What is Global Carrier Tape for Electronic Components Market?

The Global Carrier Tape for Electronic Components Market is a specialized segment within the broader electronics industry, focusing on the packaging and transportation of electronic components. Carrier tapes are essential for the safe and efficient handling of tiny electronic parts, such as semiconductors, resistors, and capacitors, during manufacturing and assembly processes. These tapes are designed to hold components securely in place, preventing damage and ensuring precise placement during automated assembly. The market for carrier tapes is driven by the increasing demand for electronic devices, advancements in technology, and the need for miniaturization of components. As electronics become more compact and complex, the role of carrier tapes becomes even more critical. They not only protect components from physical damage but also from environmental factors such as moisture and static electricity. The market is characterized by a variety of materials and designs, catering to different types of components and manufacturing processes. With the continuous growth of the electronics industry, the Global Carrier Tape for Electronic Components Market is poised for significant expansion, driven by innovation and the need for efficient manufacturing solutions.

Paper Core Carier Tape, Plastic Core Carier Tape in the Global Carrier Tape for Electronic Components Market:

Carrier tapes are primarily categorized into two types based on the core material used: paper core carrier tapes and plastic core carrier tapes. Each type has its unique characteristics and applications within the Global Carrier Tape for Electronic Components Market. Paper core carrier tapes are typically made from biodegradable materials, making them an environmentally friendly option. They are lightweight and cost-effective, which makes them suitable for a wide range of electronic components. These tapes are often used in applications where environmental impact is a concern, and they provide adequate protection for components during transportation and assembly. However, paper core tapes may not be as durable as their plastic counterparts, especially in environments with high humidity or temperature fluctuations. On the other hand, plastic core carrier tapes are made from materials such as polystyrene, polycarbonate, or polyethylene. These tapes offer superior durability and protection, making them ideal for high-value or sensitive components. Plastic core tapes are resistant to moisture, chemicals, and physical stress, ensuring that components remain secure and undamaged throughout the manufacturing process. They are often used in applications where precision and reliability are paramount, such as in the assembly of semiconductors or other high-tech components. The choice between paper and plastic core carrier tapes depends on various factors, including the specific requirements of the components being handled, the environmental conditions, and cost considerations. Manufacturers must carefully evaluate these factors to select the most appropriate carrier tape for their needs. As the demand for electronic devices continues to grow, the market for both paper and plastic core carrier tapes is expected to expand, driven by the need for efficient and reliable packaging solutions.

Active Components, Passive Components in the Global Carrier Tape for Electronic Components Market:

The Global Carrier Tape for Electronic Components Market plays a crucial role in the assembly and manufacturing of both active and passive components. Active components, such as transistors, diodes, and integrated circuits, require precise handling and placement during assembly. Carrier tapes ensure that these components are securely held in place, preventing damage and ensuring accurate placement on printed circuit boards (PCBs). The use of carrier tapes in the assembly of active components is essential for maintaining the integrity and performance of electronic devices. Passive components, such as resistors, capacitors, and inductors, also benefit from the use of carrier tapes. These components are often smaller and more delicate, making them susceptible to damage during handling and assembly. Carrier tapes provide a protective barrier, preventing physical damage and contamination from dust or moisture. The use of carrier tapes in the assembly of passive components ensures that they are accurately placed and securely held in place, reducing the risk of defects and improving the overall quality of electronic devices. In both cases, carrier tapes play a vital role in the automation of the assembly process, allowing for high-speed and high-precision manufacturing. The use of carrier tapes reduces the need for manual handling, minimizing the risk of human error and increasing production efficiency. As the demand for electronic devices continues to grow, the use of carrier tapes in the assembly of active and passive components is expected to increase, driven by the need for efficient and reliable manufacturing solutions.

Global Carrier Tape for Electronic Components Market Outlook:

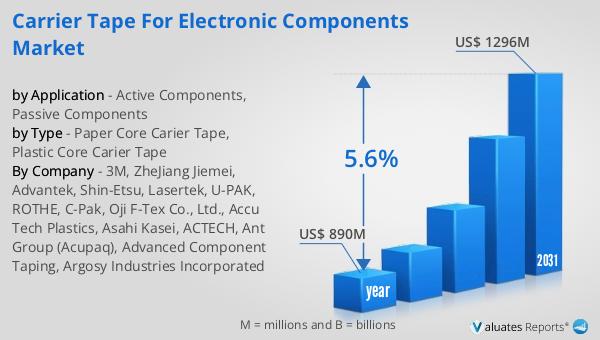

The global market for Carrier Tape for Electronic Components was valued at $890 million in 2024 and is anticipated to grow to a revised size of $1,296 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.6% over the forecast period. This growth is indicative of the increasing demand for electronic components and the need for efficient packaging solutions. Carrier tapes are essential for the safe and efficient handling of electronic components during manufacturing and assembly processes. They provide protection against physical damage, moisture, and static electricity, ensuring that components remain secure and undamaged. The market is driven by advancements in technology, the miniaturization of components, and the increasing demand for electronic devices. As the electronics industry continues to evolve, the role of carrier tapes becomes even more critical, providing manufacturers with the tools they need to produce high-quality electronic devices efficiently. The growth of the Global Carrier Tape for Electronic Components Market is a testament to the importance of these packaging solutions in the modern electronics industry, and their continued development and innovation will be essential for meeting the demands of the future.

| Report Metric | Details |

| Report Name | Carrier Tape for Electronic Components Market |

| Accounted market size in year | US$ 890 million |

| Forecasted market size in 2031 | US$ 1296 million |

| CAGR | 5.6% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | 3M, ZheJiang Jiemei, Advantek, Shin-Etsu, Lasertek, U-PAK, ROTHE, C-Pak, Oji F-Tex Co., Ltd., Accu Tech Plastics, Asahi Kasei, ACTECH, Ant Group (Acupaq), Advanced Component Taping, Argosy Industries Incorporated |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |