What is Global Commercial Vehicle Low Voltage Power Distribution Modules Market?

The Global Commercial Vehicle Low Voltage Power Distribution Modules Market refers to the industry focused on the development, production, and distribution of power distribution modules specifically designed for commercial vehicles. These modules are essential components that manage and distribute electrical power within vehicles, ensuring that various systems and components receive the necessary voltage to function effectively. As commercial vehicles, such as trucks and buses, become increasingly sophisticated with advanced electronics and systems, the demand for efficient and reliable power distribution solutions has grown. These modules are crucial for maintaining the performance and safety of vehicles by preventing electrical overloads and ensuring that power is distributed evenly across all systems. The market is driven by the need for enhanced vehicle performance, increased safety standards, and the growing adoption of electric and hybrid vehicles, which require more complex electrical systems. As a result, manufacturers are focusing on developing innovative solutions that cater to the evolving needs of the commercial vehicle industry, making this market a vital component of the automotive sector.

Relay Type, Solid-State Type in the Global Commercial Vehicle Low Voltage Power Distribution Modules Market:

In the realm of Global Commercial Vehicle Low Voltage Power Distribution Modules, two primary types of technologies are prevalent: Relay Type and Solid-State Type. Relay Type modules are traditional systems that use electromechanical relays to control the distribution of electrical power within a vehicle. These relays act as switches that open or close circuits, allowing or interrupting the flow of electricity to various components. Relay Type modules are known for their reliability and cost-effectiveness, making them a popular choice for many commercial vehicle manufacturers. However, they have limitations in terms of speed and durability, as the mechanical components can wear out over time, leading to potential failures. On the other hand, Solid-State Type modules represent a more modern approach to power distribution. These modules utilize semiconductor devices, such as transistors and diodes, to control the flow of electricity. Unlike Relay Type modules, Solid-State modules have no moving parts, which enhances their durability and reduces the risk of mechanical failure. They offer faster response times and greater precision in controlling electrical power, making them ideal for applications that require high levels of accuracy and reliability. Additionally, Solid-State modules are more compact and lightweight, which is advantageous for vehicle manufacturers looking to reduce weight and improve fuel efficiency. The adoption of Solid-State Type modules is driven by the increasing complexity of vehicle electrical systems and the demand for more efficient and reliable power distribution solutions. As commercial vehicles continue to evolve with advanced technologies and systems, the need for robust and efficient power distribution modules becomes more critical. Manufacturers are investing in research and development to enhance the capabilities of both Relay Type and Solid-State Type modules, ensuring they meet the growing demands of the industry. The choice between these two types of modules often depends on the specific requirements of the vehicle and the preferences of the manufacturer. While Relay Type modules remain a cost-effective solution for many applications, Solid-State modules are gaining traction due to their superior performance and reliability. As the market continues to grow, it is expected that both types of modules will coexist, each serving different segments of the commercial vehicle industry based on their unique advantages.

Internal Combustion Engine, Electric Vehicle in the Global Commercial Vehicle Low Voltage Power Distribution Modules Market:

The Global Commercial Vehicle Low Voltage Power Distribution Modules Market plays a crucial role in the operation of both Internal Combustion Engine (ICE) vehicles and Electric Vehicles (EVs). In ICE vehicles, these modules are responsible for managing the distribution of electrical power generated by the engine's alternator. They ensure that all electrical systems, such as lighting, infotainment, and safety features, receive the appropriate voltage to function effectively. As ICE vehicles become more advanced with the integration of electronic control units and other sophisticated systems, the demand for efficient power distribution modules has increased. These modules help maintain the performance and reliability of ICE vehicles by preventing electrical overloads and ensuring that power is distributed evenly across all systems. In Electric Vehicles, the role of power distribution modules becomes even more critical. EVs rely entirely on electrical power stored in batteries to operate, making efficient power distribution essential for optimal performance. Low voltage power distribution modules in EVs manage the flow of electricity from the battery to various components, such as the electric motor, climate control system, and onboard electronics. They ensure that each component receives the necessary power to function efficiently, contributing to the overall performance and range of the vehicle. As the adoption of EVs continues to grow, the demand for advanced power distribution modules is expected to increase. Manufacturers are focusing on developing innovative solutions that cater to the unique requirements of EVs, such as higher efficiency, compact size, and lightweight design. These modules are designed to handle the increased electrical loads associated with EVs while ensuring safety and reliability. The growing trend towards electrification in the automotive industry is driving the development of new technologies and solutions in the power distribution modules market. As both ICE vehicles and EVs continue to evolve with advanced technologies and systems, the need for robust and efficient power distribution modules becomes more critical. Manufacturers are investing in research and development to enhance the capabilities of these modules, ensuring they meet the growing demands of the industry. The Global Commercial Vehicle Low Voltage Power Distribution Modules Market is poised to play a significant role in the future of the automotive industry, supporting the transition towards more sustainable and efficient transportation solutions.

Global Commercial Vehicle Low Voltage Power Distribution Modules Market Outlook:

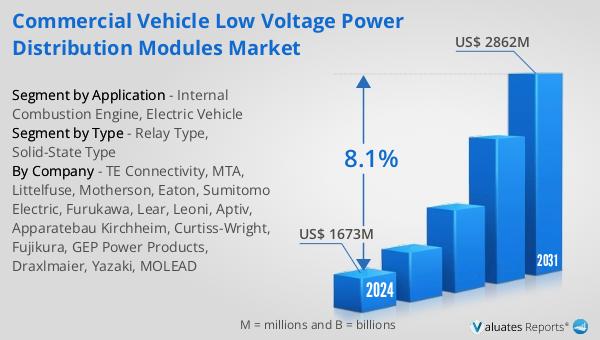

The outlook for the Global Commercial Vehicle Low Voltage Power Distribution Modules Market indicates a significant growth trajectory, with projections showing an increase from $1,673 million in 2024 to $2,862 million by 2031, reflecting a compound annual growth rate (CAGR) of 8.1% from 2025 to 2031. This growth is driven by key product segments and a wide range of end-use applications. However, evolving U.S. tariff policies are introducing volatility in trade costs and creating uncertainty in supply chains. Despite these challenges, the market for low voltage power distribution units (LV PDUs) is expected to expand at a CAGR of 10-15%, with trends such as smartization and solid-state solutions gaining prominence. These trends are particularly evident in China's burgeoning new energy vehicle (NEV) market and Europe's smart vehicle applications. As the industry adapts to these changes, manufacturers are focusing on developing innovative solutions that cater to the evolving needs of the commercial vehicle sector. The market's growth is supported by the increasing complexity of vehicle electrical systems and the demand for more efficient and reliable power distribution solutions. As a result, the Global Commercial Vehicle Low Voltage Power Distribution Modules Market is poised to play a crucial role in the future of the automotive industry, supporting the transition towards more sustainable and efficient transportation solutions.

| Report Metric | Details |

| Report Name | Commercial Vehicle Low Voltage Power Distribution Modules Market |

| Accounted market size in 2024 | US$ 1673 in million |

| Forecasted market size in 2031 | US$ 2862 million |

| CAGR | 8.1% |

| Base Year | 2024 |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Production by Region |

|

| Sales by Region |

|

| By Company | TE Connectivity, MTA, Littelfuse, Motherson, Eaton, Sumitomo Electric, Furukawa, Lear, Leoni, Aptiv, Apparatebau Kirchheim, Curtiss-Wright, Fujikura, GEP Power Products, Draxlmaier, Yazaki, MOLEAD |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |