What is Global Chemotherapy-Induced Oral Mucositis Market?

The Global Chemotherapy-Induced Oral Mucositis Market refers to the market dedicated to the treatment and management of oral mucositis, a common and often debilitating side effect of chemotherapy. Oral mucositis involves the inflammation and ulceration of the mucous membranes lining the mouth, leading to severe pain, difficulty in eating and swallowing, and an increased risk of infection. This condition significantly impacts the quality of life of cancer patients and can also lead to interruptions in cancer treatment, thereby affecting overall treatment outcomes. The market encompasses a range of products and therapies designed to prevent, manage, and treat oral mucositis, including medications, mouthwashes, gels, and other supportive care products. The growing prevalence of cancer and the increasing use of chemotherapy as a treatment modality are key factors driving the demand for effective oral mucositis management solutions. Additionally, advancements in medical research and technology are leading to the development of more effective and targeted therapies, further expanding the market.

Ice Chips(Cryotherapy), Preventive And Supportive Dental Care, Strong Oral Cleaning Procedures, Gels/Rinses in the Global Chemotherapy-Induced Oral Mucositis Market:

Ice chips, also known as cryotherapy, are a simple yet effective method used in the management of chemotherapy-induced oral mucositis. The principle behind cryotherapy is to reduce blood flow to the oral mucosa by cooling the tissues, thereby minimizing the exposure of the mucous membranes to the harmful effects of chemotherapy drugs. Patients are often advised to suck on ice chips before, during, and after chemotherapy sessions to help prevent the onset of mucositis. This method is particularly beneficial because it is non-invasive, cost-effective, and easy to administer. Preventive and supportive dental care is another crucial aspect of managing oral mucositis. Regular dental check-ups and cleanings can help identify and address any pre-existing oral health issues that may exacerbate mucositis. Dentists may also provide patients with customized oral care plans, including the use of fluoride treatments, antimicrobial mouthwashes, and other preventive measures to maintain oral hygiene and reduce the risk of infection. Strong oral cleaning procedures are essential for patients undergoing chemotherapy to minimize the risk of mucositis. This includes brushing teeth with a soft-bristled toothbrush, using non-alcoholic mouthwashes, and avoiding irritants such as spicy or acidic foods. Patients are also advised to maintain good hydration and use saliva substitutes if they experience dry mouth. Gels and rinses specifically formulated for oral mucositis can provide significant relief from pain and discomfort. These products often contain ingredients such as lidocaine, which acts as a local anesthetic, or benzydamine, which has anti-inflammatory properties. Some gels and rinses also include protective coatings that form a barrier over the mucous membranes, shielding them from further irritation and promoting healing. The availability of these various treatment options allows healthcare providers to tailor their approach to each patient's specific needs, improving overall outcomes and quality of life.

Hospitals, Oncology Centres, Research Institutes, Dental Clinics, Others in the Global Chemotherapy-Induced Oral Mucositis Market:

The usage of products and therapies from the Global Chemotherapy-Induced Oral Mucositis Market spans across various healthcare settings, including hospitals, oncology centers, research institutes, dental clinics, and other specialized care facilities. In hospitals, the management of oral mucositis is an integral part of the overall care plan for cancer patients undergoing chemotherapy. Hospital-based healthcare providers, including oncologists, nurses, and dental specialists, work collaboratively to implement preventive measures and provide timely interventions to manage mucositis symptoms. This multidisciplinary approach ensures that patients receive comprehensive care, addressing both the physical and emotional aspects of their condition. Oncology centers, which specialize in cancer treatment, are at the forefront of implementing advanced therapies and protocols for managing chemotherapy-induced oral mucositis. These centers often have access to the latest research and clinical trials, allowing them to offer cutting-edge treatments and personalized care plans. Oncology centers also play a crucial role in educating patients about the importance of oral care during chemotherapy and providing them with the necessary resources and support. Research institutes contribute significantly to the advancement of knowledge and development of new therapies for oral mucositis. Scientists and researchers at these institutions conduct studies to understand the underlying mechanisms of mucositis, identify potential therapeutic targets, and evaluate the efficacy of new treatments. Their findings help shape clinical guidelines and inform best practices for managing the condition. Dental clinics are essential in providing preventive and supportive dental care to patients at risk of or suffering from oral mucositis. Dentists and dental hygienists work closely with oncology teams to ensure that patients maintain optimal oral health throughout their cancer treatment. They offer services such as dental cleanings, fluoride treatments, and the management of oral infections, all of which are crucial in preventing and mitigating the effects of mucositis. Other specialized care facilities, including palliative care centers and home healthcare services, also play a role in managing oral mucositis. These facilities provide ongoing support to patients, helping them manage symptoms and maintain their quality of life during and after chemotherapy.

Global Chemotherapy-Induced Oral Mucositis Market Outlook:

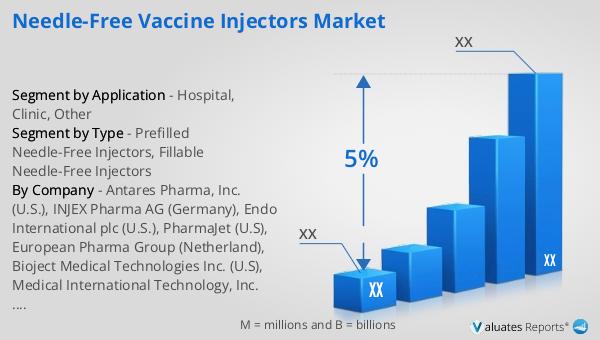

According to our research, the global market for medical devices is projected to reach approximately $603 billion by the year 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including advancements in medical technology, an aging global population, and an increasing prevalence of chronic diseases. The demand for innovative medical devices that can improve patient outcomes and enhance the efficiency of healthcare delivery is on the rise. Additionally, the expansion of healthcare infrastructure in emerging markets and the growing adoption of digital health solutions are contributing to the market's growth. Companies operating in the medical device sector are continuously investing in research and development to bring new and improved products to market. This includes the development of minimally invasive surgical devices, advanced diagnostic tools, and wearable health monitors. The regulatory environment for medical devices is also evolving, with a focus on ensuring the safety and efficacy of new products. As a result, manufacturers are required to adhere to stringent quality standards and undergo rigorous testing and approval processes. Overall, the global medical device market is poised for significant growth, driven by technological innovation and increasing healthcare needs.

| Report Metric | Details |

| Report Name | Chemotherapy-Induced Oral Mucositis Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Izun Pharmaceuticals, Soleva Pharma, Aurora Bioscience, INNOVATION Pharma, Camurus AB, Monopar Therapeutics, Prothex Inc., Access Pharmaceutical Inc., Swedish Orphan Biovitrum AB, NeoMedLight |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |