What is Global Wind Energy Recycling Market?

The Global Wind Energy Recycling Market is a rapidly evolving sector that focuses on the sustainable disposal and repurposing of wind turbine components. As wind energy becomes a more prominent source of renewable energy worldwide, the need to manage the lifecycle of wind turbines, particularly their blades, has become increasingly important. Wind turbines are typically designed to last around 20-25 years, after which their components, especially the blades, need to be either refurbished or recycled. The recycling process involves breaking down these components into reusable materials, thereby reducing waste and promoting environmental sustainability. This market encompasses various technologies and methods to recycle different parts of wind turbines, including blades, towers, and nacelles. The goal is to minimize the environmental impact of decommissioned wind turbines and to create a circular economy where materials are continuously reused. The Global Wind Energy Recycling Market is driven by increasing environmental regulations, advancements in recycling technologies, and the growing emphasis on sustainable practices within the energy sector.

Carbon Fiber, Glass Fiber, Other Blade Materials in the Global Wind Energy Recycling Market:

Carbon fiber, glass fiber, and other blade materials play a crucial role in the Global Wind Energy Recycling Market. Wind turbine blades are primarily made from composite materials, with carbon fiber and glass fiber being the most common. Carbon fiber is known for its high strength-to-weight ratio, making it an ideal material for wind turbine blades that need to withstand significant mechanical stress while remaining lightweight. However, recycling carbon fiber is challenging due to its complex structure and the energy-intensive processes required to break it down. Despite these challenges, advancements in recycling technologies are making it increasingly feasible to recover and reuse carbon fiber from decommissioned blades. Glass fiber, on the other hand, is more commonly used in wind turbine blades due to its lower cost and adequate mechanical properties. Recycling glass fiber involves processes such as grinding and pyrolysis to break down the material into reusable forms. The recycled glass fiber can then be used in various applications, including the production of new blades, construction materials, and automotive components. Other blade materials, such as epoxy resins and balsa wood, also present unique recycling challenges. Epoxy resins, used as binding agents in composite blades, are difficult to recycle due to their thermosetting nature, which means they cannot be remelted and reshaped. However, research is ongoing to develop methods to break down these resins into reusable components. Balsa wood, used as a core material in some blades, can be recycled through processes such as grinding and composting. The recycling of these materials not only helps in reducing waste but also in conserving resources and reducing the carbon footprint associated with the production of new materials. The Global Wind Energy Recycling Market is thus a complex and multifaceted sector that requires continuous innovation and collaboration among various stakeholders, including manufacturers, recyclers, and policymakers, to develop effective and sustainable recycling solutions for wind turbine components.

Physical Recycling, Pyrolysis in the Global Wind Energy Recycling Market:

The usage of the Global Wind Energy Recycling Market in physical recycling and pyrolysis is essential for managing the lifecycle of wind turbine components. Physical recycling involves mechanical processes to break down wind turbine blades into smaller, reusable parts. This method typically includes cutting, grinding, and shredding the blades to separate the different materials, such as carbon fiber, glass fiber, and other composites. The resulting materials can then be repurposed for various applications, including the production of new wind turbine blades, construction materials, and automotive components. Physical recycling is advantageous because it is relatively straightforward and does not require complex chemical processes. However, it can be energy-intensive and may not fully recover all the valuable materials from the blades. Pyrolysis, on the other hand, is a thermal decomposition process that involves heating the wind turbine blades in the absence of oxygen to break down the composite materials into their constituent components. This process can recover valuable materials such as carbon fiber and glass fiber, as well as produce byproducts like oils and gases that can be used as energy sources. Pyrolysis is particularly effective for recycling composite materials that are difficult to break down through mechanical processes. It offers a higher recovery rate of valuable materials and can be more environmentally friendly compared to physical recycling. However, pyrolysis requires specialized equipment and can be more expensive to implement. Both physical recycling and pyrolysis play a crucial role in the Global Wind Energy Recycling Market by providing sustainable solutions for managing the end-of-life of wind turbine components. These methods help reduce waste, conserve resources, and minimize the environmental impact of decommissioned wind turbines. As the demand for wind energy continues to grow, the development and implementation of efficient recycling technologies will be essential for promoting a circular economy and ensuring the sustainability of the wind energy sector.

Global Wind Energy Recycling Market Outlook:

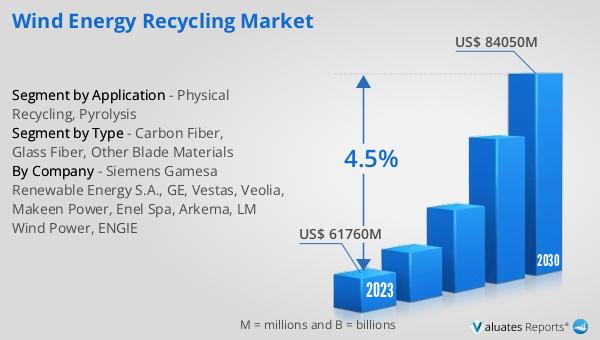

The global Wind Energy Recycling market was valued at US$ 61,760 million in 2023 and is anticipated to reach US$ 84,050 million by 2030, witnessing a compound annual growth rate (CAGR) of 4.5% during the forecast period from 2024 to 2030. This significant growth reflects the increasing emphasis on sustainable practices and the need to manage the lifecycle of wind turbine components effectively. As wind energy becomes a more prominent source of renewable energy worldwide, the importance of recycling wind turbine components, particularly blades, has become more apparent. The market's growth is driven by advancements in recycling technologies, stringent environmental regulations, and the growing awareness of the environmental impact of decommissioned wind turbines. The recycling process involves breaking down wind turbine components into reusable materials, thereby reducing waste and promoting environmental sustainability. The Global Wind Energy Recycling Market encompasses various technologies and methods to recycle different parts of wind turbines, including blades, towers, and nacelles. The goal is to minimize the environmental impact of decommissioned wind turbines and to create a circular economy where materials are continuously reused. This market outlook highlights the potential for significant growth and the increasing importance of sustainable practices within the energy sector.

| Report Metric | Details |

| Report Name | Wind Energy Recycling Market |

| Accounted market size in 2023 | US$ 61760 million |

| Forecasted market size in 2030 | US$ 84050 million |

| CAGR | 4.5% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Siemens Gamesa Renewable Energy S.A., GE, Vestas, Veolia, Makeen Power, Enel Spa, Arkema, LM Wind Power, ENGIE |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |