What is Global Ski Clothing Market?

The global ski clothing market encompasses a wide range of apparel designed specifically for skiing and other snow sports. This market includes various types of clothing such as jackets, pants, one-piece suits, and accessories that are essential for skiers to stay warm, dry, and comfortable in cold and snowy conditions. The market is driven by factors such as the increasing popularity of skiing as a recreational activity, advancements in fabric technology, and the growing awareness of the importance of proper ski attire for safety and performance. Ski clothing is designed to provide insulation, waterproofing, and breathability, ensuring that skiers can enjoy their time on the slopes without being hindered by the elements. The market caters to a diverse range of consumers, from amateur skiers to professional athletes, and includes products at various price points to accommodate different budgets. As skiing continues to gain popularity worldwide, the demand for high-quality ski clothing is expected to grow, making this market an important segment of the broader outdoor apparel industry.

Jacket, Pants, One-Piece Suits in the Global Ski Clothing Market:

Jackets, pants, and one-piece suits are the primary categories of products in the global ski clothing market. Jackets are the most common type of ski clothing, accounting for a significant share of the market. They are designed to provide warmth, protection from wind and snow, and breathability to prevent overheating. Ski jackets often feature multiple layers, including an outer shell that is waterproof and windproof, and an inner layer that provides insulation. They also come with various features such as adjustable hoods, cuffs, and ventilation zippers to enhance comfort and functionality. Pants are another essential component of ski clothing, designed to keep the lower body warm and dry. Like jackets, ski pants are made from waterproof and breathable materials and often include insulation for added warmth. They typically feature reinforced knees and seat areas to withstand the wear and tear of skiing, as well as adjustable waistbands and gaiters to keep snow out. One-piece suits, also known as ski suits, offer full-body protection and are popular among both amateur and professional skiers. These suits combine the features of jackets and pants into a single garment, providing seamless coverage and eliminating the risk of snow getting in between layers. One-piece suits are particularly favored in extremely cold conditions or for activities that involve a lot of movement, as they offer maximum warmth and flexibility. In addition to these main categories, the ski clothing market also includes accessories such as gloves, hats, and base layers, which are essential for complete protection and comfort on the slopes. Overall, the variety of products available in the ski clothing market ensures that skiers can find the right gear to suit their needs and preferences, whether they are hitting the slopes for the first time or competing at a professional level.

Amateurs, Professional Athletes, Others in the Global Ski Clothing Market:

The global ski clothing market serves a wide range of users, including amateurs, professional athletes, and others who engage in snow sports. Amateurs, who make up the largest segment of the market, include recreational skiers and beginners who ski occasionally or as a hobby. For these users, ski clothing is primarily about comfort, warmth, and affordability. They often look for products that offer good value for money, with features such as waterproofing, insulation, and breathability. Many amateur skiers also prioritize style and fashion, choosing ski clothing that looks good both on and off the slopes. Professional athletes, on the other hand, have more specific and demanding requirements for their ski clothing. These users need gear that can withstand the rigors of competitive skiing, providing maximum performance, durability, and protection. Professional ski clothing often incorporates advanced materials and technologies, such as high-performance insulation, moisture-wicking fabrics, and ergonomic designs that enhance mobility and reduce drag. These athletes also require clothing that meets the regulations and standards of their sport, ensuring that they can compete at the highest level. In addition to amateurs and professional athletes, the ski clothing market also caters to other users, such as ski instructors, resort staff, and outdoor enthusiasts who engage in activities like snowboarding, snowshoeing, and winter hiking. These users need versatile and durable clothing that can handle a variety of conditions and activities. For example, ski instructors may require clothing that is both professional-looking and functional, with features like multiple pockets for carrying tools and accessories. Resort staff, who spend long hours outdoors in varying weather conditions, need clothing that provides reliable protection and comfort throughout their shifts. Outdoor enthusiasts, meanwhile, look for gear that can transition seamlessly between different activities, offering the right balance of warmth, breathability, and flexibility. Overall, the global ski clothing market caters to a diverse range of users, each with their own unique needs and preferences. By offering a wide variety of products and features, the market ensures that everyone can find the right gear to enjoy their time in the snow.

Global Ski Clothing Market Outlook:

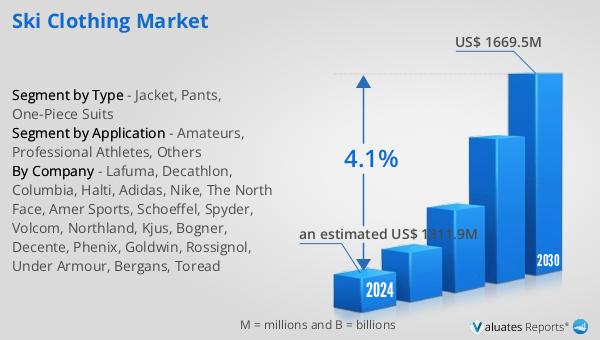

The global ski clothing market is anticipated to grow significantly, with projections indicating it will reach approximately US$ 1669.5 million by 2030, up from an estimated US$ 1311.9 million in 2024. This growth is expected to occur at a compound annual growth rate (CAGR) of 4.1% between 2024 and 2030. Europe stands out as the largest market for ski clothing, holding a share of over 29%. Among the various products available, jackets are the most prevalent, accounting for more than 58% of the market share. When it comes to the application of ski clothing, amateurs represent the largest segment, with a share exceeding 74%. This data highlights the significant demand for ski clothing among recreational skiers and the importance of jackets as a key product category within the market. The growth of the ski clothing market is driven by factors such as the increasing popularity of skiing as a recreational activity, advancements in fabric technology, and the growing awareness of the importance of proper ski attire for safety and performance. As skiing continues to gain popularity worldwide, the demand for high-quality ski clothing is expected to grow, making this market an important segment of the broader outdoor apparel industry.

| Report Metric | Details |

| Report Name | Ski Clothing Market |

| Accounted market size in 2024 | an estimated US$ 1311.9 million |

| Forecasted market size in 2030 | US$ 1669.5 million |

| CAGR | 4.1% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Lafuma, Decathlon, Columbia, Halti, Adidas, Nike, The North Face, Amer Sports, Schoeffel, Spyder, Volcom, Northland, Kjus, Bogner, Decente, Phenix, Goldwin, Rossignol, Under Armour, Bergans, Toread |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |