What is Global Optical Encapsulation Adhesive Market?

The Global Optical Encapsulation Adhesive Market refers to the industry focused on the production and distribution of adhesives used to encapsulate optical components. These adhesives are crucial in protecting sensitive optical elements from environmental factors such as moisture, dust, and mechanical stress. They ensure the longevity and reliability of optical devices by providing a protective barrier that maintains the integrity of the encapsulated components. The market encompasses a wide range of adhesive types, including heat curing and UV curing adhesives, each with specific properties tailored to different applications. The demand for these adhesives is driven by the growing use of optical components in various industries, including telecommunications, electronics, and medical devices. As technology advances and the need for high-performance optical devices increases, the Global Optical Encapsulation Adhesive Market is expected to continue its growth trajectory, offering innovative solutions to meet the evolving needs of these industries.

Heat Curing, UV Curing in the Global Optical Encapsulation Adhesive Market:

Heat curing and UV curing are two primary methods used in the Global Optical Encapsulation Adhesive Market. Heat curing adhesives require the application of heat to initiate the curing process, which involves a chemical reaction that transforms the adhesive from a liquid or semi-liquid state to a solid state. This type of adhesive is known for its strong bonding capabilities and resistance to high temperatures, making it ideal for applications where durability and thermal stability are critical. Heat curing adhesives are commonly used in the semiconductor industry, where they provide robust encapsulation for delicate components that operate under high thermal conditions. On the other hand, UV curing adhesives rely on ultraviolet light to trigger the curing process. These adhesives contain photoinitiators that react when exposed to UV light, causing the adhesive to harden rapidly. UV curing adhesives offer several advantages, including fast curing times, which enhance production efficiency, and the ability to cure at room temperature, which is beneficial for temperature-sensitive applications. They are widely used in the manufacturing of fiber optic devices, where precise and quick bonding is essential. Both heat curing and UV curing adhesives play a vital role in the Global Optical Encapsulation Adhesive Market, catering to the diverse needs of various industries by providing reliable and efficient encapsulation solutions.

Semiconductor, Fiber Optic Device, Hybrid Circuit, Electronic Assembly, Medical Instruments in the Global Optical Encapsulation Adhesive Market:

The Global Optical Encapsulation Adhesive Market finds extensive usage across several key areas, including semiconductors, fiber optic devices, hybrid circuits, electronic assemblies, and medical instruments. In the semiconductor industry, these adhesives are used to encapsulate delicate components, providing protection against environmental factors and ensuring the longevity and reliability of the devices. The adhesives help in maintaining the performance of semiconductors by preventing contamination and mechanical damage. In fiber optic devices, optical encapsulation adhesives are crucial for securing and protecting the delicate fibers and connectors. They ensure that the optical signals are transmitted without interference, maintaining the integrity and efficiency of the communication systems. Hybrid circuits, which combine different types of electronic components on a single substrate, also benefit from these adhesives. They provide a protective layer that shields the components from environmental stress and mechanical damage, ensuring the stability and performance of the circuits. In electronic assemblies, optical encapsulation adhesives are used to protect sensitive components from moisture, dust, and mechanical stress. They help in maintaining the functionality and reliability of electronic devices, especially in harsh environments. In the medical instruments sector, these adhesives are used to encapsulate optical components in devices such as endoscopes and imaging equipment. They ensure the clarity and precision of the optical elements, which is crucial for accurate diagnostics and treatment. Overall, the Global Optical Encapsulation Adhesive Market plays a vital role in enhancing the performance and reliability of various high-tech devices across multiple industries.

Global Optical Encapsulation Adhesive Market Outlook:

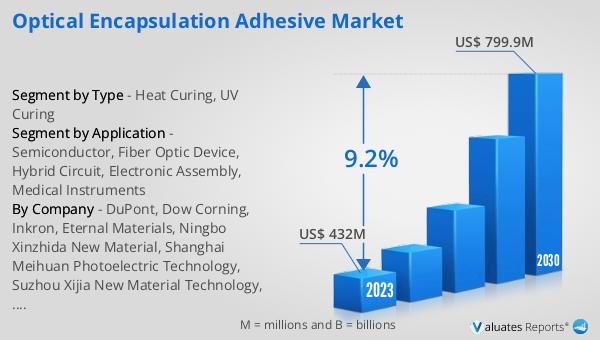

The global Optical Encapsulation Adhesive market was valued at US$ 432 million in 2023 and is anticipated to reach US$ 799.9 million by 2030, witnessing a CAGR of 9.2% during the forecast period 2024-2030. The global market for semiconductors was estimated at US$ 579 billion in the year 2022 and is projected to reach US$ 790 billion by 2029, growing at a CAGR of 6% during the forecast period. This significant growth in both markets underscores the increasing demand for advanced materials and technologies that enhance the performance and reliability of electronic and optical devices. The rising adoption of optical encapsulation adhesives in various applications, including semiconductors, fiber optic devices, hybrid circuits, electronic assemblies, and medical instruments, is a testament to their critical role in modern technology. As industries continue to innovate and develop more sophisticated devices, the need for high-quality encapsulation adhesives is expected to grow, driving the expansion of the Global Optical Encapsulation Adhesive Market.

| Report Metric | Details |

| Report Name | Optical Encapsulation Adhesive Market |

| Accounted market size in 2023 | US$ 432 million |

| Forecasted market size in 2030 | US$ 799.9 million |

| CAGR | 9.2% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | DuPont, Dow Corning, Inkron, Eternal Materials, Ningbo Xinzhida New Material, Shanghai Meihuan Photoelectric Technology, Suzhou Xijia New Material Technology, Zhejiang Guoneng Technology, Guangzhou Human Chemicals, Hefei Jingcheng Technology, Momentive, Henkel, Master Bond, Intertronics |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |