What is Global Semiconductor Epoxy Molding Compound Market?

The Global Semiconductor Epoxy Molding Compound Market is a crucial segment within the electronics industry, primarily focusing on the materials used to encapsulate and protect semiconductor devices. These compounds are essential for safeguarding delicate electronic components from environmental factors such as moisture, dust, and mechanical stress. Epoxy molding compounds are known for their excellent thermal stability, mechanical strength, and electrical insulation properties, making them ideal for use in semiconductor packaging. The market for these compounds is driven by the increasing demand for consumer electronics, automotive electronics, and advancements in communication technologies. As the world becomes more interconnected and reliant on electronic devices, the need for reliable and efficient semiconductor packaging solutions continues to grow. This market is characterized by continuous innovation and development, with manufacturers striving to enhance the performance and sustainability of their products. The global semiconductor epoxy molding compound market is poised for significant growth, driven by technological advancements and the ever-increasing demand for electronic devices across various sectors.

Bulk Molding Compounds, Sheet Molding Compounds in the Global Semiconductor Epoxy Molding Compound Market:

Bulk Molding Compounds (BMC) and Sheet Molding Compounds (SMC) are two significant types of materials used in the Global Semiconductor Epoxy Molding Compound Market. BMC is a ready-to-mold, glass-fiber reinforced thermoset polymer material, primarily used for its excellent electrical insulation properties, dimensional stability, and resistance to corrosion and heat. It is composed of a mixture of resin paste, chopped glass fibers, and various additives, which are combined to form a thick, dough-like compound. BMC is widely used in the electronics industry for manufacturing components that require high precision and durability, such as connectors, insulators, and housings for electronic devices. Its ability to withstand high temperatures and harsh environmental conditions makes it an ideal choice for applications in automotive electronics and industrial equipment. On the other hand, Sheet Molding Compounds (SMC) are a type of composite material made by impregnating a fiber mat with a thermosetting resin. SMCs are known for their high strength-to-weight ratio, excellent surface finish, and superior mechanical properties. They are typically used in applications where lightweight and high-performance materials are required, such as in the automotive and aerospace industries. In the context of the semiconductor epoxy molding compound market, SMCs are used for encapsulating and protecting semiconductor devices, providing a robust barrier against environmental factors. The use of SMCs in semiconductor packaging helps improve the reliability and longevity of electronic components, ensuring their optimal performance in various applications. Both BMC and SMC play a crucial role in the semiconductor epoxy molding compound market, offering unique advantages that cater to different application needs. The choice between BMC and SMC depends on the specific requirements of the application, such as the desired mechanical properties, thermal stability, and environmental resistance. As the demand for advanced electronic devices continues to rise, the need for high-quality molding compounds like BMC and SMC is expected to grow, driving innovation and development in this market segment. Manufacturers are continually exploring new formulations and processing techniques to enhance the performance and sustainability of these materials, ensuring they meet the evolving needs of the electronics industry.

Semiconductor Packaging, Electronic Component, Others in the Global Semiconductor Epoxy Molding Compound Market:

The Global Semiconductor Epoxy Molding Compound Market finds extensive usage in various areas, including semiconductor packaging, electronic components, and other applications. In semiconductor packaging, epoxy molding compounds are used to encapsulate and protect semiconductor chips, ensuring their reliability and performance. These compounds provide a robust barrier against environmental factors such as moisture, dust, and mechanical stress, which can adversely affect the functionality of semiconductor devices. The use of epoxy molding compounds in semiconductor packaging helps improve the thermal and mechanical stability of the devices, ensuring their optimal performance in various applications. As the demand for smaller, more efficient electronic devices continues to grow, the need for advanced semiconductor packaging solutions is expected to rise, driving the demand for epoxy molding compounds in this sector. In the realm of electronic components, epoxy molding compounds are used to manufacture a wide range of products, including connectors, insulators, and housings for electronic devices. These compounds offer excellent electrical insulation properties, dimensional stability, and resistance to heat and corrosion, making them ideal for use in high-performance electronic components. The use of epoxy molding compounds in electronic components helps enhance their durability and reliability, ensuring they can withstand the rigors of everyday use. As the electronics industry continues to evolve, with advancements in technology and increasing demand for innovative products, the need for high-quality epoxy molding compounds is expected to grow, driving innovation and development in this market segment. Beyond semiconductor packaging and electronic components, epoxy molding compounds are also used in various other applications, such as automotive electronics, industrial equipment, and consumer electronics. In automotive electronics, these compounds are used to encapsulate and protect electronic control units, sensors, and other critical components, ensuring their reliability and performance in harsh environmental conditions. In industrial equipment, epoxy molding compounds are used to manufacture components that require high precision and durability, such as connectors and insulators. In consumer electronics, these compounds are used to encapsulate and protect delicate electronic components, ensuring their longevity and performance. The versatility and reliability of epoxy molding compounds make them an essential material in various industries, driving their demand and growth in the global market.

Global Semiconductor Epoxy Molding Compound Market Outlook:

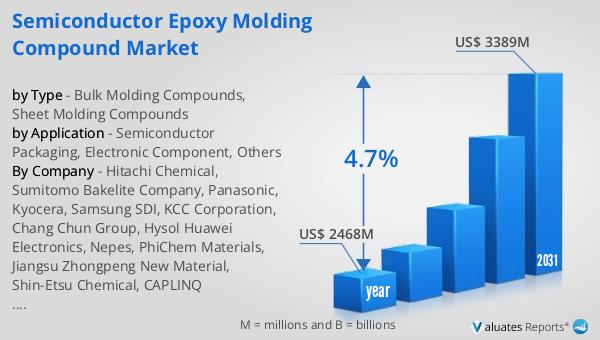

The global market for Semiconductor Epoxy Molding Compound was valued at approximately $2.468 billion in 2024. This market is anticipated to experience significant growth over the coming years, with projections indicating that it will reach an estimated size of $3.389 billion by 2031. This growth trajectory reflects a compound annual growth rate (CAGR) of 4.7% during the forecast period. The increasing demand for semiconductor devices, driven by advancements in technology and the proliferation of electronic devices, is a key factor contributing to this market expansion. As industries such as consumer electronics, automotive, and telecommunications continue to evolve, the need for reliable and efficient semiconductor packaging solutions becomes increasingly critical. Epoxy molding compounds play a vital role in ensuring the performance and longevity of semiconductor devices, making them an essential component in the electronics industry. The projected growth of the semiconductor epoxy molding compound market underscores the importance of these materials in supporting the development and advancement of electronic technologies. As the market continues to expand, manufacturers are likely to focus on innovation and sustainability, developing new formulations and processing techniques to meet the evolving needs of the industry.

| Report Metric | Details |

| Report Name | Semiconductor Epoxy Molding Compound Market |

| Accounted market size in year | US$ 2468 million |

| Forecasted market size in 2031 | US$ 3389 million |

| CAGR | 4.7% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Hitachi Chemical, Sumitomo Bakelite Company, Panasonic, Kyocera, Samsung SDI, KCC Corporation, Chang Chun Group, Hysol Huawei Electronics, Nepes, PhiChem Materials, Jiangsu Zhongpeng New Material, Shin-Etsu Chemical, CAPLINQ Corporation, Scienchem |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |