What is Global Electrical Cooktops and Free-standing Ranges Market?

The global Electrical Cooktops and Free-standing Ranges market is a dynamic and rapidly evolving sector within the home appliance industry. Electrical cooktops are kitchen appliances that use electricity to heat and cook food, offering a sleek and modern alternative to traditional gas stoves. Free-standing ranges, on the other hand, combine an oven and a cooktop in a single unit, providing versatility and convenience for both cooking and baking needs. These appliances are becoming increasingly popular due to their ease of use, energy efficiency, and advanced features such as touch controls, precise temperature settings, and safety mechanisms. The market for these products is driven by factors such as rising disposable incomes, urbanization, and the growing trend of smart homes. Consumers are increasingly looking for appliances that not only perform well but also enhance the aesthetic appeal of their kitchens. As a result, manufacturers are focusing on innovation and design to meet the evolving demands of the market.

Electrical Cooktops, Free-standing Ranges in the Global Electrical Cooktops and Free-standing Ranges Market:

Electrical cooktops and free-standing ranges are essential components of modern kitchens, offering a range of features that cater to different cooking needs. Electrical cooktops come in various types, including induction, ceramic, and coil cooktops. Induction cooktops are known for their energy efficiency and fast cooking times, as they use electromagnetic fields to directly heat the cookware. Ceramic cooktops, with their smooth glass surfaces, are easy to clean and provide a sleek look. Coil cooktops, although less common, are durable and cost-effective. Free-standing ranges, which combine an oven and a cooktop, are available in electric, gas, and dual-fuel options. Electric ranges are popular for their even heating and consistent oven temperatures, while gas ranges offer precise control over cooking temperatures. Dual-fuel ranges combine the best of both worlds, with a gas cooktop for precise cooking and an electric oven for even baking. These appliances are designed to meet the diverse needs of consumers, from everyday cooking to gourmet meal preparation. The global market for electrical cooktops and free-standing ranges is characterized by continuous innovation, with manufacturers introducing new features such as smart connectivity, self-cleaning functions, and advanced safety features. As consumers become more conscious of energy efficiency and environmental impact, there is a growing demand for appliances that are not only functional but also eco-friendly.

Household, Commercial in the Global Electrical Cooktops and Free-standing Ranges Market:

The usage of electrical cooktops and free-standing ranges varies significantly between household and commercial settings. In households, these appliances are essential for daily cooking and meal preparation. Electrical cooktops are favored for their ease of use, safety features, and modern design. They are ideal for small kitchens and apartments where space is limited. Free-standing ranges, with their combination of oven and cooktop, offer versatility and convenience, making them a popular choice for family homes. These appliances are designed to cater to a wide range of cooking needs, from simple meals to elaborate dishes. In commercial settings, such as restaurants, hotels, and catering services, the demand for high-performance and durable cooking appliances is paramount. Electrical cooktops and free-standing ranges used in commercial kitchens are built to withstand heavy usage and provide consistent performance. Induction cooktops are particularly popular in commercial kitchens due to their energy efficiency and fast cooking times. They allow chefs to prepare meals quickly and efficiently, which is crucial in a fast-paced environment. Free-standing ranges in commercial settings often come with additional features such as multiple ovens, high-capacity burners, and advanced temperature controls to meet the demands of professional cooking. The global market for these appliances is driven by the need for reliable and efficient cooking solutions in both household and commercial settings. As technology advances, manufacturers are continually improving the performance, design, and functionality of electrical cooktops and free-standing ranges to meet the evolving needs of consumers and businesses.

Global Electrical Cooktops and Free-standing Ranges Market Outlook:

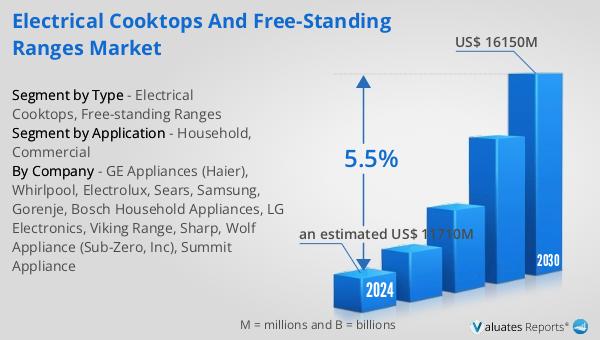

The global Electrical Cooktops and Freestanding Ranges market is anticipated to grow significantly, reaching an estimated value of US$ 16,150 million by 2030, up from US$ 11,710 million in 2024, with a compound annual growth rate (CAGR) of 5.5% between 2024 and 2030. The market is dominated by the top three players, who collectively account for about 55% of the total global market share. Among the different types of products available, freestanding ranges hold the largest segment, making up 81% of the market. This growth is driven by various factors, including technological advancements, increasing consumer demand for energy-efficient and aesthetically pleasing kitchen appliances, and the rising trend of smart homes. Manufacturers are focusing on innovation and design to cater to the evolving preferences of consumers, offering features such as touch controls, precise temperature settings, and enhanced safety mechanisms. The market's expansion is also supported by the growing disposable incomes and urbanization, which are leading to increased spending on home appliances. As the market continues to evolve, it is expected that the demand for electrical cooktops and freestanding ranges will keep rising, driven by both household and commercial needs.

| Report Metric | Details |

| Report Name | Electrical Cooktops and Free-standing Ranges Market |

| Accounted market size in 2024 | an estimated US$ 11710 million |

| Forecasted market size in 2030 | US$ 16150 million |

| CAGR | 5.5% |

| Base Year | 2024 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | GE Appliances (Haier), Whirlpool, Electrolux, Sears, Samsung, Gorenje, Bosch Household Appliances, LG Electronics, Viking Range, Sharp, Wolf Appliance (Sub-Zero, Inc), Summit Appliance |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |