What is Aluminum Nitride Ceramic Package - Global Market?

Aluminum Nitride Ceramic Package is a specialized component used in various high-tech applications due to its excellent thermal conductivity and electrical insulation properties. This material is particularly valued in industries where heat dissipation is crucial, such as electronics and semiconductors. The global market for Aluminum Nitride Ceramic Packages is driven by the increasing demand for efficient thermal management solutions in electronic devices. As technology advances, the need for materials that can handle higher power densities without compromising performance becomes more critical. Aluminum Nitride Ceramic Packages offer a solution by providing a robust platform that can withstand high temperatures while maintaining electrical insulation. This makes them ideal for use in high-frequency and high-power applications. The market is also influenced by the growing trend towards miniaturization in electronics, which requires materials that can efficiently manage heat in smaller spaces. As a result, the demand for Aluminum Nitride Ceramic Packages is expected to grow as industries continue to seek out materials that can meet these challenging requirements.

Substrate Thickness ≤0.5mm, Substrate Thickness >0.5mm in the Aluminum Nitride Ceramic Package - Global Market:

In the context of Aluminum Nitride Ceramic Packages, substrate thickness plays a crucial role in determining the performance and application suitability of the material. Substrate thickness can be broadly categorized into two segments: those with a thickness of ≤0.5mm and those with a thickness of >0.5mm. Substrates with a thickness of ≤0.5mm are typically used in applications where space is at a premium, and weight reduction is a priority. These thin substrates are ideal for use in compact electronic devices where efficient heat dissipation is required without adding significant bulk. They are often used in portable electronics, where the balance between performance and size is critical. On the other hand, substrates with a thickness of >0.5mm are used in applications where durability and robustness are more important than size constraints. These thicker substrates can handle higher power loads and are often used in industrial applications where reliability and longevity are paramount. The choice between these two substrate thicknesses depends largely on the specific requirements of the application, including factors such as thermal management needs, space constraints, and power handling capabilities. As the demand for more efficient and compact electronic devices continues to grow, the market for Aluminum Nitride Ceramic Packages with varying substrate thicknesses is expected to expand, offering solutions tailored to a wide range of applications.

Automotive Electronics, Communication Devices, Aeronautics and Astronautics, High Power LED, Consumer Electronics, Others in the Aluminum Nitride Ceramic Package - Global Market:

Aluminum Nitride Ceramic Packages are utilized in a variety of industries due to their unique properties, including high thermal conductivity and electrical insulation. In the automotive electronics sector, these packages are used to manage heat in components such as power modules and sensors, which are critical for the performance and reliability of modern vehicles. As vehicles become more technologically advanced, the demand for efficient thermal management solutions continues to grow. In communication devices, Aluminum Nitride Ceramic Packages are used to enhance the performance of high-frequency components, ensuring reliable signal transmission and reception. The aeronautics and astronautics industries also benefit from these packages, as they provide the necessary thermal management for high-performance electronic systems used in aircraft and spacecraft. High power LEDs, which are used in a variety of lighting applications, rely on Aluminum Nitride Ceramic Packages to dissipate heat effectively, ensuring long-lasting performance and reliability. In consumer electronics, these packages are used in devices such as smartphones and laptops, where efficient heat management is crucial for maintaining performance and preventing overheating. Other industries, including industrial and medical, also utilize Aluminum Nitride Ceramic Packages for their thermal management needs, highlighting the versatility and importance of this material in a wide range of applications.

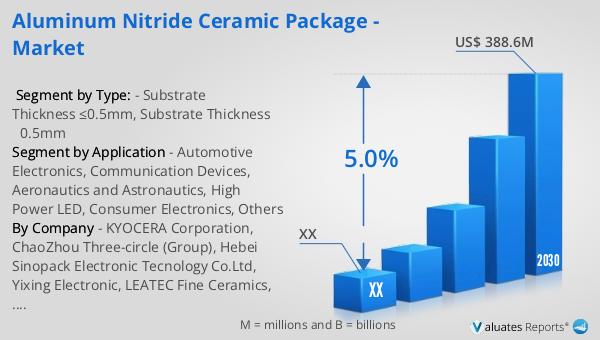

Aluminum Nitride Ceramic Package - Global Market Outlook:

The global market for Aluminum Nitride Ceramic Packages was valued at approximately $275.8 million in 2023. It is projected to grow to a revised size of $388.6 million by 2030, reflecting a compound annual growth rate (CAGR) of 5.0% during the forecast period from 2024 to 2030. This growth is indicative of the increasing demand for advanced thermal management solutions across various industries. In comparison, the global semiconductor market was estimated at $579 billion in 2022 and is expected to reach $790 billion by 2029, growing at a CAGR of 6% during the forecast period. The growth in the semiconductor market underscores the broader trend towards increased technological integration and the need for materials that can support high-performance applications. As industries continue to evolve and demand more efficient and reliable electronic components, the market for Aluminum Nitride Ceramic Packages is poised to expand, offering solutions that meet the stringent requirements of modern technology.

| Report Metric | Details |

| Report Name | Aluminum Nitride Ceramic Package - Market |

| Forecasted market size in 2030 | US$ 388.6 million |

| CAGR | 5.0% |

| Forecasted years | 2024 - 2030 |

| Segment by Type: |

|

| Segment by Application |

|

| By Region |

|

| By Company | KYOCERA Corporation, ChaoZhou Three-circle (Group), Hebei Sinopack Electronic Tecnology Co.Ltd, Yixing Electronic, LEATEC Fine Ceramics, Shengda Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |