What is Global Fire Resistant Hydraulic Fluids Market?

The Global Fire Resistant Hydraulic Fluids Market is a specialized segment within the broader hydraulic fluids industry, focusing on fluids that are designed to resist ignition and reduce the risk of fire. These fluids are crucial in industries where high temperatures and potential fire hazards are prevalent, such as mining, metallurgy, marine, and aviation. Fire resistant hydraulic fluids are engineered to provide the necessary lubrication and power transmission while minimizing the risk of fire, which can be catastrophic in industrial settings. The market for these fluids is driven by stringent safety regulations and the need for reliable performance in extreme conditions. As industries continue to prioritize safety and efficiency, the demand for fire resistant hydraulic fluids is expected to grow. These fluids are categorized into different types based on their composition and fire resistance properties, including water-containing fluids and synthetic fluids. Each type offers unique benefits and is suited for specific applications, making the selection of the right fluid critical for optimal performance and safety. The market is characterized by continuous innovation and development, with manufacturers focusing on enhancing the fire resistance, environmental compatibility, and performance of these fluids to meet the evolving needs of various industries.

HFA, HFB, HFC, HFD in the Global Fire Resistant Hydraulic Fluids Market:

In the Global Fire Resistant Hydraulic Fluids Market, there are several types of fluids categorized based on their composition and fire resistance properties: HFA, HFB, HFC, and HFD. HFA fluids are water-based and contain a high percentage of water, typically over 80%. They are known for their excellent fire resistance due to the high water content, which acts as a natural fire suppressant. These fluids are often used in applications where fire safety is a primary concern, but they may require special materials for seals and hoses due to their high water content. HFB fluids are also water-based but contain a higher concentration of oil compared to HFA fluids. This composition provides a balance between fire resistance and lubrication properties, making them suitable for applications where both are required. HFB fluids offer better lubrication than HFA fluids but may not be as fire-resistant due to the higher oil content. HFC fluids are water-glycol based and are known for their excellent fire resistance and lubrication properties. They contain a mixture of water and glycol, which provides good fire resistance while maintaining the necessary lubrication for hydraulic systems. HFC fluids are widely used in industries where both fire safety and performance are critical. HFD fluids are synthetic, non-water-based fluids that offer excellent fire resistance and thermal stability. They are typically used in high-temperature applications where water-based fluids may not perform well. HFD fluids are known for their superior performance in extreme conditions, making them ideal for industries such as aviation and offshore drilling. Each type of fluid has its own advantages and limitations, and the choice of fluid depends on the specific requirements of the application, including fire resistance, lubrication, and environmental considerations. Manufacturers in the Global Fire Resistant Hydraulic Fluids Market continue to innovate and develop new formulations to enhance the performance and safety of these fluids, addressing the evolving needs of various industries.

Mining, Metallurgy, Marine/Offshore, Aviation, Others in the Global Fire Resistant Hydraulic Fluids Market:

The usage of Global Fire Resistant Hydraulic Fluids Market spans across several critical industries, including mining, metallurgy, marine/offshore, aviation, and others. In the mining industry, fire resistant hydraulic fluids are essential due to the high risk of fire in underground operations. These fluids help prevent fires that can be caused by hydraulic system failures, ensuring the safety of workers and equipment. In metallurgy, the high temperatures and presence of molten metals create a significant fire hazard. Fire resistant hydraulic fluids are used to minimize the risk of fire in hydraulic systems, which are crucial for the operation of machinery and equipment in metal processing plants. In the marine and offshore industry, fire resistant hydraulic fluids are vital for ensuring the safety of operations on ships and offshore platforms. These environments are particularly susceptible to fire hazards due to the presence of flammable materials and the confined spaces in which operations take place. Fire resistant fluids help prevent fires in hydraulic systems used for steering, propulsion, and other critical functions. In aviation, the use of fire resistant hydraulic fluids is critical for the safety of aircraft operations. Hydraulic systems are used in various aircraft functions, including landing gear, brakes, and flight controls. The use of fire resistant fluids helps prevent fires that can be caused by hydraulic system failures, ensuring the safety of passengers and crew. Other industries that benefit from the use of fire resistant hydraulic fluids include manufacturing, construction, and transportation. In these industries, the use of fire resistant fluids helps minimize the risk of fire in hydraulic systems, ensuring the safety of workers and equipment. The demand for fire resistant hydraulic fluids is driven by the need for safety and reliability in these critical industries, and manufacturers continue to innovate and develop new formulations to meet the evolving needs of their customers.

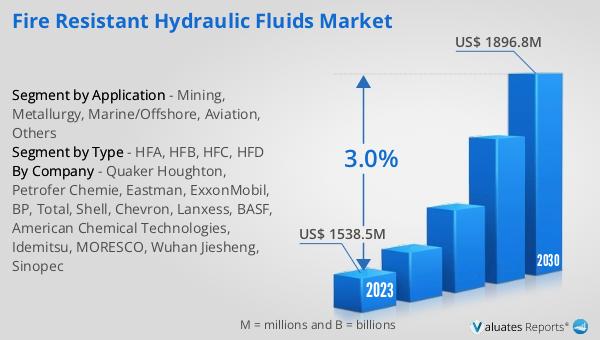

Global Fire Resistant Hydraulic Fluids Market Outlook:

In 2024, the global market size for Fire Resistant Hydraulic Fluids was valued at approximately US$ 1631 million. Looking ahead, it is projected to grow to around US$ 2001 million by the year 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.0% during the forecast period from 2025 to 2031. This steady growth reflects the increasing demand for fire resistant hydraulic fluids across various industries, driven by the need for enhanced safety and performance in high-risk environments. The market's expansion is supported by stringent safety regulations and the continuous innovation in fluid formulations to improve fire resistance and environmental compatibility. As industries such as mining, metallurgy, marine, and aviation continue to prioritize safety and efficiency, the demand for these specialized fluids is anticipated to rise. The projected growth in the market size underscores the importance of fire resistant hydraulic fluids in ensuring the safety and reliability of operations in critical industries. Manufacturers are expected to focus on developing advanced formulations that meet the evolving needs of their customers, further driving the growth of the market. The outlook for the Global Fire Resistant Hydraulic Fluids Market is positive, with opportunities for growth and innovation in the coming years.

| Report Metric | Details |

| Report Name | Fire Resistant Hydraulic Fluids Market |

| CAGR | 3.0% |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Quaker Houghton, Petrofer Chemie, Eastman, ExxonMobil, BP, Total, Shell, Chevron, Lanxess, BASF, American Chemical Technologies, Idemitsu, MORESCO, Wuhan Jiesheng, Sinopec, COGELSA, CNPC |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |