What is Global FCC Refinery Catalysts Market?

The Global FCC Refinery Catalysts Market refers to the worldwide industry focused on the production and utilization of catalysts used in Fluid Catalytic Cracking (FCC) units within oil refineries. These catalysts play a crucial role in breaking down large, complex hydrocarbon molecules into simpler, more valuable products like gasoline, diesel, and other petrochemicals. The market encompasses various types of catalysts, including zeolites, matrices, binders, and fillers, each contributing to the efficiency and effectiveness of the cracking process. The demand for FCC refinery catalysts is driven by the continuous need for refined petroleum products, advancements in catalyst technology, and the growing emphasis on optimizing refinery operations to meet environmental regulations. As refineries strive to enhance their output and reduce emissions, the importance of high-performance FCC catalysts becomes increasingly significant. The market is characterized by ongoing research and development efforts aimed at improving catalyst formulations and performance, ensuring that refineries can meet the evolving demands of the energy sector.

Crystalline Zeolite, Matrix, Binder, Filler in the Global FCC Refinery Catalysts Market:

Crystalline zeolite, matrix, binder, and filler are essential components of FCC refinery catalysts, each serving a specific function to enhance the overall performance of the catalyst. Crystalline zeolites are microporous, aluminosilicate minerals that act as the primary active component in FCC catalysts. They possess a unique crystalline structure with a high surface area and strong acidity, which facilitates the cracking of large hydrocarbon molecules into smaller, more valuable products. The zeolite's structure allows for selective cracking, improving the yield of desired products like gasoline and propylene. The matrix, on the other hand, provides a support structure for the zeolite crystals and contributes to the catalyst's overall mechanical strength and stability. It also plays a role in the diffusion of reactants and products, ensuring efficient contact between the hydrocarbons and the active sites of the zeolite. Binders are used to hold the zeolite and matrix components together, forming a cohesive and durable catalyst particle. They enhance the physical integrity of the catalyst, preventing attrition and loss of active material during the high-temperature and high-pressure conditions of the FCC process. Common binders include silica, alumina, and clay materials. Fillers are inert materials added to the catalyst formulation to control the density and porosity of the catalyst particles. They help in optimizing the catalyst's physical properties, such as bulk density and pore size distribution, which are crucial for maintaining the desired flow characteristics and minimizing pressure drop in the FCC unit. The combination of these components results in a highly efficient and robust FCC catalyst that can withstand the harsh operating conditions of the refinery while maximizing the conversion of heavy hydrocarbons into valuable lighter products. The continuous improvement and innovation in the formulation of these components are essential for meeting the evolving demands of the refining industry and achieving higher levels of performance and sustainability.

Vacuum Gas Oil, Residue, Other in the Global FCC Refinery Catalysts Market:

The usage of Global FCC Refinery Catalysts Market in areas such as Vacuum Gas Oil (VGO), residue, and other feedstocks is critical for optimizing refinery operations and maximizing the yield of valuable products. Vacuum Gas Oil is a heavy petroleum fraction obtained from the vacuum distillation of crude oil. It serves as a primary feedstock for FCC units due to its high content of long-chain hydrocarbons. FCC catalysts are specifically designed to crack these long-chain molecules into shorter, more valuable products like gasoline, diesel, and olefins. The high activity and selectivity of FCC catalysts ensure efficient conversion of VGO, enhancing the overall profitability of the refinery. Residue, also known as residual oil or resid, is the heaviest fraction obtained from the distillation of crude oil. It contains a high concentration of complex, high-molecular-weight hydrocarbons and impurities such as sulfur, metals, and nitrogen compounds. FCC catalysts used for residue processing are formulated to withstand the challenging conditions posed by these impurities while maintaining high catalytic activity. Advanced catalyst formulations with enhanced metal tolerance and coke selectivity are employed to maximize the conversion of residue into valuable lighter products, reducing the production of low-value by-products like coke and slurry oil. Other feedstocks processed in FCC units include atmospheric gas oil, coker gas oil, and hydrotreated feedstocks. Each of these feedstocks presents unique challenges and requires specific catalyst formulations to achieve optimal performance. For instance, hydrotreated feedstocks, which have been pre-treated to remove impurities, require catalysts with high activity and selectivity to maximize the yield of desired products. The versatility and adaptability of FCC catalysts to process a wide range of feedstocks make them indispensable for modern refineries aiming to maximize their output and profitability. The continuous development of FCC catalyst technology, driven by the need for higher efficiency, lower emissions, and improved product quality, ensures that refineries can meet the ever-increasing demand for refined petroleum products while adhering to stringent environmental regulations.

Global FCC Refinery Catalysts Market Outlook:

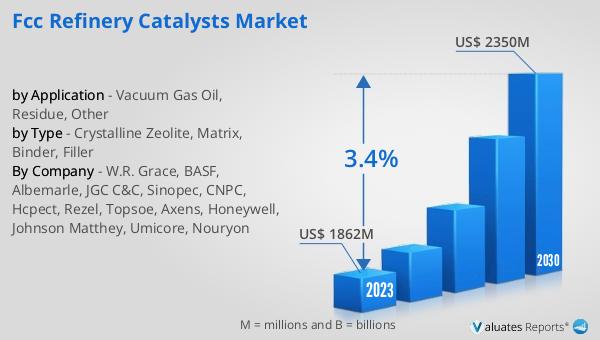

The global FCC Refinery Catalysts market was valued at US$ 1862 million in 2023 and is anticipated to reach US$ 2350 million by 2030, witnessing a CAGR of 3.4% during the forecast period 2024-2030. This market outlook indicates a steady growth trajectory driven by the increasing demand for refined petroleum products and the continuous advancements in catalyst technology. The projected growth reflects the ongoing efforts of refineries to optimize their operations, enhance product yields, and comply with environmental regulations. The market's expansion is also supported by the rising investments in research and development aimed at improving catalyst formulations and performance. As refineries strive to meet the evolving demands of the energy sector, the importance of high-performance FCC catalysts becomes increasingly significant. The anticipated growth in the market underscores the critical role of FCC catalysts in modern refining processes and highlights the need for continuous innovation to address the challenges posed by changing feedstock compositions and environmental requirements. The steady increase in market value over the forecast period demonstrates the resilience and adaptability of the FCC Refinery Catalysts market in the face of evolving industry dynamics and underscores its importance in the global energy landscape.

| Report Metric | Details |

| Report Name | FCC Refinery Catalysts Market |

| Accounted market size in 2023 | US$ 1862 million |

| Forecasted market size in 2030 | US$ 2350 million |

| CAGR | 3.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | W.R. Grace, BASF, Albemarle, JGC C&C, Sinopec, CNPC, Hcpect, Rezel, Topsoe, Axens, Honeywell, Johnson Matthey, Umicore, Nouryon |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |