What is Global Hi-Fi Standmount Speakers Market?

The Global Hi-Fi Standmount Speakers Market refers to the worldwide industry focused on the production, distribution, and sale of high-fidelity standmount speakers. These speakers are designed to deliver superior sound quality, making them a popular choice among audiophiles and music enthusiasts. Standmount speakers, also known as bookshelf speakers, are typically smaller than floor-standing speakers but are engineered to provide a rich and immersive audio experience. They are often used in home audio systems, recording studios, and other settings where high-quality sound reproduction is essential. The market encompasses a wide range of products from various manufacturers, each offering different features, designs, and price points to cater to diverse consumer preferences. Factors such as technological advancements, increasing consumer demand for high-quality audio equipment, and the growing popularity of home entertainment systems are driving the growth of this market. Additionally, the rise of e-commerce platforms has made it easier for consumers to access a wide variety of Hi-Fi standmount speakers, further contributing to market expansion. As a result, the Global Hi-Fi Standmount Speakers Market is expected to continue its growth trajectory, offering numerous opportunities for manufacturers and retailers alike.

Active Speakers, Passive Speakers in the Global Hi-Fi Standmount Speakers Market:

Active speakers and passive speakers are two primary categories within the Global Hi-Fi Standmount Speakers Market, each with distinct characteristics and applications. Active speakers, also known as powered speakers, have built-in amplifiers, which means they can be directly connected to audio sources without the need for an external amplifier. This integration simplifies the setup process and reduces the number of components required in an audio system. Active speakers are often favored for their convenience and ease of use, making them a popular choice for home audio systems, professional studios, and live sound applications. They are designed to deliver precise sound reproduction, with some models offering advanced features such as digital signal processing (DSP) and wireless connectivity options like Bluetooth and Wi-Fi. These features allow users to stream music directly from their devices and customize the sound output to suit their preferences. On the other hand, passive speakers do not have built-in amplifiers and require an external amplifier to function. This setup allows for greater flexibility in terms of system configuration, as users can choose amplifiers that best match their specific needs and preferences. Passive speakers are often preferred by audiophiles and sound engineers who seek to create highly customized audio systems with separate components. They are known for their ability to deliver high-quality sound with minimal distortion, making them ideal for critical listening environments such as recording studios and home theaters. In the Global Hi-Fi Standmount Speakers Market, both active and passive speakers have their own set of advantages and are available in a wide range of designs, sizes, and price points. Manufacturers continue to innovate and introduce new technologies to enhance the performance and appeal of these speakers. For instance, some active speakers now feature built-in digital-to-analog converters (DACs) and room correction technologies that automatically adjust the sound output based on the acoustics of the listening environment. Similarly, passive speakers are being designed with advanced materials and construction techniques to improve sound clarity and durability. As consumer preferences evolve, the demand for both active and passive speakers is expected to grow, driven by the increasing popularity of high-quality audio experiences in various settings. Whether for personal enjoyment or professional use, the Global Hi-Fi Standmount Speakers Market offers a diverse array of options to cater to the needs of different users.

in the Global Hi-Fi Standmount Speakers Market:

The Global Hi-Fi Standmount Speakers Market serves a wide range of applications, each benefiting from the superior sound quality and versatility of these speakers. One of the primary applications is in home audio systems, where Hi-Fi standmount speakers are used to create immersive listening experiences for music, movies, and gaming. These speakers are often paired with other audio components such as amplifiers, subwoofers, and receivers to form a complete home theater setup. The compact size of standmount speakers makes them ideal for use in smaller spaces, while their high-fidelity sound reproduction ensures that users can enjoy clear and detailed audio. In addition to home audio systems, Hi-Fi standmount speakers are widely used in professional audio environments such as recording studios, broadcast facilities, and live sound venues. In these settings, the accuracy and precision of sound reproduction are critical, and standmount speakers are valued for their ability to deliver consistent and reliable performance. Sound engineers and producers rely on these speakers to monitor and mix audio tracks, ensuring that the final product meets the highest standards of quality. Another important application of Hi-Fi standmount speakers is in the realm of personal audio. With the rise of portable music players, smartphones, and streaming services, consumers are increasingly seeking high-quality audio solutions that can enhance their listening experiences. Standmount speakers offer a convenient and effective way to enjoy music at home or in the office, providing a level of sound quality that is often superior to that of traditional portable speakers. Additionally, the growing trend of smart homes and connected devices has led to the integration of Hi-Fi standmount speakers with voice assistants and home automation systems. This allows users to control their audio systems using voice commands and seamlessly integrate their speakers with other smart devices in their homes. As technology continues to advance, the applications for Hi-Fi standmount speakers are expected to expand, offering new opportunities for innovation and growth in the market.

Global Hi-Fi Standmount Speakers Market Outlook:

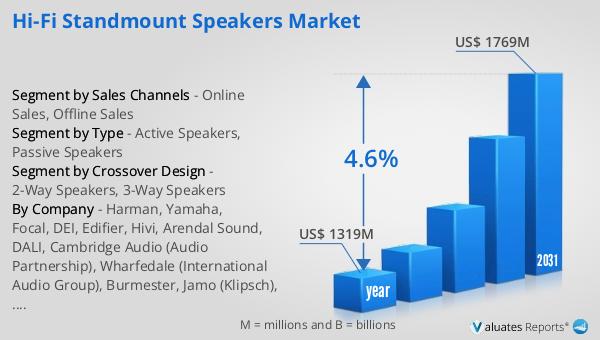

In 2024, the global market for Hi-Fi Standmount Speakers was valued at approximately $1,319 million. This market is anticipated to grow steadily, reaching an estimated value of $1,769 million by the year 2031. This growth represents a compound annual growth rate (CAGR) of 4.6% over the forecast period. The increasing demand for high-quality audio equipment, driven by the rising popularity of home entertainment systems and the growing number of audiophiles worldwide, is a significant factor contributing to this market expansion. Additionally, technological advancements in speaker design and functionality, such as the integration of wireless connectivity and digital signal processing, are enhancing the appeal of Hi-Fi standmount speakers to a broader audience. As consumers continue to seek superior sound experiences, manufacturers are focusing on developing innovative products that cater to diverse preferences and needs. The availability of these speakers through various distribution channels, including online platforms, is also making it easier for consumers to access a wide range of options, further fueling market growth. Overall, the Global Hi-Fi Standmount Speakers Market is poised for continued expansion, offering numerous opportunities for manufacturers, retailers, and consumers alike.

| Report Metric | Details |

| Report Name | Hi-Fi Standmount Speakers Market |

| Accounted market size in year | US$ 1319 million |

| Forecasted market size in 2031 | US$ 1769 million |

| CAGR | 4.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Crossover Design |

|

| Segment by Sales Channels |

|

| Consumption by Region |

|

| By Company | Harman, Yamaha, Focal, DEI, Edifier, Hivi, Arendal Sound, DALI, Cambridge Audio (Audio Partnership), Wharfedale (International Audio Group), Burmester, Jamo (Klipsch), KEF, Dynaudio (GoerTek), Spendor, Wilson Benesch, GoldenEar, ZHUHAI SPARK ELECTRONIC, Monitor Audio |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |