What is Global Eco-Friendly Cutting Fluid Market?

The Global Eco-Friendly Cutting Fluid Market refers to the industry focused on producing and distributing cutting fluids that are environmentally friendly. Cutting fluids, also known as coolants or lubricants, are used in various machining processes to cool and lubricate the cutting tool and the workpiece. Traditional cutting fluids often contain harmful chemicals that can be detrimental to both the environment and human health. In contrast, eco-friendly cutting fluids are formulated with biodegradable and non-toxic ingredients, reducing their environmental impact. These fluids are designed to provide effective cooling and lubrication while minimizing the release of hazardous substances. The market for these eco-friendly alternatives is growing as industries become more conscious of their environmental footprint and seek sustainable solutions. This shift is driven by stringent environmental regulations, increasing awareness about the benefits of green products, and the rising demand for sustainable manufacturing practices. As a result, the Global Eco-Friendly Cutting Fluid Market is gaining traction across various sectors, including automotive, aerospace, electronics, and general manufacturing, where precision and sustainability are paramount.

Straight Oil, Water in the Global Eco-Friendly Cutting Fluid Market:

Straight oil and water-based cutting fluids are two primary types of eco-friendly cutting fluids used in the Global Eco-Friendly Cutting Fluid Market. Straight oils are typically composed of mineral or synthetic oils and are used in applications where high lubrication is required. These oils provide excellent lubrication properties, reducing friction and wear on cutting tools, which extends their lifespan. Straight oils are particularly effective in heavy-duty machining operations, such as turning, milling, and drilling of hard metals. However, they can be less effective in cooling compared to water-based fluids and may require additional measures to manage heat. On the other hand, water-based cutting fluids, also known as soluble oils, semi-synthetic, or synthetic fluids, are formulated by mixing water with oil or other additives. These fluids offer superior cooling properties due to the high thermal conductivity of water, making them ideal for high-speed machining operations where heat dissipation is critical. Water-based fluids are also more environmentally friendly as they are easier to dispose of and less likely to cause environmental contamination. They are commonly used in applications such as grinding, where precise temperature control is essential to prevent thermal damage to the workpiece. Both straight oils and water-based fluids have their advantages and are chosen based on the specific requirements of the machining process. The trend towards eco-friendly cutting fluids in the market is driven by the need to balance performance with environmental sustainability, ensuring that industries can achieve high-quality machining results while minimizing their ecological impact.

Mechanical, The Automobile, 3C Electronic, Other in the Global Eco-Friendly Cutting Fluid Market:

The usage of eco-friendly cutting fluids in various industries such as mechanical, automotive, 3C electronics, and others is becoming increasingly prevalent due to their environmental benefits and performance advantages. In the mechanical industry, eco-friendly cutting fluids are used extensively in machining processes like turning, milling, drilling, and grinding. These fluids help in reducing tool wear, improving surface finish, and enhancing the overall efficiency of the machining process. The use of biodegradable and non-toxic cutting fluids ensures that the waste generated during machining does not harm the environment, aligning with the industry's push towards sustainable manufacturing practices. In the automotive industry, eco-friendly cutting fluids play a crucial role in the production of various components such as engine parts, transmission systems, and chassis components. The high lubrication and cooling properties of these fluids help in achieving precise machining tolerances and extending the life of cutting tools, which is essential for maintaining the quality and reliability of automotive parts. The shift towards eco-friendly cutting fluids in the automotive sector is also driven by stringent environmental regulations and the industry's commitment to reducing its carbon footprint. In the 3C electronics industry, which includes computers, communications, and consumer electronics, eco-friendly cutting fluids are used in the manufacturing of electronic components and devices. The high precision required in the machining of electronic parts necessitates the use of cutting fluids that can provide effective cooling and lubrication without causing any contamination. Eco-friendly cutting fluids meet these requirements while also ensuring that the manufacturing process is environmentally sustainable. Other industries, such as aerospace, medical devices, and general manufacturing, also benefit from the use of eco-friendly cutting fluids. In aerospace, the high-performance requirements of aircraft components demand cutting fluids that can provide excellent lubrication and cooling while being safe for the environment. In the medical device industry, the use of non-toxic and biodegradable cutting fluids is crucial to ensure that the manufacturing process does not introduce any harmful substances into medical products. Overall, the adoption of eco-friendly cutting fluids across various industries is driven by the need to achieve high-quality machining results while minimizing environmental impact.

Global Eco-Friendly Cutting Fluid Market Outlook:

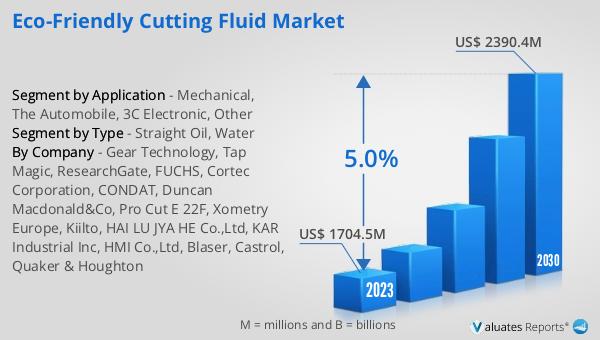

The global market for eco-friendly cutting fluids was valued at approximately $1,704.5 million in 2023. Projections indicate that this market is expected to grow significantly, reaching around $2,390.4 million by the year 2030. This growth is anticipated to occur at a compound annual growth rate (CAGR) of 5.0% during the forecast period from 2024 to 2030. This upward trend reflects the increasing demand for sustainable and environmentally friendly solutions in various industries. As companies and manufacturers become more aware of the environmental impact of their operations, the shift towards eco-friendly cutting fluids is gaining momentum. This market growth is also driven by stringent environmental regulations and the need for industries to adopt greener practices. The rising awareness about the benefits of using eco-friendly cutting fluids, such as reduced environmental contamination and improved worker safety, is further propelling the market forward. As a result, the Global Eco-Friendly Cutting Fluid Market is poised for substantial growth in the coming years, reflecting a broader trend towards sustainability and environmental responsibility in industrial processes.

| Report Metric | Details |

| Report Name | Eco-Friendly Cutting Fluid Market |

| Accounted market size in 2023 | US$ 1704.5 million |

| Forecasted market size in 2030 | US$ 2390.4 million |

| CAGR | 5.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Gear Technology, Tap Magic, ResearchGate, FUCHS, Cortec Corporation, CONDAT, Duncan Macdonald&Co, Pro Cut E 22F, Xometry Europe, Kiilto, HAI LU JYA HE Co.,Ltd, KAR Industrial Inc, HMI Co.,Ltd, Blaser, Castrol, Quaker & Houghton |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |