What is Global Floor Grinding Machine Market?

The Global Floor Grinding Machine Market is a dynamic and evolving sector that plays a crucial role in the construction and renovation industries. Floor grinding machines are essential tools used to smooth and polish concrete, marble, granite, and other types of floors. These machines help in leveling uneven surfaces, removing coatings, and preparing floors for further treatment. The market for these machines is driven by the increasing demand for polished concrete floors, which are popular for their aesthetic appeal and durability. Additionally, the rise in construction activities, both residential and commercial, across the globe is fueling the demand for floor grinding machines. Technological advancements have led to the development of more efficient and user-friendly machines, further boosting their adoption. The market is characterized by a wide range of products, catering to different needs and preferences, from small handheld grinders to large industrial machines. As urbanization continues to rise, the demand for floor grinding machines is expected to grow, making it a vital component of the construction equipment market. The market's growth is also supported by the increasing focus on sustainability and the use of eco-friendly materials in construction, which floor grinding machines help facilitate by preparing surfaces for the application of such materials.

Single and Double Headed Grinders, Three and Four Headed Grinders, Others in the Global Floor Grinding Machine Market:

Single and double-headed grinders are among the most commonly used types of floor grinding machines in the Global Floor Grinding Machine Market. These machines are typically used for smaller projects or areas that require precision work. Single-headed grinders have one grinding disc, making them ideal for light-duty tasks such as removing small imperfections or preparing a surface for a new coating. They are easy to maneuver and are often used in residential settings or small commercial spaces. Double-headed grinders, on the other hand, have two grinding discs, which allow for more efficient grinding over larger areas. They provide a balance between precision and productivity, making them suitable for medium-sized projects. These machines are often used in commercial settings where a higher level of surface preparation is required. Three and four-headed grinders are designed for larger projects and are commonly used in industrial settings. These machines have multiple grinding discs, which allow them to cover more surface area in a shorter amount of time. This makes them ideal for large-scale projects such as warehouses, factories, and other industrial facilities. Three-headed grinders offer a good balance between power and maneuverability, making them suitable for a wide range of applications. Four-headed grinders, on the other hand, provide maximum coverage and are often used for the most demanding projects. They are capable of removing thick coatings, leveling uneven surfaces, and polishing large areas to a high shine. These machines are typically used by professional contractors who require high-performance equipment to complete large projects efficiently. In addition to single, double, three, and four-headed grinders, there are other types of floor grinding machines available in the market. These include planetary grinders, which have multiple rotating discs that move in a circular motion. This design allows for more even grinding and polishing, making them ideal for achieving a high-quality finish. Planetary grinders are often used for polishing concrete floors in commercial and residential settings. Another type of grinder is the edge grinder, which is specifically designed for grinding and polishing the edges of floors. These machines are essential for achieving a uniform finish across the entire floor surface. They are often used in conjunction with larger grinders to ensure that every part of the floor is properly prepared and polished. The Global Floor Grinding Machine Market is diverse and caters to a wide range of applications. Whether it's a small residential project or a large industrial facility, there is a floor grinding machine available to meet the specific needs of the job. The market continues to evolve with new technologies and innovations, providing users with more efficient and effective tools for their projects. As the demand for polished concrete floors and other high-quality finishes continues to grow, the market for floor grinding machines is expected to expand, offering new opportunities for manufacturers and users alike.

Commercial, Industrial, Public in the Global Floor Grinding Machine Market:

The usage of floor grinding machines in the Global Floor Grinding Machine Market spans across various sectors, including commercial, industrial, and public areas. In commercial settings, these machines are widely used for preparing and polishing floors in retail spaces, office buildings, hotels, and restaurants. The aesthetic appeal of polished concrete floors, combined with their durability and low maintenance requirements, makes them a popular choice for commercial properties. Floor grinding machines are used to remove old coatings, level uneven surfaces, and polish floors to a high shine, creating an attractive and professional appearance. In addition to enhancing the visual appeal of commercial spaces, these machines also help improve safety by creating slip-resistant surfaces. In industrial settings, floor grinding machines are essential tools for maintaining and preparing floors in factories, warehouses, and manufacturing facilities. These environments often require heavy-duty equipment capable of handling large areas and tough materials. Floor grinding machines are used to remove thick coatings, such as epoxy or paint, and to level uneven surfaces caused by heavy machinery or foot traffic. By creating a smooth and even surface, these machines help improve the efficiency and safety of industrial operations. Additionally, polished concrete floors are resistant to chemicals and abrasions, making them ideal for industrial settings where durability is a key concern. Public areas, such as airports, train stations, and government buildings, also benefit from the use of floor grinding machines. These spaces experience high foot traffic and require durable and easy-to-maintain flooring solutions. Floor grinding machines are used to prepare and polish floors in public areas, ensuring they can withstand the wear and tear of daily use. The machines help create a clean and professional appearance, enhancing the overall experience for visitors and users. In addition to improving the aesthetics of public spaces, floor grinding machines also contribute to safety by creating slip-resistant surfaces that reduce the risk of accidents. Overall, the Global Floor Grinding Machine Market plays a vital role in the construction and maintenance of commercial, industrial, and public spaces. The versatility and efficiency of these machines make them indispensable tools for achieving high-quality finishes and durable flooring solutions. As the demand for polished concrete floors and other advanced flooring options continues to grow, the market for floor grinding machines is expected to expand, offering new opportunities for manufacturers and users alike. The continued development of new technologies and innovations in the field will further enhance the capabilities and applications of floor grinding machines, ensuring their continued relevance in the construction and maintenance industries.

Global Floor Grinding Machine Market Outlook:

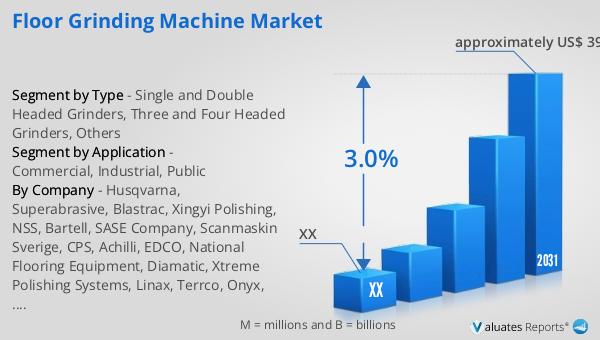

In 2024, the global market size for floor grinding machines was valued at approximately US$ 323 million. Looking ahead, this market is projected to grow, reaching an estimated value of around US$ 396 million by the year 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 3.0% during the forecast period from 2025 to 2031. This steady growth can be attributed to several factors, including the increasing demand for polished concrete floors, which are favored for their aesthetic appeal and durability. Additionally, the rise in construction activities worldwide, both in residential and commercial sectors, is driving the demand for efficient and versatile floor grinding machines. Technological advancements in the design and functionality of these machines are also contributing to market growth, as they offer improved performance and ease of use. As urbanization continues to expand, the need for high-quality flooring solutions is expected to rise, further fueling the demand for floor grinding machines. The market's growth is also supported by the increasing focus on sustainability and the use of eco-friendly materials in construction, which floor grinding machines help facilitate by preparing surfaces for the application of such materials. Overall, the Global Floor Grinding Machine Market is poised for steady growth, driven by a combination of technological advancements, increasing construction activities, and a growing preference for polished concrete floors.

| Report Metric | Details |

| Report Name | Floor Grinding Machine Market |

| Forecasted market size in 2031 | approximately US$ 396 million |

| CAGR | 3.0% |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| By Region |

|

| By Company | Husqvarna, Superabrasive, Blastrac, Xingyi Polishing, NSS, Bartell, SASE Company, Scanmaskin Sverige, CPS, Achilli, EDCO, National Flooring Equipment, Diamatic, Xtreme Polishing Systems, Linax, Terrco, Onyx, Substrate Technology, Aztec, StoneKor, Klindex |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |