What is Global Urea Formaldehyde Concentrate (UFC) Market?

The Global Urea Formaldehyde Concentrate (UFC) Market is a significant segment within the chemical industry, primarily driven by its extensive use in various applications such as adhesives, resins, and fertilizers. Urea Formaldehyde Concentrate (UFC) is a solution of urea and formaldehyde, which is used as a raw material in the production of urea-formaldehyde resins. These resins are widely used in the manufacture of particleboard, plywood, and other wood-based products due to their strong adhesive properties. The market for UFC is influenced by the demand from the construction and furniture industries, which utilize these resins extensively. Additionally, UFC is used in the agricultural sector as a nitrogen-release fertilizer, which helps in enhancing crop yield. The global market for UFC is characterized by the presence of several key players who contribute to the production and distribution of this chemical compound. The market dynamics are shaped by factors such as raw material availability, technological advancements, and regulatory policies. As industries continue to grow and evolve, the demand for UFC is expected to remain steady, driven by its versatile applications and the ongoing need for efficient and cost-effective solutions in various sectors.

UFC 85, UFC 80, UFC 75, Others in the Global Urea Formaldehyde Concentrate (UFC) Market:

UFC 85, UFC 80, and UFC 75 are different grades of Urea Formaldehyde Concentrate, each with varying concentrations of urea and formaldehyde. UFC 85, which contains 85% urea and formaldehyde, is the most concentrated form and is widely used in the production of high-performance resins. These resins are essential in the manufacture of durable and robust wood-based products such as particleboard and plywood. The high concentration of UFC 85 ensures that the resins produced have superior adhesive properties, making them ideal for applications that require strong bonding and structural integrity. UFC 80, with an 80% concentration, is slightly less concentrated than UFC 85 but still finds extensive use in the production of resins and adhesives. It offers a balance between performance and cost, making it a popular choice for manufacturers looking to optimize their production processes. UFC 75, containing 75% urea and formaldehyde, is the least concentrated among the three but is still valuable in various industrial applications. It is often used in the production of resins for lower-end applications where the highest performance is not a critical requirement. Apart from these three main grades, there are other variations of UFC available in the market, each tailored to meet specific industrial needs. These variations may include different concentrations or additional components to enhance certain properties of the resins produced. The choice of UFC grade depends on the specific requirements of the application, the desired properties of the end product, and cost considerations. The versatility of UFC in its various forms makes it a crucial component in the chemical industry, catering to a wide range of applications and industries.

UF Resins, Fertilizers, Others in the Global Urea Formaldehyde Concentrate (UFC) Market:

The usage of Global Urea Formaldehyde Concentrate (UFC) Market spans across several key areas, including UF Resins, Fertilizers, and other applications. In the production of UF Resins, UFC is a critical raw material. UF Resins are widely used in the manufacture of wood-based products such as particleboard, plywood, and medium-density fiberboard (MDF). These resins provide excellent adhesive properties, ensuring strong bonding and structural integrity of the wood products. The construction and furniture industries are major consumers of UF Resins, driving the demand for UFC. The high-performance characteristics of UF Resins, such as durability, moisture resistance, and cost-effectiveness, make them a preferred choice in these industries. In the agricultural sector, UFC is used as a nitrogen-release fertilizer. Nitrogen is a vital nutrient for plant growth, and UFC-based fertilizers provide a controlled release of nitrogen, enhancing crop yield and productivity. The use of UFC in fertilizers helps in improving soil fertility and promoting healthy plant growth. This application is particularly important in regions with intensive agricultural activities, where efficient and effective fertilization is crucial for sustaining crop production. Apart from UF Resins and Fertilizers, UFC finds applications in other areas as well. It is used in the production of coatings, adhesives, and sealants, where its strong bonding properties and chemical stability are highly valued. UFC is also utilized in the textile industry for fabric finishing and in the paper industry for paper coating and sizing. The versatility of UFC in various applications highlights its importance in the chemical industry. Its ability to enhance the performance of products, improve efficiency, and provide cost-effective solutions makes it a valuable component in multiple sectors. As industries continue to evolve and innovate, the demand for UFC is expected to remain robust, driven by its wide range of applications and the ongoing need for high-performance materials.

Global Urea Formaldehyde Concentrate (UFC) Market Outlook:

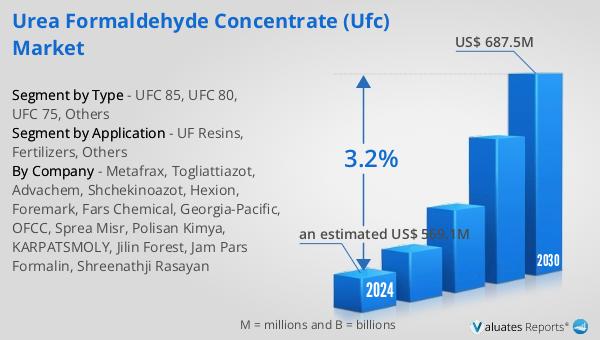

The global Urea Formaldehyde Concentrate (UFC) market is anticipated to grow from an estimated US$ 569.1 million in 2024 to US$ 687.5 million by 2030, reflecting a compound annual growth rate (CAGR) of 3.2% between 2024 and 2030. Key players in the global UFC market include Metafrax, Togliattiazot, Advachem, Shchekinoazot, Hexion, Foremark, Fars Chemical, Georgia-Pacific, OFCC, Sprea Misr, Polisan Kimya, KARPATSMOLY, Jilin Forest, Jam Pars Formalin, and Shreenathji Rasayan, collectively accounting for approximately 70% of the market. Europe holds the largest market share, exceeding 45%. Among the different grades of UFC, UFC 85 is the most dominant, holding a market share of over 85%. The most prevalent application of UFC is in UF resins, which account for more than 76% of the market.

| Report Metric | Details |

| Report Name | Urea Formaldehyde Concentrate (UFC) Market |

| Accounted market size in 2024 | an estimated US$ 569.1 million |

| Forecasted market size in 2030 | US$ 687.5 million |

| CAGR | 3.2% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Metafrax, Togliattiazot, Advachem, Shchekinoazot, Hexion, Foremark, Fars Chemical, Georgia-Pacific, OFCC, Sprea Misr, Polisan Kimya, KARPATSMOLY, Jilin Forest, Jam Pars Formalin, Shreenathji Rasayan |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |