What is Global Compact Motor Grader Market?

The Global Compact Motor Grader Market refers to the worldwide industry focused on the production, distribution, and utilization of compact motor graders. These machines are essential in various construction and maintenance activities due to their ability to create a smooth, flat surface. Compact motor graders are smaller and more maneuverable than their larger counterparts, making them ideal for projects that require precision in confined spaces. They are used in tasks such as road construction, snow removal, and the maintenance of soil and gravel roads. The market for these machines is driven by the increasing demand for infrastructure development and the need for efficient and versatile equipment. As urbanization and industrialization continue to grow, the demand for compact motor graders is expected to rise, making this market a significant segment within the broader construction equipment industry.

Rigid Frame Motor Grader, Articulated Frame Motor Grader in the Global Compact Motor Grader Market:

Rigid Frame Motor Graders and Articulated Frame Motor Graders are two primary types of machines within the Global Compact Motor Grader Market. Rigid Frame Motor Graders are characterized by their fixed, non-flexible frame, which provides stability and strength. These graders are typically used in applications where a high degree of precision and control is required, such as in the construction of highways and large-scale infrastructure projects. The rigid frame design ensures that the machine can handle heavy loads and maintain a consistent grading performance, making it ideal for tasks that demand durability and reliability. On the other hand, Articulated Frame Motor Graders feature a flexible frame that can pivot at the center, allowing for greater maneuverability and versatility. This design enables the machine to navigate tight spaces and complex terrains more easily, making it suitable for urban construction projects, road maintenance, and other tasks that require a high level of adaptability. The articulated frame allows the grader to make sharper turns and adjust its blade angle more effectively, enhancing its overall performance in various conditions. Both types of motor graders play a crucial role in the Global Compact Motor Grader Market, catering to different needs and preferences of end-users. The choice between a rigid frame and an articulated frame motor grader often depends on the specific requirements of the project, including the type of terrain, the level of precision needed, and the overall scope of the work. As the demand for infrastructure development continues to grow, the market for both rigid frame and articulated frame motor graders is expected to expand, driven by the need for efficient and versatile construction equipment.

Construction, Snow Removing, Soil and Gravel Road Maintenance, Others in the Global Compact Motor Grader Market:

The usage of Global Compact Motor Grader Market machines spans several key areas, including construction, snow removal, soil and gravel road maintenance, and other applications. In construction, compact motor graders are indispensable for creating smooth and level surfaces, which are essential for building roads, highways, and other infrastructure projects. Their ability to precisely grade and level the ground ensures that the foundation for construction is stable and even, reducing the risk of structural issues in the future. Additionally, compact motor graders are used in site preparation, trenching, and landscaping, making them versatile tools in the construction industry. In snow removal, compact motor graders are highly effective in clearing snow from roads, parking lots, and other surfaces. Their powerful blades can cut through thick layers of snow, ensuring that transportation routes remain accessible and safe during winter months. The maneuverability of compact motor graders allows them to navigate tight spaces and clear snow from areas that larger machines may struggle to reach. For soil and gravel road maintenance, compact motor graders are essential in maintaining the quality and usability of unpaved roads. They can smooth out ruts, fill in potholes, and redistribute gravel, ensuring that the road surface remains even and safe for travel. This is particularly important in rural and remote areas where paved roads may not be available. Other applications of compact motor graders include landscaping, agricultural land leveling, and mining operations. In landscaping, these machines are used to create level surfaces for lawns, gardens, and other outdoor spaces. In agriculture, they help in preparing fields for planting by leveling the soil and removing obstacles. In mining, compact motor graders are used to maintain haul roads and other critical infrastructure within the mining site. Overall, the versatility and efficiency of compact motor graders make them valuable assets in a wide range of industries and applications.

Global Compact Motor Grader Market Outlook:

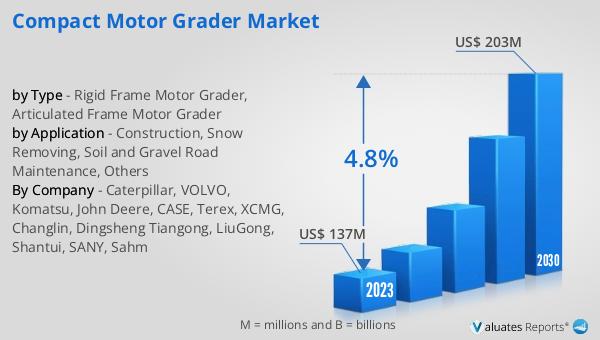

The global Compact Motor Grader market was valued at US$ 137 million in 2023 and is anticipated to reach US$ 203 million by 2030, witnessing a CAGR of 4.8% during the forecast period 2024-2030. This market outlook highlights the significant growth potential of the compact motor grader industry over the next several years. The increasing demand for infrastructure development, coupled with the need for efficient and versatile construction equipment, is expected to drive the market's expansion. As urbanization and industrialization continue to rise, the demand for compact motor graders is likely to grow, making this market a crucial segment within the broader construction equipment industry. The projected growth rate of 4.8% CAGR indicates a steady and sustained increase in market value, reflecting the ongoing investments in infrastructure projects and the adoption of advanced construction technologies. The anticipated market value of US$ 203 million by 2030 underscores the importance of compact motor graders in meeting the evolving needs of the construction and maintenance sectors. Overall, the market outlook for compact motor graders is positive, with significant opportunities for growth and development in the coming years.

| Report Metric | Details |

| Report Name | Compact Motor Grader Market |

| Accounted market size in 2023 | US$ 137 million |

| Forecasted market size in 2030 | US$ 203 million |

| CAGR | 4.8% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Caterpillar, VOLVO, Komatsu, John Deere, CASE, Terex, XCMG, Changlin, Dingsheng Tiangong, LiuGong, Shantui, SANY, Sahm |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |