What is Global Industrial Power Transmission Belts Market?

The Global Industrial Power Transmission Belts Market is a crucial segment within the broader industrial machinery and components sector. These belts are essential components used to transfer power between different parts of machinery, ensuring efficient operation and productivity. They are widely used across various industries, including manufacturing, agriculture, construction, and more, due to their ability to handle high loads and operate under diverse conditions. The market for these belts is driven by the need for efficient power transmission solutions that can enhance the performance and longevity of machinery. As industries continue to evolve and demand more efficient and reliable machinery, the need for high-quality power transmission belts is expected to grow. These belts come in various types, including V-belts, timing belts, and others, each designed to meet specific operational requirements. The market is characterized by technological advancements, with manufacturers focusing on developing belts that offer improved durability, efficiency, and resistance to wear and tear. Additionally, the market is influenced by factors such as industrial automation, the rise of smart manufacturing, and the increasing emphasis on energy efficiency. As a result, the Global Industrial Power Transmission Belts Market is poised for significant growth in the coming years, driven by innovation and the expanding needs of various industries.

V-belts, Timing Belts, Other in the Global Industrial Power Transmission Belts Market:

V-belts are one of the most commonly used types of power transmission belts in the Global Industrial Power Transmission Belts Market. They are named for their V-shaped cross-section, which allows them to fit snugly into the grooves of pulleys, providing excellent grip and reducing slippage. This design makes V-belts highly efficient for transmitting power in various industrial applications. They are particularly favored for their simplicity, ease of installation, and ability to handle high-speed operations. V-belts are used in a wide range of machinery, from small appliances to large industrial equipment, due to their versatility and reliability. They are available in different sizes and materials, allowing them to be tailored to specific applications and operating conditions. Timing belts, on the other hand, are designed for applications where precise timing and synchronization are critical. They have teeth on the inner surface that mesh with corresponding grooves on the pulleys, ensuring accurate and consistent power transmission. This makes them ideal for applications such as automotive engines, where precise timing is essential for optimal performance. Timing belts are also used in various industrial machinery, including conveyor systems and robotics, where precision and reliability are paramount. They are known for their durability and ability to operate quietly, making them a preferred choice in noise-sensitive environments. Other types of power transmission belts in the market include flat belts, ribbed belts, and specialty belts designed for specific applications. Flat belts are used in applications where high-speed operation and smooth power transmission are required. They are often used in conveyor systems and other machinery where large amounts of power need to be transmitted over long distances. Ribbed belts, also known as multi-rib belts, combine the advantages of flat belts and V-belts, offering high power transmission capacity and flexibility. They are used in applications where compact design and high efficiency are required. Specialty belts are designed for specific applications, such as high-temperature environments or applications requiring chemical resistance. These belts are made from specialized materials and are engineered to meet the unique demands of their respective applications. Overall, the Global Industrial Power Transmission Belts Market offers a wide range of belt types, each designed to meet the specific needs of different industries and applications. As technology continues to advance, manufacturers are focusing on developing belts that offer improved performance, efficiency, and durability, ensuring that they can meet the evolving demands of the market.

General Industry, Agricultural Machinery, Construction Machinery, Others in the Global Industrial Power Transmission Belts Market:

The usage of Global Industrial Power Transmission Belts Market extends across various sectors, each with its unique requirements and challenges. In the general industry, these belts are used in a wide range of machinery and equipment, from conveyor systems to pumps and compressors. They play a crucial role in ensuring the smooth and efficient operation of industrial processes, helping to reduce downtime and maintenance costs. The versatility and reliability of power transmission belts make them an essential component in the general industry, where they are used to transmit power in various applications, from manufacturing to material handling. In agricultural machinery, power transmission belts are used in equipment such as tractors, combine harvesters, and balers. These belts are designed to withstand the harsh conditions of agricultural environments, including exposure to dust, dirt, and moisture. They are essential for ensuring the efficient operation of agricultural machinery, helping to improve productivity and reduce operational costs. The durability and reliability of power transmission belts make them a preferred choice in the agricultural sector, where they are used to transmit power in various applications, from plowing to harvesting. In construction machinery, power transmission belts are used in equipment such as excavators, bulldozers, and cranes. These belts are designed to handle the high loads and demanding conditions of construction environments, ensuring the efficient operation of machinery and equipment. They are essential for ensuring the smooth and efficient operation of construction processes, helping to reduce downtime and maintenance costs. The durability and reliability of power transmission belts make them a preferred choice in the construction sector, where they are used to transmit power in various applications, from earthmoving to material handling. In other sectors, power transmission belts are used in a wide range of applications, from automotive to aerospace. They are essential for ensuring the efficient operation of machinery and equipment, helping to improve productivity and reduce operational costs. The versatility and reliability of power transmission belts make them an essential component in various industries, where they are used to transmit power in various applications, from manufacturing to material handling. Overall, the Global Industrial Power Transmission Belts Market plays a crucial role in ensuring the efficient operation of machinery and equipment across various sectors, helping to improve productivity and reduce operational costs.

Global Industrial Power Transmission Belts Market Outlook:

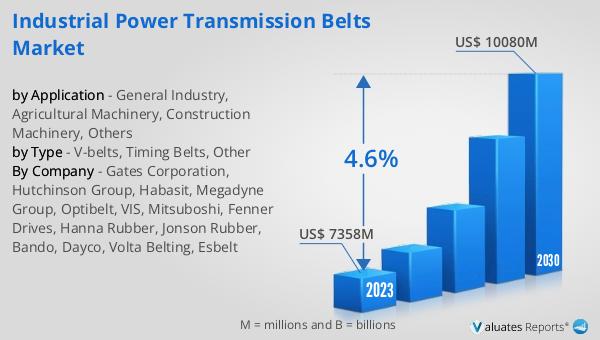

The outlook for the Global Industrial Power Transmission Belts Market indicates a promising growth trajectory. The market is anticipated to expand from $7,697 million in 2024 to $10,500 million by 2031, reflecting a compound annual growth rate (CAGR) of 4.6% from 2025 to 2031. This growth is primarily driven by the increasing demand for critical product segments and the diverse applications of these belts across various industries. As industries continue to evolve, the need for efficient and reliable power transmission solutions becomes more pronounced, fueling the demand for high-quality belts. However, the market is not without its challenges. Evolving U.S. tariff policies introduce a level of trade-cost volatility and supply chain uncertainty, which could impact the market dynamics. These policies may lead to fluctuations in raw material prices and affect the overall cost structure of manufacturing power transmission belts. Despite these challenges, the market is expected to continue its growth trajectory, driven by innovation and the expanding needs of various industries. Manufacturers are focusing on developing belts that offer improved performance, efficiency, and durability, ensuring that they can meet the evolving demands of the market. As a result, the Global Industrial Power Transmission Belts Market is poised for significant growth in the coming years, driven by innovation and the expanding needs of various industries.

| Report Metric |

Details |

| Report Name |

Industrial Power Transmission Belts Market |

| Accounted market size in 2024 |

US$ 7697 in million |

| Forecasted market size in 2031 |

US$ 10500 million |

| CAGR |

4.6% |

| Base Year |

2024 |

| Forecasted years |

2025 - 2031 |

| Segment by Type |

- V-belts

- Timing Belts

- Other

|

| Segment by Application |

- General Industry

- Agricultural Machinery

- Construction Machinery

- Others

|

| Production by Region |

- North America

- Europe

- China

- Japan

|

| Sales by Region |

- North America (United States, Canada)

- Europe (Germany, France, UK, Italy, Russia) Rest of Europe

- Nordic Countries

- Asia-Pacific (China, Japan, South Korea)

- Southeast Asia (India, Australia)

- Rest of Asia

- Latin America (Mexico, Brazil)

- Rest of Latin America

- Middle East & Africa (Turkey, Saudi Arabia, UAE, Rest of MEA)

|

| By Company |

Gates Corporation, Hutchinson Group, Habasit, Megadyne Group, Optibelt, VIS, Mitsuboshi, Fenner Drives, Hanna Rubber, Jonson Rubber, Bando, Dayco, Volta Belting, Esbelt |

| Forecast units |

USD million in value |

| Report coverage |

Revenue and volume forecast, company share, competitive landscape, growth factors and trends |