What is Global Anti-stick Surface Market?

The Global Anti-stick Surface Market refers to the industry focused on the production and application of materials that prevent substances from sticking to surfaces. These materials are crucial in various industries, including cookware, food processing, textiles, electronics, and medical devices. The primary function of anti-stick surfaces is to enhance the efficiency and longevity of products by reducing the need for cleaning and maintenance. These surfaces are typically coated with specialized chemicals or materials that create a non-stick layer, making it easier to remove residues and preventing the buildup of unwanted substances. The market for these surfaces is driven by the demand for high-performance, durable, and easy-to-clean products. Innovations in material science and coating technologies have expanded the applications of anti-stick surfaces, making them an integral part of modern manufacturing and consumer goods. The global market is characterized by a diverse range of products and applications, catering to both industrial and consumer needs.

PTFE, PFA, FEP, Others in the Global Anti-stick Surface Market:

Polytetrafluoroethylene (PTFE), Perfluoroalkoxy alkane (PFA), Fluorinated ethylene propylene (FEP), and other materials are pivotal in the Global Anti-stick Surface Market. PTFE, commonly known by the brand name Teflon, is renowned for its exceptional non-stick properties, high-temperature resistance, and chemical inertness. It is widely used in cookware, industrial applications, and medical devices due to its ability to withstand extreme conditions without degrading. PFA, another fluoropolymer, offers similar non-stick characteristics but with enhanced mechanical strength and flexibility. This makes it suitable for applications requiring more robust performance, such as in chemical processing equipment and high-performance electrical insulation. FEP, on the other hand, combines the non-stick properties of PTFE with improved transparency and flexibility, making it ideal for applications in the food processing industry, where visibility and flexibility are crucial. Other materials in the anti-stick surface market include silicone and ceramic coatings, which provide alternative solutions for specific applications. Silicone coatings are known for their heat resistance and flexibility, making them suitable for bakeware and kitchen utensils. Ceramic coatings, while not as non-stick as fluoropolymers, offer excellent durability and scratch resistance, making them a popular choice for high-end cookware. Each of these materials brings unique properties to the table, allowing manufacturers to select the most appropriate solution for their specific needs. The versatility and performance of these materials have made them indispensable in the development of advanced anti-stick surfaces, driving innovation and growth in the market.

Cookware, Food Processing, Fabrics and Carpet, Electrical Appliance, Medical, Others in the Global Anti-stick Surface Market:

The Global Anti-stick Surface Market finds extensive usage across various sectors, including cookware, food processing, fabrics and carpet, electrical appliances, medical, and others. In the cookware industry, anti-stick surfaces are essential for creating non-stick pots, pans, and baking sheets, which make cooking and cleaning easier and more efficient. These surfaces prevent food from sticking, reducing the need for excessive oil or butter, and ensuring even cooking. In food processing, anti-stick coatings are applied to machinery and equipment to prevent food residues from adhering to surfaces, thereby enhancing hygiene and reducing downtime for cleaning. This is particularly important in industries such as baking, confectionery, and meat processing, where cleanliness and efficiency are paramount. In the textile industry, anti-stick coatings are used on fabrics and carpets to repel stains and liquids, making them easier to clean and maintain. This extends the lifespan of the products and enhances their aesthetic appeal. Electrical appliances, such as irons and hair straighteners, also benefit from anti-stick surfaces, which prevent materials from sticking and ensure smooth operation. In the medical field, anti-stick coatings are applied to surgical instruments, catheters, and other medical devices to reduce friction and prevent the buildup of biological materials, thereby improving patient outcomes and reducing the risk of infections. Other applications of anti-stick surfaces include automotive parts, where they reduce friction and wear, and consumer electronics, where they enhance the durability and performance of devices. The widespread use of anti-stick surfaces across these diverse sectors underscores their importance in modern manufacturing and consumer products.

Global Anti-stick Surface Market Outlook:

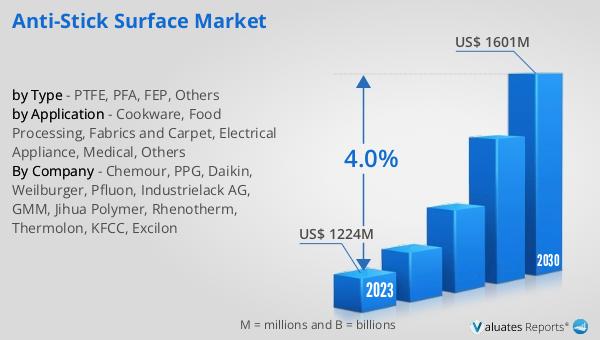

The global Anti-stick Surface market was valued at $1,224 million in 2023 and is projected to grow to $1,601 million by 2030, reflecting a compound annual growth rate (CAGR) of 4.0% during the forecast period from 2024 to 2030. This growth is driven by the increasing demand for high-performance, durable, and easy-to-clean products across various industries. The market's expansion is also fueled by advancements in material science and coating technologies, which have broadened the range of applications for anti-stick surfaces. As industries continue to seek innovative solutions to enhance the efficiency and longevity of their products, the demand for anti-stick surfaces is expected to rise. The market's growth trajectory indicates a robust and sustained interest in these materials, highlighting their critical role in modern manufacturing and consumer goods. The projected increase in market value underscores the importance of anti-stick surfaces in meeting the evolving needs of industries and consumers alike.

| Report Metric | Details |

| Report Name | Anti-stick Surface Market |

| Accounted market size in 2023 | US$ 1224 million |

| Forecasted market size in 2030 | US$ 1601 million |

| CAGR | 4.0% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Chemour, PPG, Daikin, Weilburger, Pfluon, Industrielack AG, GMM, Jihua Polymer, Rhenotherm, Thermolon, KFCC, Excilon |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |