What is Global Lysine Sales Market?

The global lysine sales market is a dynamic and essential segment of the broader amino acids market. Lysine is an indispensable amino acid that plays a crucial role in animal nutrition, particularly in the livestock industry. It is primarily used as a feed additive to enhance the growth and development of animals, especially poultry and swine. The demand for lysine is driven by the increasing consumption of meat and meat products worldwide, as it helps improve feed efficiency and animal health. The market is characterized by a few dominant players who hold a significant share, ensuring a steady supply of lysine to meet the growing needs of the agricultural sector. Additionally, the market is influenced by factors such as advancements in production technologies, fluctuations in raw material prices, and regulatory policies affecting the feed industry. As the global population continues to rise, the demand for lysine is expected to grow, making it a vital component in the quest for sustainable and efficient animal agriculture. The market's growth is also supported by the rising awareness of the benefits of lysine in animal nutrition, leading to its increased adoption across various regions.

in the Global Lysine Sales Market:

In the global lysine sales market, various types of lysine are utilized by different customers based on their specific needs and applications. The most common types of lysine include lysine hydrochloride, lysine sulfate, and liquid lysine. Lysine hydrochloride is the most widely used form, known for its high purity and effectiveness in animal feed. It is particularly favored in regions with stringent quality standards, as it provides a reliable source of lysine for enhancing animal growth and feed efficiency. Lysine sulfate, on the other hand, is a cost-effective alternative that offers a slightly lower lysine content but is still highly effective in promoting animal health. It is often preferred in markets where cost considerations are paramount, providing a balance between performance and affordability. Liquid lysine is another variant that is gaining popularity due to its ease of handling and mixing in feed formulations. It is particularly useful in large-scale operations where efficiency and convenience are critical. The choice of lysine type often depends on factors such as regional preferences, cost constraints, and specific nutritional requirements of the livestock being raised. In addition to these primary types, there are also specialized lysine products designed for specific applications, such as lysine monohydrochloride for aquaculture and lysine acetate for pharmaceutical uses. These specialized forms cater to niche markets where specific attributes of lysine are required to meet unique challenges. The diversity of lysine types available in the market ensures that customers can select the most appropriate form to meet their specific needs, whether it be for enhancing animal growth, improving feed efficiency, or addressing specific nutritional deficiencies. The global lysine market is thus characterized by a wide range of products that cater to the diverse needs of its customers, ensuring that the benefits of lysine can be harnessed across various applications and industries. As the market continues to evolve, the development of new and innovative lysine products is expected to further expand the range of options available to customers, driving growth and innovation in the industry.

in the Global Lysine Sales Market:

Lysine finds applications across a wide range of industries, with its primary use being in animal nutrition. In the livestock industry, lysine is an essential feed additive that helps improve the growth and development of animals, particularly poultry and swine. By enhancing feed efficiency, lysine contributes to better weight gain and overall health of the animals, making it a crucial component in animal agriculture. Beyond its role in animal nutrition, lysine is also used in the food and beverage industry as a nutritional supplement. It is added to various food products to enhance their protein content and nutritional value, catering to the growing demand for high-protein diets among health-conscious consumers. In the pharmaceutical industry, lysine is utilized in the formulation of various medications and supplements, particularly those aimed at improving immune function and promoting overall health. Its role in collagen synthesis makes it a valuable ingredient in skincare products, where it is used to enhance skin elasticity and reduce the appearance of wrinkles. Additionally, lysine is used in the production of certain industrial products, such as adhesives and coatings, where its unique chemical properties contribute to improved performance and durability. The versatility of lysine and its wide range of applications make it a valuable commodity in various sectors, driving demand and innovation in the global lysine sales market. As industries continue to explore new uses for lysine, its applications are expected to expand further, contributing to the growth and diversification of the market. The ongoing research and development efforts in the field of lysine are likely to lead to the discovery of new applications and benefits, further solidifying its position as a key ingredient in multiple industries.

Global Lysine Sales Market Outlook:

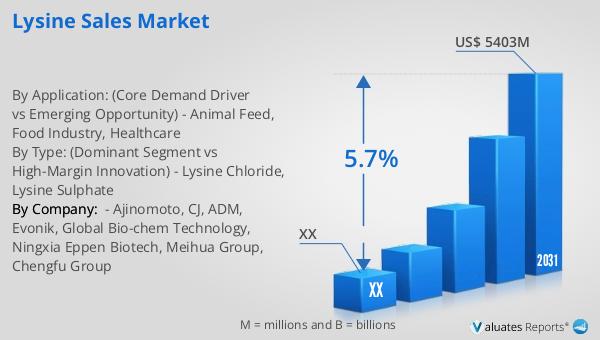

The global lysine market is poised for significant growth, with its size estimated at $3,685 million in 2024. By 2031, it is projected to reach an adjusted size of $5,403 million, reflecting a compound annual growth rate (CAGR) of 5.7% during the forecast period from 2025 to 2031. The market is dominated by the top five manufacturers, who collectively hold approximately 70% of the market share, underscoring the competitive nature of the industry. The Asia-Pacific (APAC) region emerges as the largest market, accounting for about 51% of the global share, followed by the Americas and Europe, which together hold over 47% of the market. Among the various product segments, lysine sulfate stands out as the largest, with a share exceeding 62%. This dominance is attributed to its cost-effectiveness and widespread use in animal feed formulations. The market's growth is driven by the increasing demand for meat and meat products, as well as the rising awareness of the benefits of lysine in animal nutrition. As the global population continues to grow, the demand for lysine is expected to rise, making it a vital component in the quest for sustainable and efficient animal agriculture. The market's expansion is further supported by advancements in production technologies and the development of new and innovative lysine products, which are expected to drive growth and innovation in the industry.

| Report Metric | Details |

| Report Name | Lysine Sales Market |

| Forecasted market size in 2031 | US$ 5403 million |

| CAGR | 5.7% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Ajinomoto, CJ, ADM, Evonik, Global Bio-chem Technology, Ningxia Eppen Biotech, Meihua Group, Chengfu Group |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |