What is Global Drive-by-wire Chassis Market?

The Global Drive-by-wire Chassis Market refers to the advanced automotive technology that replaces traditional mechanical and hydraulic control systems with electronic controls. This market encompasses various systems such as throttle-by-wire, steer-by-wire, brake-by-wire, suspension-by-wire, and shift-by-wire. These systems use electronic signals to control vehicle functions, enhancing precision, reducing weight, and improving fuel efficiency. The drive-by-wire technology is gaining traction due to its potential to enhance vehicle safety, performance, and driver comfort. It also paves the way for the development of autonomous and semi-autonomous vehicles by providing more reliable and responsive control systems. The market is driven by the increasing demand for advanced driver assistance systems (ADAS) and the growing trend towards vehicle electrification. As automotive manufacturers continue to innovate and integrate these technologies into their vehicles, the global drive-by-wire chassis market is expected to witness significant growth in the coming years.

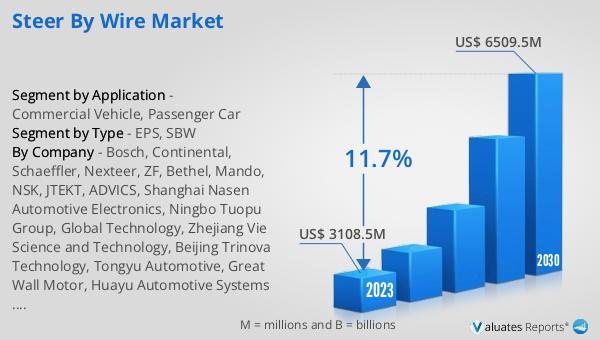

Throttle By Wire, Steer By Wire, Brake By Wire, Suspension By Wire, Shift By Wire in the Global Drive-by-wire Chassis Market:

Throttle-by-wire, steer-by-wire, brake-by-wire, suspension-by-wire, and shift-by-wire are key components of the global drive-by-wire chassis market. Throttle-by-wire replaces the traditional mechanical linkage between the accelerator pedal and the throttle with electronic sensors and actuators. This system improves fuel efficiency and reduces emissions by providing more precise control over the engine's air intake. Steer-by-wire eliminates the mechanical connection between the steering wheel and the wheels, using electronic controls to steer the vehicle. This technology enhances steering precision and allows for more flexible vehicle design, as it removes the need for a steering column. Brake-by-wire replaces the hydraulic brake system with electronic controls, providing faster and more accurate braking response. This system also reduces the weight of the vehicle, contributing to improved fuel efficiency. Suspension-by-wire uses electronic controls to adjust the vehicle's suspension system in real-time, enhancing ride comfort and handling. This technology allows for adaptive suspension systems that can automatically adjust to different driving conditions. Shift-by-wire replaces the mechanical linkage between the gear shifter and the transmission with electronic controls. This system provides smoother and faster gear changes, improving the overall driving experience. Together, these drive-by-wire technologies contribute to the development of more efficient, safer, and more comfortable vehicles. They also play a crucial role in the advancement of autonomous and semi-autonomous driving systems, as they provide the precise and reliable control needed for these technologies to function effectively.

Commercial Vehicle, Passenger Car in the Global Drive-by-wire Chassis Market:

The global drive-by-wire chassis market finds significant usage in both commercial vehicles and passenger cars. In commercial vehicles, drive-by-wire systems enhance operational efficiency and safety. Throttle-by-wire systems in commercial vehicles provide more precise control over engine power, leading to better fuel efficiency and reduced emissions. Steer-by-wire systems improve maneuverability, especially in large trucks and buses, by providing more accurate and responsive steering. Brake-by-wire systems enhance braking performance, reducing stopping distances and improving overall safety. Suspension-by-wire systems in commercial vehicles can adapt to varying load conditions, providing a smoother ride and reducing wear and tear on the vehicle. Shift-by-wire systems enable smoother and faster gear changes, improving the driving experience and reducing driver fatigue. In passenger cars, drive-by-wire systems offer numerous benefits, including enhanced safety, improved fuel efficiency, and a more comfortable driving experience. Throttle-by-wire systems provide more responsive acceleration, while steer-by-wire systems offer more precise and effortless steering. Brake-by-wire systems enhance braking performance, providing faster and more accurate braking response. Suspension-by-wire systems improve ride comfort by automatically adjusting to different driving conditions. Shift-by-wire systems provide smoother and faster gear changes, enhancing the overall driving experience. Additionally, drive-by-wire technologies are essential for the development of advanced driver assistance systems (ADAS) and autonomous driving features in passenger cars. These systems provide the precise and reliable control needed for features such as adaptive cruise control, lane-keeping assist, and automated parking. As a result, the adoption of drive-by-wire technologies in passenger cars is expected to increase significantly in the coming years.

Global Drive-by-wire Chassis Market Outlook:

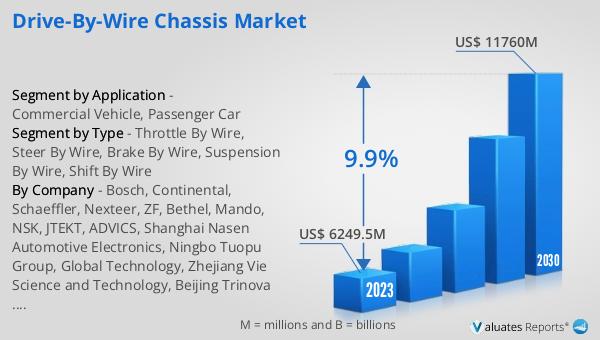

The global drive-by-wire chassis market was valued at approximately $6,249.5 million in 2023 and is projected to reach around $11,760 million by 2030, reflecting a compound annual growth rate (CAGR) of 9.9% during the forecast period from 2024 to 2030. This substantial growth is driven by the increasing demand for advanced automotive technologies that enhance vehicle performance, safety, and fuel efficiency. The adoption of drive-by-wire systems is also fueled by the growing trend towards vehicle electrification and the development of autonomous and semi-autonomous vehicles. As automotive manufacturers continue to innovate and integrate these technologies into their vehicles, the global drive-by-wire chassis market is expected to witness significant growth. The market's expansion is further supported by the rising demand for advanced driver assistance systems (ADAS) and the increasing focus on reducing vehicle weight and emissions. Overall, the global drive-by-wire chassis market is poised for substantial growth in the coming years, driven by technological advancements and the evolving needs of the automotive industry.

| Report Metric | Details |

| Report Name | Drive-by-wire Chassis Market |

| Accounted market size in 2023 | US$ 6249.5 million |

| Forecasted market size in 2030 | US$ 11760 million |

| CAGR | 9.9% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Bosch, Continental, Schaeffler, Nexteer, ZF, Bethel, Mando, NSK, JTEKT, ADVICS, Shanghai Nasen Automotive Electronics, Ningbo Tuopu Group, Global Technology, Zhejiang Vie Science and Technology, Beijing Trinova Technology, Tongyu Automotive, Great Wall Motor, Huayu Automotive Systems Company |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |