What is Global Medical Stainless Steel Tubing Market?

The Global Medical Stainless Steel Tubing Market is a specialized segment within the broader medical device industry, focusing on the production and distribution of stainless steel tubes used in various medical applications. These tubes are essential components in medical devices and equipment, offering durability, corrosion resistance, and biocompatibility, which are crucial for maintaining hygiene and ensuring patient safety. The market encompasses a wide range of products, including seamless and welded tubes, each serving specific purposes in medical settings. The demand for medical stainless steel tubing is driven by the increasing prevalence of chronic diseases, advancements in medical technology, and the growing need for minimally invasive surgical procedures. As healthcare systems worldwide continue to expand and modernize, the need for high-quality medical tubing is expected to rise, making this market a vital part of the global healthcare infrastructure. The market's growth is also supported by stringent regulatory standards that ensure the safety and efficacy of medical devices, further emphasizing the importance of reliable and high-quality tubing solutions.

Seamless Pipe, Welded Pipe in the Global Medical Stainless Steel Tubing Market:

Seamless and welded pipes are two primary types of tubing used in the Global Medical Stainless Steel Tubing Market, each with distinct characteristics and applications. Seamless pipes are manufactured through a process that involves piercing a solid billet of stainless steel to create a hollow tube, which is then elongated and shaped to the desired dimensions. This method results in a pipe with a uniform structure and no welded seams, making it highly resistant to pressure and ideal for applications requiring high strength and reliability. Seamless pipes are often used in critical medical applications, such as in the production of catheters, cannulas, and other devices that require precise dimensions and superior mechanical properties. Their ability to withstand high pressure and temperature variations makes them suitable for use in demanding environments, such as in surgical procedures and diagnostic equipment.

Hospital, Clinic, Other in the Global Medical Stainless Steel Tubing Market:

On the other hand, welded pipes are produced by rolling a flat strip of stainless steel into a tubular shape and then welding the edges together to form a seam. This process is generally more cost-effective than producing seamless pipes, making welded pipes a popular choice for applications where cost considerations are a priority. Despite the presence of a seam, modern welding techniques ensure that welded pipes offer excellent strength and durability, making them suitable for a wide range of medical applications. Welded pipes are commonly used in the manufacturing of medical instruments, hospital furniture, and other equipment where the demands on the tubing are less stringent than in high-pressure applications. The choice between seamless and welded pipes often depends on the specific requirements of the application, including factors such as pressure, temperature, and the need for precision.

Global Medical Stainless Steel Tubing Market Outlook:

In the context of the Global Medical Stainless Steel Tubing Market, both seamless and welded pipes play crucial roles in meeting the diverse needs of the healthcare industry. The choice between these two types of tubing is influenced by various factors, including the intended use, cost considerations, and regulatory requirements. As the demand for advanced medical devices continues to grow, manufacturers are increasingly focusing on developing innovative tubing solutions that offer enhanced performance, reliability, and cost-effectiveness. This has led to the development of new materials and manufacturing techniques that further enhance the properties of stainless steel tubing, ensuring that it remains a vital component in the medical device industry. The ongoing advancements in medical technology and the increasing emphasis on patient safety and quality of care are expected to drive the demand for both seamless and welded pipes in the coming years, highlighting the importance of this market segment in the global healthcare landscape.

| Report Metric | Details |

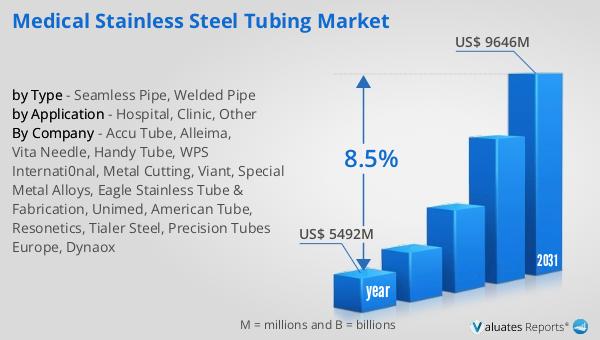

| Report Name | Medical Stainless Steel Tubing Market |

| Accounted market size in year | US$ 5492 million |

| Forecasted market size in 2031 | US$ 9646 million |

| CAGR | 8.5% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Accu Tube, Alleima, Vita Needle, Handy Tube, WPS Internati0nal, Metal Cutting, Viant, Special Metal Alloys, Eagle Stainless Tube & Fabrication, Unimed, American Tube, Resonetics, Tialer Steel, Precision Tubes Europe, Dynaox |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |