. Built-in barbeques are a unique addition to modular kitchens, offering the convenience of outdoor grilling within the comfort of the home. These barbeques are designed to be integrated into the kitchen layout, providing a versatile cooking option for those who enjoy grilling. Built-in refrigerators are designed to fit seamlessly into kitchen cabinetry, offering a cohesive look while providing ample storage space for food and beverages. These refrigerators come with advanced features such as temperature control, energy efficiency, and customizable storage options, making them a valuable addition to any modular kitchen. The global market for these built-in appliances is driven by the increasing demand for efficient and aesthetically pleasing kitchen solutions that cater to the modern lifestyle. As consumers continue to prioritize design and functionality, the demand for built-in kitchen appliances is expected to grow, making it a key segment of the modular kitchen appliances market.

Household, Commercial in the Modular Kitchen Appliances - Global Market:

The usage of modular kitchen appliances extends beyond residential households to commercial settings, each with its unique requirements and benefits. In households, modular kitchen appliances offer a blend of functionality and aesthetics, catering to the modern lifestyle of consumers. These appliances are designed to maximize space efficiency, making them ideal for compact living spaces. The integration of technology in these appliances enhances the cooking experience, offering features such as programmable settings, energy efficiency, and smart connectivity. For instance, built-in ovens and microwaves provide versatile cooking options, while built-in dishwashers offer a convenient solution for cleaning dishes. The sleek design of these appliances complements the overall kitchen decor, creating a cohesive and organized environment. In commercial settings, such as restaurants and cafes, modular kitchen appliances play a crucial role in enhancing operational efficiency. These appliances are designed to withstand the demands of a busy kitchen, offering durability and performance. Built-in hobs and ovens provide efficient cooking solutions, while built-in dishwashers ensure quick and effective cleaning of dishes. The integration of technology in these appliances allows for precise control and monitoring, enhancing the overall efficiency of the kitchen operations. The demand for modular kitchen appliances in commercial settings is driven by the need for efficient and reliable solutions that cater to the high demands of the food service industry. As the global market for modular kitchen appliances continues to grow, the usage of these appliances in both household and commercial settings is expected to increase, driven by the need for efficient and aesthetically pleasing kitchen solutions.

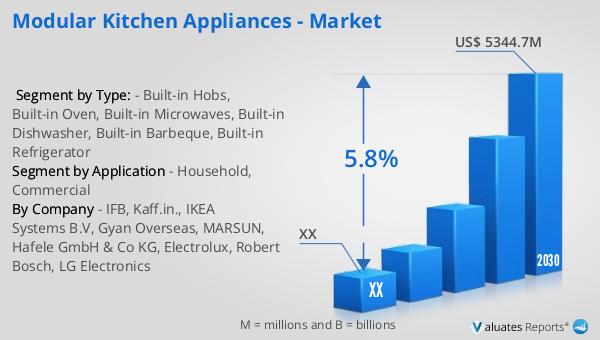

Modular Kitchen Appliances - Global Market Outlook:

The global market for modular kitchen appliances was valued at approximately $3,625 million in 2023, with projections indicating a growth to around $5,344.7 million by 2030. This growth is expected to occur at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2024 to 2030. The North American market, in particular, is a significant contributor to this growth, although specific figures for this region were not provided. The increasing demand for modular kitchen appliances is driven by the need for efficient and aesthetically pleasing kitchen solutions that cater to the modern lifestyle. The integration of technology and design in these appliances is a key factor driving market growth, as consumers continue to prioritize functionality and aesthetics in their kitchen spaces. The market encompasses a wide range of products, including built-in hobs, ovens, microwaves, dishwashers, barbeques, and refrigerators, each designed to enhance the cooking experience while maintaining a clutter-free environment. As the global market for modular kitchen appliances continues to grow, the demand for these products is expected to increase, driven by the need for efficient and aesthetically pleasing kitchen solutions.

| Report Metric | Details |

| Report Name | Modular Kitchen Appliances - Market |

| Forecasted market size in 2030 | US$ 5344.7 million |

| CAGR | 5.8% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | IFB, Kaff.in., IKEA Systems B.V, Gyan Overseas, MARSUN, Hafele GmbH & Co KG, Electrolux, Robert Bosch, LG Electronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |