What is Global Mobile Phone Vibration Motor Market?

The Global Mobile Phone Vibration Motor Market is an essential segment of the broader mobile phone industry, focusing on the tiny motors that create vibrations in mobile devices. These motors are crucial for providing tactile feedback to users, enhancing the overall user experience by alerting them to incoming calls, messages, and notifications without the need for sound. As mobile phones have become ubiquitous, the demand for efficient and reliable vibration motors has grown significantly. This market encompasses various types of motors, including Eccentric Rotating Mass (ERM) actuators and Linear Resonant Actuators (LRAs), each offering distinct advantages in terms of performance, power consumption, and cost. The market is driven by the continuous evolution of mobile phone technology, with manufacturers seeking to improve the haptic feedback capabilities of their devices. Additionally, the rise of smartphones and the increasing importance of user interface design have further propelled the demand for advanced vibration motors. As a result, the Global Mobile Phone Vibration Motor Market is poised for steady growth, driven by technological advancements and the ever-increasing penetration of mobile devices worldwide.

Eccentric Rotating Mass (ERM) Actuators, Linear Resonant Actuators (LRAS), Others in the Global Mobile Phone Vibration Motor Market:

Eccentric Rotating Mass (ERM) Actuators, Linear Resonant Actuators (LRAs), and other types of vibration motors play a pivotal role in the Global Mobile Phone Vibration Motor Market. ERM actuators are among the most commonly used vibration motors in mobile phones. They operate by rotating an off-center mass, which creates a centrifugal force that results in vibration. These actuators are favored for their simplicity, cost-effectiveness, and ease of integration into mobile devices. However, they tend to consume more power and may not offer the precise control required for more sophisticated haptic feedback applications. On the other hand, Linear Resonant Actuators (LRAs) are designed to provide more refined and precise vibrations. They work by using a magnetic mass attached to a spring, which moves back and forth when an alternating current is applied. This design allows LRAs to offer faster response times and more accurate haptic feedback, making them ideal for applications that require nuanced tactile sensations. LRAs are generally more energy-efficient than ERMs, which is a significant advantage in battery-powered devices like smartphones. Despite their higher cost, the demand for LRAs is increasing as manufacturers strive to enhance the user experience with more sophisticated haptic feedback. In addition to ERMs and LRAs, other types of vibration motors are also used in the mobile phone market. These include piezoelectric actuators, which use the piezoelectric effect to generate vibrations. Piezoelectric actuators are known for their high precision and low power consumption, making them suitable for applications that require subtle and complex haptic feedback. However, their higher cost and complexity can be a barrier to widespread adoption in cost-sensitive markets. The choice of vibration motor depends on various factors, including the desired haptic feedback, power consumption, cost, and the specific requirements of the mobile device. As the mobile phone industry continues to evolve, manufacturers are exploring new technologies and innovations to improve the performance and efficiency of vibration motors. This includes the development of hybrid actuators that combine the benefits of different types of motors to deliver enhanced haptic feedback. The Global Mobile Phone Vibration Motor Market is characterized by intense competition among manufacturers, with companies striving to develop innovative solutions that meet the changing needs of consumers. As a result, the market is witnessing continuous advancements in vibration motor technology, driven by the demand for improved user experiences and the growing importance of haptic feedback in mobile devices.

Smartphone, Feature Phone in the Global Mobile Phone Vibration Motor Market:

The usage of vibration motors in the Global Mobile Phone Vibration Motor Market is particularly significant in smartphones and feature phones, each serving distinct user needs and market segments. In smartphones, vibration motors are integral to the device's functionality, providing essential tactile feedback that enhances the user experience. With the proliferation of touchscreens, smartphones rely heavily on haptic feedback to simulate the sensation of pressing physical buttons, improving the overall interaction with the device. Vibration motors in smartphones are used for various purposes, including alerting users to incoming calls, messages, and notifications, as well as providing feedback during gaming and other interactive applications. The demand for sophisticated haptic feedback in smartphones has led to the adoption of advanced vibration motors, such as Linear Resonant Actuators (LRAs), which offer precise and nuanced vibrations. These motors are particularly favored in high-end smartphones, where the user experience is a critical differentiator. In contrast, feature phones, which are typically more affordable and less complex than smartphones, also utilize vibration motors, albeit with a focus on basic functionality. In feature phones, vibration motors are primarily used for call and message alerts, providing a silent mode of notification that is essential in various settings. Eccentric Rotating Mass (ERM) actuators are commonly used in feature phones due to their cost-effectiveness and simplicity. While the demand for feature phones has declined with the rise of smartphones, they remain popular in certain markets, particularly in regions where affordability and basic functionality are prioritized. The Global Mobile Phone Vibration Motor Market caters to both smartphones and feature phones, with manufacturers offering a range of solutions to meet the diverse needs of these devices. As the mobile phone industry continues to evolve, the role of vibration motors in enhancing the user experience remains crucial, driving innovation and growth in the market.

Global Mobile Phone Vibration Motor Market Outlook:

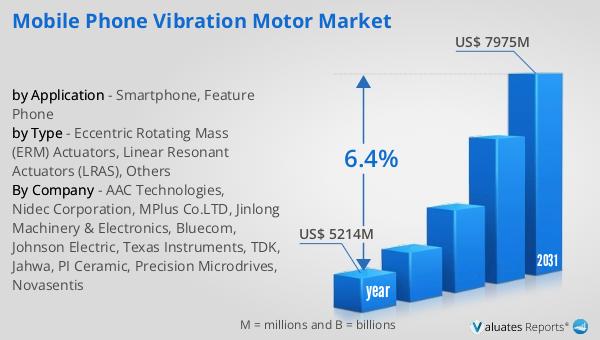

In 2024, the global market for Mobile Phone Vibration Motors was valued at approximately $5,214 million. Looking ahead, this market is expected to expand significantly, reaching an estimated size of $7,975 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 6.4% over the forecast period. The increasing demand for mobile phones, coupled with advancements in haptic feedback technology, is driving this market expansion. As mobile devices become more integral to daily life, the need for efficient and reliable vibration motors continues to rise. These motors play a crucial role in enhancing the user experience by providing tactile feedback, which is essential for various applications, including notifications, gaming, and user interface interactions. The market's growth is further fueled by the continuous innovation in vibration motor technology, with manufacturers striving to develop solutions that offer improved performance, energy efficiency, and cost-effectiveness. As a result, the Global Mobile Phone Vibration Motor Market is poised for steady growth, driven by the increasing penetration of mobile devices and the growing importance of haptic feedback in enhancing the overall user experience.

| Report Metric | Details |

| Report Name | Mobile Phone Vibration Motor Market |

| Accounted market size in year | US$ 5214 million |

| Forecasted market size in 2031 | US$ 7975 million |

| CAGR | 6.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | AAC Technologies, Nidec Corporation, MPlus Co.LTD, Jinlong Machinery & Electronics, Bluecom, Johnson Electric, Texas Instruments, TDK, Jahwa, PI Ceramic, Precision Microdrives, Novasentis |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |