What is Global TOC Analyzers Market?

The Global TOC Analyzers Market refers to the worldwide industry focused on the production, distribution, and utilization of Total Organic Carbon (TOC) analyzers. These devices are essential for measuring the amount of organic carbon present in a sample, which is crucial for various applications, including environmental monitoring, water treatment, and pharmaceutical manufacturing. TOC analyzers help in ensuring the quality and safety of water by detecting contaminants and organic pollutants. The market encompasses a range of TOC analyzers, including benchtop, portable, and online models, each designed to meet specific needs and applications. The increasing awareness about water quality and stringent regulatory standards are driving the demand for TOC analyzers globally. As industries and municipalities strive to comply with environmental regulations and ensure the safety of water supplies, the adoption of TOC analyzers is expected to grow. The market is characterized by technological advancements, with manufacturers continuously innovating to offer more accurate, reliable, and user-friendly devices.

Benchtop, Portable, Online in the Global TOC Analyzers Market:

Benchtop, portable, and online TOC analyzers each serve distinct purposes within the Global TOC Analyzers Market. Benchtop TOC analyzers are typically used in laboratory settings where precise and detailed analysis is required. These devices are known for their high accuracy and ability to handle a wide range of sample types, making them ideal for research and quality control applications. They are often equipped with advanced features such as automated sample handling and sophisticated software for data analysis, which enhance their functionality and ease of use. Portable TOC analyzers, on the other hand, are designed for field use, providing the flexibility to conduct on-site testing. These analyzers are compact, lightweight, and battery-operated, making them convenient for environmental monitoring, industrial inspections, and emergency response situations. Despite their smaller size, portable TOC analyzers are capable of delivering reliable and accurate results, enabling users to make informed decisions quickly. Online TOC analyzers are integrated into industrial processes and water treatment systems to provide continuous, real-time monitoring of organic carbon levels. These analyzers are essential for maintaining compliance with regulatory standards and ensuring the efficiency of water treatment processes. Online TOC analyzers are designed to withstand harsh industrial environments and offer features such as remote monitoring and automated calibration, which reduce the need for manual intervention and enhance operational efficiency. The choice between benchtop, portable, and online TOC analyzers depends on the specific requirements of the application, including the need for mobility, the level of accuracy required, and the nature of the environment in which the analyzer will be used. Each type of TOC analyzer plays a crucial role in the broader context of water quality management and environmental protection, contributing to the overall growth and development of the Global TOC Analyzers Market.

High Purity Water, Water for Injection, Drinking or Source Water, Industrial Waste Effluent, Other in the Global TOC Analyzers Market:

The usage of TOC analyzers in various areas such as high purity water, water for injection, drinking or source water, industrial waste effluent, and other applications highlights their versatility and importance. In the context of high purity water, TOC analyzers are critical for industries such as pharmaceuticals and semiconductors, where even trace amounts of organic contaminants can compromise product quality and safety. These analyzers ensure that the water used in manufacturing processes meets stringent purity standards, thereby preventing contamination and ensuring the integrity of the final product. For water for injection (WFI), which is used in medical and pharmaceutical applications, TOC analyzers play a vital role in verifying that the water is free from organic impurities that could pose health risks. The ability to accurately measure TOC levels in WFI is essential for maintaining compliance with regulatory standards and ensuring patient safety. In the realm of drinking or source water, TOC analyzers help municipalities and water treatment facilities monitor and control the quality of water supplied to the public. By detecting organic pollutants, these analyzers enable timely interventions to prevent contamination and protect public health. In industrial waste effluent, TOC analyzers are used to monitor and manage the discharge of organic pollutants into the environment. Industries are required to comply with environmental regulations that limit the amount of organic carbon in their effluent, and TOC analyzers provide the necessary data to ensure compliance. This application is particularly significant as it helps prevent environmental pollution and promotes sustainable industrial practices. Other applications of TOC analyzers include monitoring the quality of water in cooling towers, boilers, and other industrial systems where organic contamination can affect performance and efficiency. Overall, the diverse applications of TOC analyzers underscore their importance in maintaining water quality across various sectors, contributing to environmental protection, public health, and industrial efficiency.

Global TOC Analyzers Market Outlook:

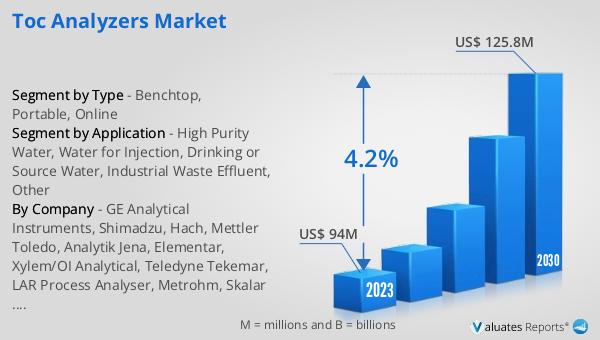

The global TOC Analyzers market is anticipated to grow significantly, with projections indicating it will reach approximately US$ 125.8 million by 2030, up from an estimated US$ 98.3 million in 2024, reflecting a compound annual growth rate (CAGR) of 4.2% during the period from 2024 to 2030. Leading companies in this market, such as GE, Shimadzu, and Hach, collectively account for 42% of the market volume, showcasing their dominance and influence in the industry. Among the various applications of TOC analyzers, industrial waste effluent stands out as the largest segment, representing 40% of the market share. This significant share highlights the critical role of TOC analyzers in monitoring and managing organic pollutants in industrial wastewater, ensuring compliance with environmental regulations and promoting sustainable industrial practices. The growth of the TOC analyzers market is driven by increasing awareness about water quality, stringent regulatory standards, and the need for accurate and reliable monitoring solutions across various industries. As the demand for clean and safe water continues to rise, the adoption of TOC analyzers is expected to expand, further solidifying their importance in water quality management and environmental protection.

| Report Metric | Details |

| Report Name | TOC Analyzers Market |

| Accounted market size in 2024 | an estimated US$ 98.3 million |

| Forecasted market size in 2030 | US$ 125.8 million |

| CAGR | 4.2% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | GE Analytical Instruments, Shimadzu, Hach, Mettler Toledo, Analytik Jena, Elementar, Xylem/OI Analytical, Teledyne Tekemar, LAR Process Analyser, Metrohm, Skalar Analytical, Comet, Tailin |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |