What is Global Vehicle Diagnostic Oscilloscopes Market?

The Global Vehicle Diagnostic Oscilloscopes Market is a specialized segment within the automotive industry that focuses on the use of oscilloscopes for diagnosing and troubleshooting vehicle systems. Oscilloscopes are electronic test instruments that graphically display varying signal voltages, making them essential for identifying issues in a vehicle's electrical and electronic systems. These devices are crucial for modern vehicles, which are increasingly reliant on complex electronic systems for everything from engine management to infotainment. The market encompasses a range of products designed to meet the needs of different types of vehicles, including passenger cars and commercial vehicles. The growing complexity of automotive electronics, coupled with the increasing demand for advanced diagnostic tools, is driving the expansion of this market. As vehicles become more sophisticated, the need for precise and reliable diagnostic equipment like oscilloscopes becomes ever more critical.

Bandwidth Below 500MHz, Bandwidth 500MHz-2GHz, Bandwidth Above 2GHz in the Global Vehicle Diagnostic Oscilloscopes Market:

In the Global Vehicle Diagnostic Oscilloscopes Market, bandwidth is a key specification that determines the range of frequencies an oscilloscope can accurately measure. Bandwidth Below 500MHz is typically sufficient for most basic diagnostic tasks in automotive applications. These oscilloscopes are often used for general-purpose diagnostics, such as checking the integrity of signals in engine control units (ECUs), sensors, and other electronic components. They are cost-effective and provide adequate performance for routine maintenance and troubleshooting. Bandwidth 500MHz-2GHz oscilloscopes offer a higher range of frequency measurement, making them suitable for more advanced diagnostic tasks. These devices are often used in scenarios where higher precision is required, such as in the development and testing of advanced driver-assistance systems (ADAS) and other high-speed automotive networks. They provide a more detailed view of signal behavior, which is essential for identifying subtle issues that could affect vehicle performance. Bandwidth Above 2GHz oscilloscopes represent the high end of the market and are used for the most demanding diagnostic applications. These devices are capable of capturing extremely high-frequency signals, making them ideal for cutting-edge automotive technologies like autonomous driving systems and high-speed communication networks. They offer unparalleled accuracy and resolution, allowing engineers to diagnose and resolve the most complex issues in modern vehicles. The choice of bandwidth depends on the specific diagnostic needs and the complexity of the vehicle's electronic systems. As automotive technology continues to evolve, the demand for higher bandwidth oscilloscopes is expected to grow, driven by the need for more precise and comprehensive diagnostic capabilities.

Passenger Cars, Commercial Vehicles in the Global Vehicle Diagnostic Oscilloscopes Market:

The usage of Global Vehicle Diagnostic Oscilloscopes Market in passenger cars and commercial vehicles varies based on the specific requirements and complexities of these vehicle types. In passenger cars, oscilloscopes are primarily used for diagnosing issues related to the vehicle's electronic control units (ECUs), sensors, and communication networks. These vehicles often feature a wide range of electronic systems, including engine management, transmission control, infotainment, and advanced driver-assistance systems (ADAS). Oscilloscopes help technicians identify and resolve issues in these systems, ensuring optimal performance and safety. For example, they can be used to diagnose problems with fuel injection systems, ignition timing, and sensor signals, providing a detailed view of the electrical activity within the vehicle. In commercial vehicles, the usage of oscilloscopes extends to more robust and heavy-duty applications. These vehicles, which include trucks, buses, and other large transport vehicles, often have more complex and demanding electronic systems. Oscilloscopes are used to diagnose issues in systems such as engine control, braking, and transmission, as well as in specialized equipment like refrigeration units and hydraulic systems. The ability to accurately measure and analyze high-frequency signals is crucial for maintaining the reliability and efficiency of these vehicles, which are often subjected to harsh operating conditions. Additionally, commercial vehicles may require more frequent and detailed diagnostics due to their higher usage rates and the critical nature of their operations. Overall, the use of oscilloscopes in both passenger cars and commercial vehicles is essential for ensuring the proper functioning of modern automotive electronics. These devices provide the precision and accuracy needed to diagnose and resolve a wide range of issues, contributing to improved vehicle performance, safety, and reliability.

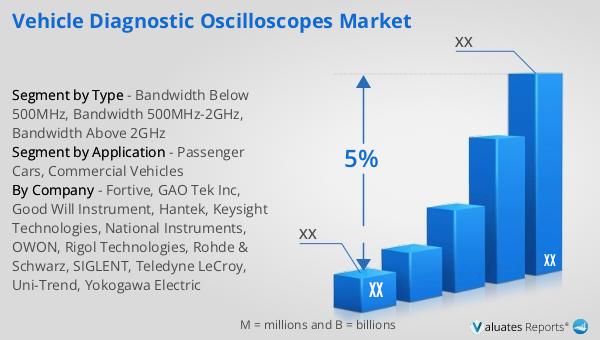

Global Vehicle Diagnostic Oscilloscopes Market Outlook:

The global pharmaceutical market was valued at 1,475 billion USD in 2022, experiencing a compound annual growth rate (CAGR) of 5% over the next six years. In comparison, the chemical drug market saw an increase from 1,005 billion USD in 2018 to 1,094 billion USD in 2022. This growth highlights the expanding demand for pharmaceutical products and the significant role that chemical drugs continue to play within the broader market. The pharmaceutical industry encompasses a wide range of products, including prescription medications, over-the-counter drugs, and biologics, all of which contribute to the overall market value. The steady growth rate indicates a robust and resilient market, driven by factors such as an aging population, increasing prevalence of chronic diseases, and ongoing advancements in medical research and technology. As the market continues to evolve, the demand for innovative and effective pharmaceutical products is expected to remain strong, further fueling growth and development within the industry.

| Report Metric | Details |

| Report Name | Vehicle Diagnostic Oscilloscopes Market |

| CAGR | 5% |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Fortive, GAO Tek Inc, Good Will Instrument, Hantek, Keysight Technologies, National Instruments, OWON, Rigol Technologies, Rohde & Schwarz, SIGLENT, Teledyne LeCroy, Uni-Trend, Yokogawa Electric |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |