What is Global Light Vehicle Front End Modules Sales Market?

The Global Light Vehicle Front End Modules Sales Market refers to the industry focused on the production and distribution of front-end modules for light vehicles, which include passenger cars and light commercial vehicles. These modules are integral components of a vehicle's front structure, typically encompassing elements such as the bumper, headlights, radiator, and other components that contribute to the vehicle's aesthetic and functional design. The market is driven by the increasing demand for lightweight and fuel-efficient vehicles, as manufacturers strive to meet stringent environmental regulations and consumer preferences for better fuel economy. Additionally, advancements in materials and technology have enabled the development of more sophisticated and integrated front-end modules, enhancing vehicle performance and safety. The market is characterized by a high level of competition among key players, who are continuously innovating to offer more efficient and cost-effective solutions. As the automotive industry evolves, the Global Light Vehicle Front End Modules Sales Market is expected to grow, driven by the rising production of light vehicles and the increasing adoption of advanced front-end module technologies.

in the Global Light Vehicle Front End Modules Sales Market:

The Global Light Vehicle Front End Modules Sales Market caters to a diverse range of customers, each with specific needs and preferences. One of the primary types of front-end modules used by customers is the traditional steel-based module. These modules are known for their durability and strength, making them a popular choice among manufacturers who prioritize vehicle safety and structural integrity. However, the weight of steel modules can be a drawback, as it impacts fuel efficiency. To address this, many manufacturers are turning to lightweight materials such as aluminum and composites. Aluminum front-end modules offer a good balance between strength and weight, providing improved fuel efficiency without compromising on safety. Composite materials, on the other hand, are gaining traction due to their exceptional lightweight properties and flexibility in design. These materials allow for more innovative and aerodynamic designs, which can enhance vehicle performance and aesthetics. Another type of front-end module that is gaining popularity is the modular front-end system. This approach involves the integration of various components into a single module, which can be easily assembled and installed. This not only reduces manufacturing costs but also allows for greater customization and flexibility in vehicle design. Customers who prioritize cost-effectiveness and efficiency often opt for modular systems, as they offer significant savings in terms of production time and labor costs. Additionally, the growing trend towards electric and hybrid vehicles is influencing the types of front-end modules used in the market. These vehicles require specialized modules that can accommodate the unique design and cooling requirements of electric powertrains. As a result, manufacturers are developing front-end modules with integrated cooling systems and aerodynamic features to optimize the performance of electric and hybrid vehicles. Overall, the Global Light Vehicle Front End Modules Sales Market offers a wide range of options to cater to the diverse needs of customers, from traditional steel modules to advanced composite and modular systems. As the market continues to evolve, manufacturers are likely to focus on developing more innovative and sustainable solutions to meet the changing demands of the automotive industry.

in the Global Light Vehicle Front End Modules Sales Market:

The applications of Global Light Vehicle Front End Modules Sales Market are vast and varied, reflecting the diverse needs of the automotive industry. One of the primary applications is in the production of passenger cars, where front-end modules play a crucial role in defining the vehicle's appearance and performance. These modules are designed to enhance the vehicle's aerodynamics, improve fuel efficiency, and provide structural support in the event of a collision. In addition to passenger cars, front-end modules are also used in light commercial vehicles, such as vans and small trucks. These vehicles require robust and durable front-end modules that can withstand the demands of commercial use, including frequent loading and unloading, long-distance travel, and exposure to harsh environmental conditions. The use of advanced materials and technologies in front-end modules helps to improve the durability and performance of light commercial vehicles, making them more reliable and efficient for business operations. Another important application of front-end modules is in the development of electric and hybrid vehicles. As the automotive industry shifts towards more sustainable and environmentally friendly solutions, the demand for specialized front-end modules that can accommodate the unique requirements of electric powertrains is increasing. These modules are designed to optimize the cooling and aerodynamics of electric vehicles, ensuring optimal performance and efficiency. Furthermore, front-end modules are also used in the customization and modification of vehicles. Many consumers and businesses seek to personalize their vehicles with unique front-end designs, which can be achieved through the use of modular and composite front-end modules. This allows for greater flexibility and creativity in vehicle design, enabling manufacturers to cater to the specific preferences and needs of their customers. Overall, the applications of Global Light Vehicle Front End Modules Sales Market are diverse and continue to expand as the automotive industry evolves. Manufacturers are constantly innovating to develop more advanced and efficient front-end modules that can meet the changing demands of the market, from traditional passenger cars to cutting-edge electric vehicles.

Global Light Vehicle Front End Modules Sales Market Outlook:

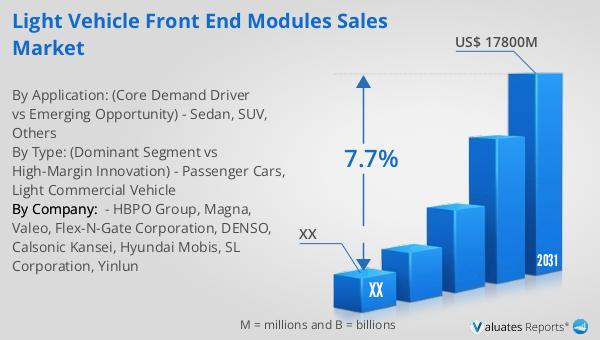

In 2024, the Global Light Vehicle Front End Modules Market was valued at approximately $10,670 million. Projections indicate that by 2031, this market is expected to grow to an adjusted size of around $17,800 million, reflecting a compound annual growth rate (CAGR) of 7.7% during the forecast period from 2025 to 2031. This growth is indicative of the increasing demand for front-end modules in the automotive industry, driven by factors such as the rising production of light vehicles and the adoption of advanced technologies. The market is dominated by the top five manufacturers, who collectively hold a significant share of over 65%. This concentration of market power highlights the competitive nature of the industry, with key players continuously innovating to maintain their market position. In terms of product segments, passenger cars represent the largest share, accounting for over 85% of the market. This dominance is attributed to the high production and sales volume of passenger cars globally, as well as the increasing consumer preference for vehicles with enhanced safety and performance features. As the market continues to evolve, manufacturers are likely to focus on developing more efficient and cost-effective front-end modules to meet the growing demand from the automotive industry.

| Report Metric | Details |

| Report Name | Light Vehicle Front End Modules Sales Market |

| Forecasted market size in 2031 | US$ 17800 million |

| CAGR | 7.7% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | HBPO Group, Magna, Valeo, Flex-N-Gate Corporation, DENSO, Calsonic Kansei, Hyundai Mobis, SL Corporation, Yinlun |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |