What is Global Inline Viscosity Sensors Market?

The Global Inline Viscosity Sensors Market is a specialized segment within the broader field of sensor technology, focusing on devices that measure the viscosity of fluids in real-time as they flow through a system. These sensors are crucial in various industries, including oil and gas, food and beverage, pharmaceuticals, and chemicals, where maintaining the correct viscosity is essential for product quality and process efficiency. Inline viscosity sensors are designed to be integrated directly into the production line, providing continuous monitoring and allowing for immediate adjustments to be made if the viscosity deviates from the desired range. This real-time data collection helps in optimizing processes, reducing waste, and ensuring compliance with industry standards. The market for these sensors is driven by the increasing demand for automation and precision in industrial processes, as well as the need for cost-effective solutions that enhance operational efficiency. As industries continue to evolve and adopt more sophisticated technologies, the role of inline viscosity sensors is expected to grow, offering significant opportunities for innovation and development in this niche market.

Low Temperature, High Temperature in the Global Inline Viscosity Sensors Market:

In the Global Inline Viscosity Sensors Market, temperature plays a critical role in determining the performance and application of these sensors. Low-temperature viscosity sensors are designed to operate in environments where the fluid temperatures are relatively low, typically ranging from sub-zero levels to around 100 degrees Celsius. These sensors are commonly used in industries such as food and beverage, pharmaceuticals, and certain chemical processes where maintaining a specific viscosity at lower temperatures is crucial for product quality and consistency. For instance, in the dairy industry, the viscosity of milk and cream must be carefully monitored to ensure the final product meets quality standards. Low-temperature sensors are engineered to provide accurate readings despite the challenges posed by cold environments, such as condensation and potential freezing of the fluid. They are often equipped with features like thermal insulation and heating elements to maintain optimal sensor performance. On the other hand, high-temperature viscosity sensors are designed to withstand and accurately measure the viscosity of fluids at elevated temperatures, often exceeding 100 degrees Celsius. These sensors are essential in industries such as oil and gas, petrochemicals, and automotive, where processes often involve high-temperature fluids. For example, in the oil refining process, the viscosity of crude oil and its derivatives must be monitored at high temperatures to ensure efficient processing and product quality. High-temperature sensors are built with materials and technologies that can endure extreme heat, such as advanced ceramics and specialized alloys, to prevent sensor degradation and ensure long-term reliability. They may also include cooling systems to protect the sensor electronics from overheating. Both low and high-temperature viscosity sensors are integral to maintaining process control and product quality across various industries. The choice between low and high-temperature sensors depends on the specific requirements of the application, including the temperature range of the fluid being measured and the environmental conditions of the production process. As industries continue to push the boundaries of what is possible with fluid processing, the demand for both types of sensors is expected to grow, driving innovation and development in sensor technology. Manufacturers are continually working to improve the accuracy, durability, and versatility of these sensors to meet the evolving needs of their customers. This includes developing sensors that can operate across a broader range of temperatures, providing more flexibility and reducing the need for multiple sensor types in a single production line.

Industrial, Commercial in the Global Inline Viscosity Sensors Market:

The usage of Global Inline Viscosity Sensors Market in industrial and commercial areas is vast and varied, reflecting the diverse needs of these sectors. In industrial applications, inline viscosity sensors are crucial for maintaining the efficiency and quality of production processes. Industries such as oil and gas, chemicals, and pharmaceuticals rely heavily on these sensors to monitor the viscosity of fluids in real-time, ensuring that the production process remains within the desired parameters. For instance, in the oil and gas industry, the viscosity of crude oil and its derivatives must be carefully monitored to optimize refining processes and ensure product quality. Similarly, in the chemical industry, maintaining the correct viscosity is essential for the production of polymers, paints, and coatings, where even slight deviations can lead to significant quality issues. In commercial applications, inline viscosity sensors are used in sectors such as food and beverage, cosmetics, and consumer goods. These sensors help ensure that products meet quality standards and regulatory requirements by providing real-time data on the viscosity of ingredients and final products. For example, in the food and beverage industry, the viscosity of sauces, syrups, and dairy products must be carefully controlled to ensure consistency and consumer satisfaction. In the cosmetics industry, the viscosity of creams, lotions, and gels is critical for product performance and consumer appeal. Inline viscosity sensors provide the necessary data to make real-time adjustments to the production process, ensuring that products meet the desired specifications. The integration of inline viscosity sensors into industrial and commercial processes offers several benefits, including improved product quality, increased efficiency, and reduced waste. By providing real-time data on fluid viscosity, these sensors enable manufacturers to make immediate adjustments to the production process, minimizing the risk of defects and ensuring that products meet quality standards. This not only enhances customer satisfaction but also reduces costs associated with rework and waste. Additionally, the use of inline viscosity sensors can help manufacturers comply with industry regulations and standards, which is particularly important in sectors such as food and pharmaceuticals where product safety and quality are paramount. As industries continue to evolve and adopt more sophisticated technologies, the role of inline viscosity sensors in industrial and commercial applications is expected to grow. Manufacturers are increasingly looking for ways to improve process efficiency and product quality, and inline viscosity sensors offer a cost-effective solution to achieve these goals. The demand for these sensors is likely to increase as industries seek to enhance their competitive edge and meet the growing expectations of consumers and regulators.

Global Inline Viscosity Sensors Market Outlook:

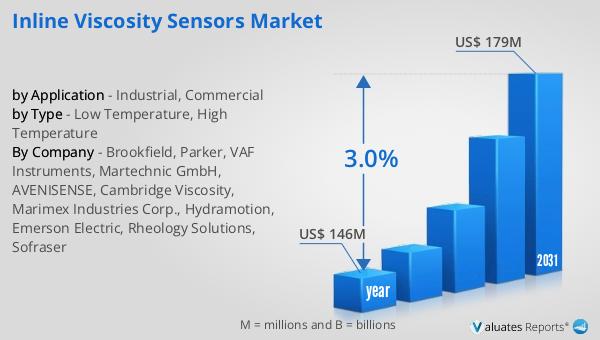

The global market for Inline Viscosity Sensors was valued at approximately $146 million in 2024, and it is anticipated to expand to a revised size of around $179 million by 2031. This growth represents a compound annual growth rate (CAGR) of 3.0% over the forecast period. This steady growth trajectory underscores the increasing importance of inline viscosity sensors across various industries. As businesses strive for greater efficiency and precision in their operations, the demand for real-time monitoring solutions like inline viscosity sensors is on the rise. These sensors provide critical data that helps industries optimize their processes, reduce waste, and ensure product quality, which are key drivers of market growth. The projected growth in the market is also indicative of the broader trend towards automation and digitalization in industrial processes. As industries continue to embrace these trends, the need for advanced sensor technologies that can provide accurate and reliable data in real-time becomes more pronounced. Inline viscosity sensors are well-positioned to meet this demand, offering a valuable tool for industries looking to enhance their operational efficiency and product quality. The market's growth is further supported by ongoing advancements in sensor technology, which are making these devices more accurate, durable, and versatile, thereby expanding their potential applications across different sectors. In conclusion, the global market for inline viscosity sensors is poised for steady growth over the coming years, driven by the increasing demand for real-time monitoring solutions and the broader trend towards automation and digitalization in industrial processes. As industries continue to evolve and adopt more sophisticated technologies, the role of inline viscosity sensors is expected to grow, offering significant opportunities for innovation and development in this niche market.

| Report Metric | Details |

| Report Name | Inline Viscosity Sensors Market |

| Accounted market size in year | US$ 146 million |

| Forecasted market size in 2031 | US$ 179 million |

| CAGR | 3.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Brookfield, Parker, VAF Instruments, Martechnic GmbH, AVENISENSE, Cambridge Viscosity, Marimex Industries Corp., Hydramotion, Emerson Electric, Rheology Solutions, Sofraser |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |