What is Global Reusable Serological Pipets Market?

The Global Reusable Serological Pipets Market refers to the worldwide industry focused on the production, distribution, and utilization of reusable serological pipets. These pipets are essential laboratory tools used for accurately measuring and transferring liquids in various scientific and medical applications. Unlike disposable pipets, reusable serological pipets are designed for multiple uses, making them a cost-effective and environmentally friendly option. They are typically made from durable materials such as glass or high-quality plastics that can withstand repeated sterilization processes. The market encompasses a wide range of pipet sizes and types, catering to different needs in research, clinical diagnostics, and industrial laboratories. The demand for reusable serological pipets is driven by the growing emphasis on sustainability, cost reduction, and the increasing volume of research activities across the globe. As laboratories seek to minimize waste and operational costs, the adoption of reusable pipets is expected to rise, further propelling the market's growth.

1-2ml, 5ml, 10 ml, 25 ml, Other in the Global Reusable Serological Pipets Market:

In the Global Reusable Serological Pipets Market, pipets are available in various sizes, including 1-2ml, 5ml, 10ml, 25ml, and other capacities, each serving specific purposes in laboratory settings. The 1-2ml pipets are commonly used for precise measurements of small liquid volumes, making them ideal for tasks that require high accuracy, such as enzyme assays, cell culture media preparation, and small-scale chemical reactions. These pipets are favored in research and clinical laboratories where precision is paramount. The 5ml pipets are versatile and widely used for a range of applications, including sample preparation, reagent addition, and routine laboratory procedures. Their moderate capacity makes them suitable for both small and medium-scale experiments, providing a balance between precision and volume. The 10ml pipets are often employed in experiments that require larger volumes of liquids, such as preparing culture media, diluting samples, and conducting biochemical assays. Their larger capacity allows for efficient handling of more substantial liquid quantities without compromising accuracy. The 25ml pipets are typically used in industrial and research laboratories for tasks that involve significant liquid volumes, such as large-scale cell culture, bulk reagent preparation, and extensive sample dilutions. These pipets are essential for processes that demand high throughput and efficiency. Additionally, the market includes other pipet sizes that cater to specific needs, such as 50ml or custom capacities, providing flexibility for specialized applications. The availability of various pipet sizes ensures that laboratories can choose the appropriate tool for their specific requirements, enhancing the efficiency and accuracy of their workflows. The diverse range of reusable serological pipets in the market underscores the importance of having the right tools for different laboratory tasks, contributing to the overall advancement of scientific research and industrial processes.

Tissue Culture, Bacterial Culture, Testing Laboratory, Other in the Global Reusable Serological Pipets Market:

The Global Reusable Serological Pipets Market finds extensive usage in several key areas, including tissue culture, bacterial culture, testing laboratories, and other specialized applications. In tissue culture, reusable serological pipets are indispensable for the preparation and maintenance of cell cultures. They are used to transfer cell suspensions, add growth media, and perform serial dilutions, ensuring the precise handling of delicate cell lines. The accuracy and reliability of these pipets are crucial for maintaining the integrity of cell cultures, which are essential for research in fields such as cancer biology, regenerative medicine, and drug development. In bacterial culture, reusable serological pipets play a vital role in inoculating media, transferring bacterial suspensions, and performing dilutions for colony counting. The ability to accurately measure and transfer small volumes of bacterial cultures is essential for microbiological studies, antibiotic testing, and the production of bacterial-based products. Testing laboratories, which conduct a wide range of diagnostic and analytical tests, rely on reusable serological pipets for sample preparation, reagent addition, and precise liquid handling. These pipets are used in clinical diagnostics, environmental testing, food safety analysis, and pharmaceutical quality control, among other areas. Their reusability and accuracy make them a cost-effective and reliable choice for high-throughput testing environments. Other specialized applications of reusable serological pipets include their use in chemical synthesis, where precise liquid measurements are critical for reaction setups, and in academic research laboratories, where they support a variety of experimental protocols. The versatility and durability of reusable serological pipets make them a valuable tool across diverse scientific disciplines, contributing to the advancement of research and the development of new technologies.

Global Reusable Serological Pipets Market Outlook:

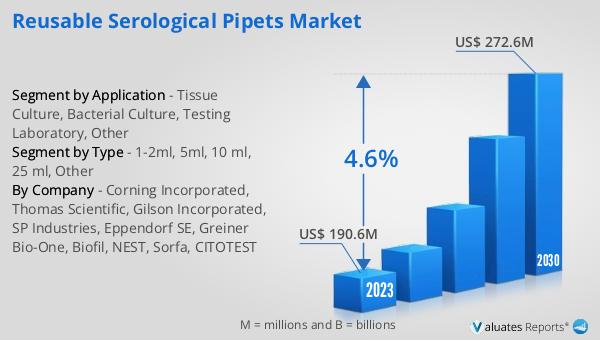

The global market for Reusable Serological Pipets was valued at US$ 190.6 million in 2023 and is projected to reach US$ 272.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.6% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for reusable pipets driven by factors such as cost-efficiency, sustainability, and the expanding scope of scientific research. Additionally, the broader medical devices market, which encompasses reusable serological pipets, is estimated to be worth US$ 603 billion in 2023 and is expected to grow at a CAGR of 5% over the next six years. This substantial market size highlights the significant role that reusable serological pipets play within the medical and scientific communities. The rising adoption of these pipets is attributed to their ability to reduce waste and operational costs, making them an attractive option for laboratories worldwide. As research activities continue to expand and the focus on sustainable practices intensifies, the demand for reusable serological pipets is anticipated to grow, further driving the market's development.

| Report Metric | Details |

| Report Name | Reusable Serological Pipets Market |

| Accounted market size in 2023 | US$ 190.6 million |

| Forecasted market size in 2030 | US$ 272.6 million |

| CAGR | 4.6% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Corning Incorporated, Thomas Scientific, Gilson Incorporated, SP Industries, Eppendorf SE, Greiner Bio-One, Biofil, NEST, Sorfa, CITOTEST |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |