What is Global Plumbing Fitting Sales Market?

The Global Plumbing Fitting Sales Market is a dynamic and essential segment of the construction and home improvement industries. Plumbing fittings are crucial components that ensure the proper functioning of water supply and drainage systems in residential, commercial, and industrial buildings. This market encompasses a wide range of products, including faucets, valves, pipes, and connectors, which are used to control and direct the flow of water. The demand for plumbing fittings is driven by factors such as urbanization, population growth, and the increasing need for modern infrastructure. As more people move to urban areas, the construction of new buildings and the renovation of existing ones create a steady demand for plumbing solutions. Additionally, the growing awareness of water conservation and the need for efficient plumbing systems contribute to the market's expansion. The market is characterized by a mix of established players and new entrants, each vying to offer innovative and sustainable products. With advancements in technology, manufacturers are focusing on developing smart plumbing solutions that enhance convenience and efficiency. Overall, the Global Plumbing Fitting Sales Market plays a vital role in supporting the infrastructure needs of societies worldwide, ensuring access to clean water and effective waste management.

in the Global Plumbing Fitting Sales Market:

The Global Plumbing Fitting Sales Market offers a diverse array of products tailored to meet the varying needs of customers across different sectors. Faucets, for instance, are one of the most prominent types of plumbing fittings, accounting for nearly 60% of the market share. These are essential in both residential and commercial settings, providing a controlled flow of water for various purposes. Faucets come in numerous designs and functionalities, ranging from traditional models to modern, touchless versions that promote hygiene and water conservation. Valves are another critical component, used to regulate the flow and pressure of water within plumbing systems. They are indispensable in both residential and industrial applications, ensuring the safe and efficient operation of water supply networks. Pipes and connectors form the backbone of any plumbing system, facilitating the transport of water from one point to another. These components are available in various materials, including copper, PVC, and PEX, each offering distinct advantages in terms of durability, flexibility, and cost. The choice of material often depends on the specific requirements of the project, such as the type of building, the local climate, and the budget constraints. In addition to these core components, the market also includes a range of accessories and fittings designed to enhance the functionality and aesthetics of plumbing systems. These include showerheads, hose bibs, and water filtration systems, each catering to specific customer preferences and needs. The increasing focus on sustainability has led to the development of eco-friendly plumbing solutions, such as low-flow faucets and water-saving showerheads, which help reduce water consumption without compromising performance. Smart plumbing technologies are also gaining traction, with products like digital faucets and leak detection systems offering enhanced convenience and efficiency. These innovations are particularly appealing to tech-savvy consumers and businesses looking to optimize their water usage and reduce operational costs. The market is further segmented based on the end-user, with residential, commercial, and industrial sectors each exhibiting unique demands and preferences. Residential customers, for example, often prioritize aesthetics and ease of use, while commercial and industrial clients may focus more on durability and compliance with regulatory standards. The competitive landscape of the Global Plumbing Fitting Sales Market is characterized by a mix of established brands and emerging players, each striving to capture a share of this lucrative market. Companies are investing in research and development to introduce new products and technologies that meet the evolving needs of their customers. Strategic partnerships and collaborations are also common, enabling firms to expand their product offerings and reach new markets. Overall, the Global Plumbing Fitting Sales Market is a vibrant and evolving sector, driven by innovation, sustainability, and the ever-changing needs of consumers worldwide.

in the Global Plumbing Fitting Sales Market:

The applications of the Global Plumbing Fitting Sales Market are vast and varied, reflecting the essential role these products play in modern infrastructure. In residential settings, plumbing fittings are integral to the functionality and comfort of homes. They are used in kitchens, bathrooms, and laundry rooms, providing access to clean water for cooking, cleaning, and personal hygiene. The aesthetic appeal of plumbing fixtures is also a significant consideration for homeowners, with many opting for stylish and contemporary designs that complement their interior decor. In commercial environments, plumbing fittings are crucial for maintaining the operational efficiency of businesses. Restaurants, hotels, and office buildings rely on robust plumbing systems to meet the demands of their daily operations. In these settings, durability and reliability are paramount, as any disruption to the water supply can have significant implications for business continuity. Industrial applications of plumbing fittings are equally important, with factories and manufacturing plants requiring specialized solutions to handle large volumes of water and other fluids. These environments often demand high-performance fittings that can withstand extreme temperatures and pressures, ensuring the safe and efficient operation of industrial processes. The healthcare sector is another critical area where plumbing fittings play a vital role. Hospitals and clinics require reliable and hygienic plumbing systems to support patient care and maintain sanitary conditions. In these settings, the use of touchless faucets and antimicrobial materials is becoming increasingly common, helping to reduce the risk of infection and improve overall hygiene. The education sector also benefits from the Global Plumbing Fitting Sales Market, with schools and universities requiring efficient plumbing systems to support their facilities. From restrooms to science labs, plumbing fittings are essential for providing students and staff with access to clean water and sanitation. The hospitality industry is another significant user of plumbing fittings, with hotels and resorts investing in high-quality fixtures to enhance the guest experience. From luxurious bathrooms to state-of-the-art kitchens, plumbing fittings are a key component of the hospitality offering, contributing to the comfort and satisfaction of guests. The public sector, including government buildings and infrastructure projects, also relies on plumbing fittings to support their operations. These projects often require large-scale plumbing solutions that can accommodate the needs of diverse populations, ensuring access to clean water and sanitation for all. Overall, the applications of the Global Plumbing Fitting Sales Market are diverse and far-reaching, underscoring the importance of these products in supporting the infrastructure needs of societies worldwide.

Global Plumbing Fitting Sales Market Outlook:

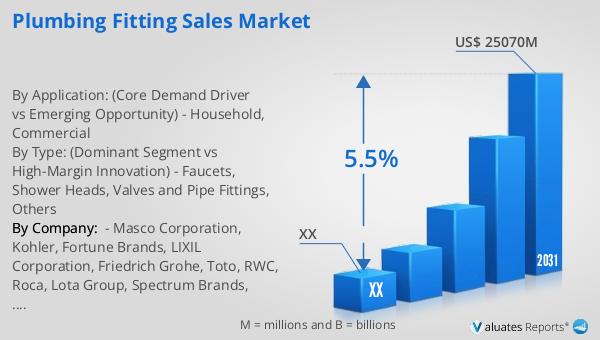

In 2024, the global plumbing fitting market was valued at approximately $17,330 million. Looking ahead, it is projected to grow to an adjusted size of around $25,070 million by 2031, reflecting a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2025 to 2031. This growth trajectory highlights the increasing demand for plumbing fittings across various sectors, driven by factors such as urbanization, infrastructure development, and the need for efficient water management solutions. The market is characterized by a competitive landscape, with the top five manufacturers holding a significant share of over 20%. This concentration of market power underscores the influence of leading players in shaping industry trends and driving innovation. Among the different product segments, faucets stand out as the largest, commanding nearly 60% of the market share. This dominance can be attributed to the widespread use of faucets in both residential and commercial settings, where they serve as essential components for controlling water flow. The popularity of faucets is further bolstered by the growing emphasis on water conservation and the adoption of smart technologies that enhance user convenience and efficiency. As the market continues to evolve, manufacturers are likely to focus on developing innovative products that cater to the diverse needs of consumers, ensuring sustained growth and competitiveness in the global plumbing fitting market.

| Report Metric | Details |

| Report Name | Plumbing Fitting Sales Market |

| Forecasted market size in 2031 | US$ 25070 million |

| CAGR | 5.5% |

| Forecasted years | 2025 - 2031 |

| By Type: (Dominant Segment vs High-Margin Innovation) |

|

| By Application: (Core Demand Driver vs Emerging Opportunity) |

|

| By Region |

|

| By Company: | Masco Corporation, Kohler, Fortune Brands, LIXIL Corporation, Friedrich Grohe, Toto, RWC, Roca, Lota Group, Spectrum Brands, Globe UNION Industrial Corp, Jacuzzi, Huayi, Elkay, Lasco, Maax, Ideal Standard, Villeroy & Boch, Jaquar Group, Sanitec, Hansgrohe, Sunlot Group, Hindware, CERA Sanitaryware |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |