What is Global Ladder Sales Market?

The Global Ladder Sales Market refers to the worldwide industry involved in the production, distribution, and sale of ladders. Ladders are essential tools used across various sectors, including construction, maintenance, and household activities, to provide access to heights that are otherwise unreachable. The market encompasses a wide range of ladder types, such as step ladders, extension ladders, and platform ladders, each designed to meet specific needs and safety standards. The demand for ladders is driven by factors such as urbanization, industrial growth, and the increasing need for infrastructure development. Additionally, advancements in ladder materials, such as aluminum and fiberglass, have enhanced durability and safety, further boosting market growth. The market is characterized by a mix of established manufacturers and new entrants, all striving to innovate and capture a share of the expanding market. As safety regulations become more stringent, manufacturers are focusing on producing ladders that not only meet but exceed safety standards, ensuring user confidence and compliance. The Global Ladder Sales Market is a dynamic and evolving sector, reflecting broader economic trends and technological advancements.

in the Global Ladder Sales Market:

The Global Ladder Sales Market offers a diverse array of ladder types, each catering to the unique needs of various customers. Step ladders are among the most common types, favored for their versatility and ease of use. They are self-supporting and can be used in a variety of settings, from household chores to professional tasks. Extension ladders, on the other hand, are designed for reaching greater heights and are commonly used in construction and maintenance work. These ladders can be extended to various lengths, making them ideal for tasks that require access to elevated areas. Platform ladders provide a stable working surface, making them suitable for tasks that require prolonged standing or the use of tools. They are often used in painting, electrical work, and other trades where stability and safety are paramount. Telescopic ladders are a modern innovation, offering portability and ease of storage. They can be extended and locked at various lengths, making them a popular choice for both professionals and DIY enthusiasts. Multi-position ladders are highly adaptable, capable of being configured into different shapes to suit a wide range of tasks. This flexibility makes them a valuable tool for professionals who need to tackle diverse projects. Specialty ladders, such as attic ladders and library ladders, cater to specific needs and are designed with particular environments in mind. Attic ladders, for example, are retractable and installed in ceilings to provide access to attic spaces, while library ladders are often mounted on rails to facilitate access to high shelves. The choice of ladder type is influenced by factors such as the nature of the task, the working environment, and safety considerations. For instance, fiberglass ladders are preferred in electrical work due to their non-conductive properties, while aluminum ladders are lightweight and resistant to corrosion, making them suitable for outdoor use. The market also sees a demand for ladders with enhanced safety features, such as slip-resistant steps and stabilizing bars, as consumers become more safety-conscious. Manufacturers are continually innovating to meet these demands, offering ladders that combine functionality with safety and convenience. The Global Ladder Sales Market is thus characterized by a wide variety of products, each designed to meet the specific needs of its users, from homeowners to professionals across various industries.

in the Global Ladder Sales Market:

Ladders are indispensable tools across a multitude of applications, reflecting the diverse needs of the Global Ladder Sales Market. In the construction industry, ladders are essential for tasks such as painting, roofing, and installation work. They provide workers with the necessary height and stability to perform their duties safely and efficiently. Maintenance and repair work also heavily rely on ladders, whether it's for fixing electrical systems, cleaning gutters, or conducting routine inspections. In the realm of home improvement, ladders are a staple for DIY enthusiasts undertaking projects like painting, decorating, or accessing storage spaces. The retail sector utilizes ladders for stocking shelves and managing inventory in warehouses and stores. In the agricultural sector, ladders are used for tasks such as fruit picking and tree pruning, where access to elevated areas is required. The entertainment industry also finds applications for ladders, particularly in stage setup and lighting installation. In the realm of emergency services, ladders are crucial for rescue operations, allowing firefighters and rescue personnel to reach high places quickly and safely. The versatility of ladders extends to the transportation sector, where they are used for vehicle maintenance and loading operations. In educational institutions, ladders are employed for maintenance tasks and accessing high storage areas. The demand for ladders in these varied applications underscores their importance as a tool that enhances productivity and safety across different fields. As industries continue to evolve, the applications for ladders are likely to expand, driven by technological advancements and changing work environments. The Global Ladder Sales Market thus plays a critical role in supporting a wide range of activities, providing the tools necessary for safe and efficient work at height.

Global Ladder Sales Market Outlook:

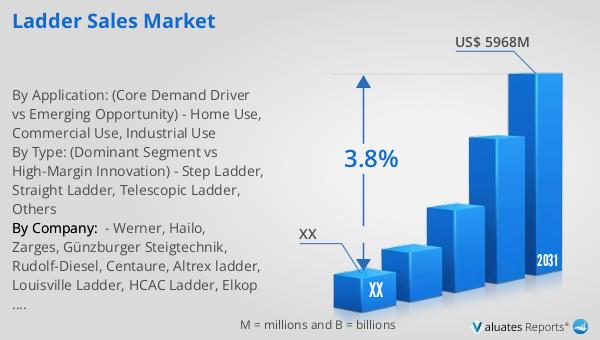

The global ladder market, valued at approximately $4,665 million in 2024, is projected to grow to an estimated $5,968 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 3.8% from 2025 to 2031. This steady growth reflects the increasing demand for ladders across various sectors, driven by factors such as urbanization, industrial expansion, and the need for infrastructure development. The market is competitive, with the top four manufacturers collectively holding a market share exceeding 10%. This indicates a significant level of concentration among leading players, who are likely to continue influencing market trends through innovation and strategic partnerships. The focus on safety and compliance with regulatory standards is expected to drive product development, as manufacturers strive to offer ladders that meet the evolving needs of consumers. The market's growth trajectory suggests a positive outlook, with opportunities for both established companies and new entrants to capture a share of the expanding market. As the demand for ladders continues to rise, the Global Ladder Sales Market is poised for sustained growth, reflecting broader economic trends and the ongoing need for safe and reliable access solutions.

| Report Metric | Details |

| Report Name | Ladder Sales Market |

| Forecasted market size in 2031 | US$ 5968 million |

| CAGR | 3.8% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Werner, Hailo, Zarges, Günzburger Steigtechnik, Rudolf-Diesel, Centaure, Altrex ladder, Louisville Ladder, HCAC Ladder, Elkop Ltd, FACAL, KRAUSE-Werk, Faraone, NERESSY, Mauderer Alutechnik, WAKÜ, KTL Ladders, Lyte, Euroline, Industrias Consolidadas S.A. de C.V., EscalumexEscalumex, SA de CV, Síntese Escadas, Alumasa, W Bertolo, SBA – Peças Acabadas de Alumínio, Zhejiang Aopeng, Alulev Escadas, Little Giant Ladders, China Jinmao, Tricam, Escaleve, Suzhou Pica Aluminum Industry Ltd., Suzhou Zhongchuang, Hasegawa, Fujian Xiangxin Hardware, Yangming Holding Group Co., Ltd, Foshan Wright Home Furnishing Products Co., Ltd, Shanghai Ruiju METAL Products Co., Ltd, Yongkang Weige Industry & Trade Co., Ltd |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |