What is Global Flow Chemistry Market?

The Global Flow Chemistry Market is a rapidly evolving sector that focuses on the use of continuous flow processes for chemical reactions. Unlike traditional batch processing, flow chemistry involves the continuous movement of reactants through a reactor, allowing for more efficient and controlled chemical reactions. This method is gaining popularity due to its ability to enhance reaction speed, improve safety, and reduce waste. The market is driven by the growing demand for sustainable and efficient chemical processes across various industries, including pharmaceuticals, petrochemicals, and specialty chemicals. Flow chemistry offers numerous advantages, such as better heat and mass transfer, precise control over reaction parameters, and scalability. These benefits make it an attractive option for industries looking to optimize their production processes and reduce environmental impact. As a result, the Global Flow Chemistry Market is expected to witness significant growth in the coming years, with increasing adoption across different sectors. The market is characterized by the presence of several key players who are investing in research and development to innovate and expand their product offerings. Overall, the Global Flow Chemistry Market represents a promising area of growth and innovation in the chemical industry.

Continuous Stirred Tank Reactors (CSTR), Plug Flow Reactors (PFR), Micro Reactor Systems (MRT), Others in the Global Flow Chemistry Market:

Continuous Stirred Tank Reactors (CSTR), Plug Flow Reactors (PFR), Micro Reactor Systems (MRT), and other types of reactors play a crucial role in the Global Flow Chemistry Market. Each of these reactor types offers unique advantages and is suited for different applications, contributing to the versatility and adaptability of flow chemistry processes. Continuous Stirred Tank Reactors (CSTR) are widely used in the industry due to their simplicity and ability to handle large volumes of reactants. In a CSTR, the reactants are continuously fed into the reactor, where they are mixed and reacted, with the products being continuously removed. This type of reactor is ideal for reactions that require constant agitation and uniform temperature distribution. CSTRs are commonly used in the production of bulk chemicals and pharmaceuticals, where consistent product quality is essential. Plug Flow Reactors (PFR), on the other hand, are designed to allow reactants to flow through a tubular reactor in a plug-like manner, with minimal back-mixing. This design ensures that the reactants experience a uniform residence time, leading to higher conversion rates and selectivity. PFRs are particularly suitable for fast and exothermic reactions, where precise control over reaction conditions is crucial. They are often used in the petrochemical industry for processes such as polymerization and oxidation. Micro Reactor Systems (MRT) represent a more advanced and miniaturized approach to flow chemistry. These systems consist of small channels or capillaries that allow for precise control over reaction parameters, such as temperature, pressure, and flow rate. MRTs offer several advantages, including enhanced heat and mass transfer, reduced reaction times, and the ability to conduct reactions under extreme conditions. They are particularly useful for research and development purposes, as well as for the production of high-value specialty chemicals and pharmaceuticals. Other types of reactors, such as packed bed reactors and membrane reactors, also contribute to the diversity of flow chemistry applications. Packed bed reactors are used for catalytic reactions, where the catalyst is immobilized in a fixed bed, allowing for efficient contact between the reactants and the catalyst. Membrane reactors, on the other hand, combine reaction and separation processes in a single unit, offering the potential for process intensification and improved efficiency. Overall, the variety of reactor types available in the Global Flow Chemistry Market allows for the optimization of chemical processes across different industries, enhancing productivity and sustainability.

Chemical, Pharmaceutical, Others in the Global Flow Chemistry Market:

The Global Flow Chemistry Market finds extensive usage in various sectors, including chemical, pharmaceutical, and others, due to its ability to enhance efficiency, safety, and sustainability. In the chemical industry, flow chemistry is employed to optimize the production of bulk chemicals, specialty chemicals, and intermediates. The continuous nature of flow processes allows for better control over reaction conditions, leading to higher yields and reduced waste. This is particularly important in the production of fine chemicals, where precision and consistency are crucial. Flow chemistry also enables the development of greener processes by minimizing the use of hazardous reagents and solvents, thereby reducing the environmental impact of chemical manufacturing. In the pharmaceutical industry, flow chemistry is revolutionizing drug development and production. The ability to conduct reactions continuously and under controlled conditions allows for the rapid synthesis of complex molecules, accelerating the drug discovery process. Flow chemistry also facilitates the production of active pharmaceutical ingredients (APIs) with high purity and consistency, ensuring the quality and safety of pharmaceutical products. Additionally, the scalability of flow processes enables pharmaceutical companies to quickly transition from laboratory-scale synthesis to large-scale production, reducing time-to-market for new drugs. Beyond the chemical and pharmaceutical sectors, flow chemistry is finding applications in other industries, such as agrochemicals, food and beverage, and materials science. In the agrochemical industry, flow chemistry is used to develop and produce pesticides, herbicides, and fertilizers with improved efficacy and reduced environmental impact. The food and beverage industry benefits from flow chemistry through the development of novel flavors, fragrances, and food additives, enhancing product quality and consumer experience. In materials science, flow chemistry is employed to synthesize advanced materials, such as polymers and nanomaterials, with precise control over their properties and performance. Overall, the versatility and adaptability of flow chemistry make it a valuable tool for various industries seeking to improve their processes and products. The Global Flow Chemistry Market is poised for continued growth as more industries recognize the benefits of adopting flow chemistry technologies to enhance efficiency, sustainability, and innovation.

Global Flow Chemistry Market Outlook:

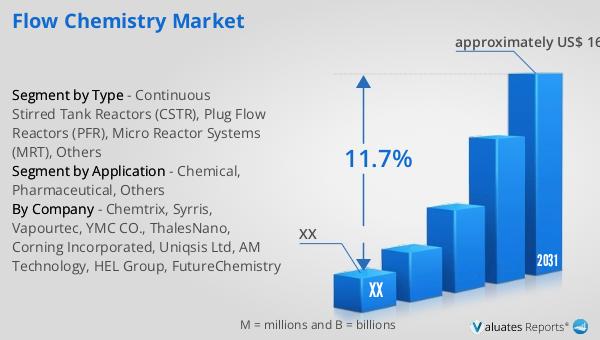

In 2024, the global market size of Flow Chemistry was valued at approximately $77.5 million. This market is projected to experience significant growth, reaching an estimated $166 million by 2031. This growth trajectory is supported by a compound annual growth rate (CAGR) of 11.7% during the forecast period from 2025 to 2031. The market's expansion is driven by the increasing adoption of flow chemistry technologies across various industries, including pharmaceuticals, chemicals, and materials science. The top three players in the Flow Chemistry Market hold a substantial share, accounting for around 40% of the total global market. This concentration of market share indicates the presence of key industry leaders who are driving innovation and development in the field. These companies are investing in research and development to enhance their product offerings and expand their market presence. As the demand for efficient and sustainable chemical processes continues to rise, the Global Flow Chemistry Market is expected to witness further growth and diversification. The market's potential for innovation and its ability to address the evolving needs of various industries make it an attractive area for investment and development. Overall, the Global Flow Chemistry Market is poised for a promising future, with opportunities for growth and advancement in the coming years.

| Report Metric | Details |

| Report Name | Flow Chemistry Market |

| Forecasted market size in 2031 | approximately US$ 166 million |

| CAGR | 11.7% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Chemtrix, Syrris, Vapourtec, YMC CO., ThalesNano, Corning Incorporated, Uniqsis Ltd, AM Technology, HEL Group, FutureChemistry |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |