What is Global Food Grade Propylene Glycol Market?

The Global Food Grade Propylene Glycol Market is an intriguing sector that focuses on the production and distribution of propylene glycol that is safe for use in food and beverage products. This particular type of propylene glycol is meticulously manufactured to meet stringent quality standards, ensuring it is suitable for consumption or use in food-related applications. The market caters to a wide array of industries, including food and beverage manufacturing, pharmaceuticals, and cosmetics, among others. The demand for food-grade propylene glycol is driven by its versatility and essential role in various products, such as acting as a solvent for food colors and flavors, serving as a humectant to maintain moisture in certain foods, or even being used as a carrier in fragrance oils. The significance of this market lies in its contribution to the safety and quality of food products, making it a critical component of the global food supply chain. Its role in ensuring the integrity and safety of consumable goods highlights its importance in the global market.

Mono Propylene Glycol, Dipropylene Glycol, Tripropylene Glycol in the Global Food Grade Propylene Glycol Market:

Diving into the Global Food Grade Propylene Glycol Market, we find it segmented into three primary types: Mono Propylene Glycol (MPG), Dipropylene Glycol (DPG), and Tripropylene Glycol (TPG). Each type serves distinct purposes and applications, making them vital in various industries. Mono Propylene Glycol, the most widely used form, is renowned for its versatility and safety, making it a preferred ingredient in food, pharmaceutical, and cosmetic products. Its properties as a solvent and humectant make it invaluable in the production of food flavors, pharmaceuticals, and skincare items. Dipropylene Glycol, on the other hand, is often used in higher-end food and fragrance applications due to its lower toxicity and better solvency properties. It's particularly favored in the creation of fragrances and cosmetics, where its ability to carry scents and stabilize volatile compounds is highly prized. Lastly, Tripropylene Glycol, though less common, finds its niche in specialized applications where its unique properties are required. It's used in certain food processing applications and in the production of some pharmaceuticals, where its performance characteristics are specifically needed. The Global Food Grade Propylene Glycol Market's reliance on these three types underscores the diversity and complexity of modern food and beverage, pharmaceutical, and cosmetic manufacturing, highlighting the critical role these substances play in the quality and safety of consumer products.

Flavors and Fragrances, Humectant and Stabilizer, Other in the Global Food Grade Propylene Glycol Market:

In the realm of the Global Food Grade Propylene Glycol Market, its applications are vast and varied, particularly notable in the areas of flavors and fragrances, humectants and stabilizers, among others. In the world of flavors and fragrances, food-grade propylene glycol stands out as a crucial ingredient. It acts as a solvent, helping to dissolve food colors and flavors, thereby ensuring they are evenly distributed throughout the product. This property is especially important in the production of processed foods and beverages, where consistency and quality are paramount. Furthermore, its use in fragrances as a carrier helps in stabilizing volatile compounds, making it indispensable in the cosmetics industry. As a humectant and stabilizer, propylene glycol's ability to retain moisture is highly valued. This characteristic is crucial in food products, where it helps maintain freshness and prevents the food from drying out. Additionally, in pharmaceuticals, it ensures that medicines retain their efficacy over time by stabilizing their moisture content. Beyond these applications, food-grade propylene glycol finds use in various other sectors, showcasing its versatility and importance in ensuring the quality and safety of a wide range of consumer products. Its multifaceted applications underscore its vital role in the global market, making it an essential component in the production of numerous goods.

Global Food Grade Propylene Glycol Market Outlook:

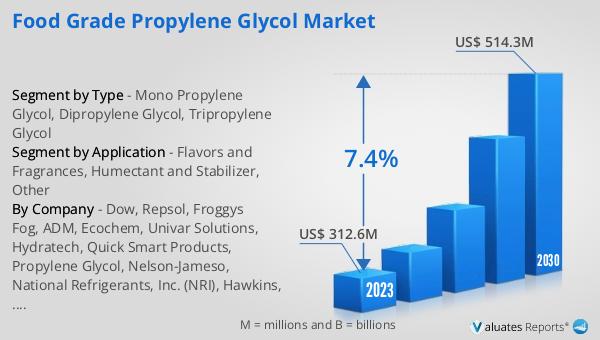

The market outlook for the Global Food Grade Propylene Glycol Market presents a promising future. As of 2023, the market's value stood at approximately 312.6 million USD. Looking ahead, projections suggest a significant growth trajectory, with expectations to reach around 514.3 million USD by the year 2030. This anticipated growth, marked by a compound annual growth rate (CAGR) of 7.4% during the forecast period from 2024 to 2030, underscores the increasing demand and expanding applications of food-grade propylene glycol across various industries. Such growth is indicative of the market's robustness and its critical role in supporting the food, pharmaceutical, and cosmetic sectors, among others. The upward trend reflects the growing recognition of the importance of high-quality, safe ingredients in consumer products, driving the demand for food-grade propylene glycol. This optimistic outlook highlights the market's potential for continued expansion and its importance in meeting the evolving needs of global consumers.

| Report Metric | Details |

| Report Name | Food Grade Propylene Glycol Market |

| Accounted market size in 2023 | US$ 312.6 million |

| Forecasted market size in 2030 | US$ 514.3 million |

| CAGR | 7.4% |

| Base Year | 2023 |

| Forecasted years | 2024 - 2030 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Dow, Repsol, Froggys Fog, ADM, Ecochem, Univar Solutions, Hydratech, Quick Smart Products, Propylene Glycol, Nelson-Jameso, National Refrigerants, Inc. (NRI), Hawkins, Finar |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |