What is Global Lump Metal Chrome Market?

The Global Lump Metal Chrome Market is a significant segment within the broader metal industry, primarily driven by its extensive use in various industrial applications. Lump metal chrome, a form of chromium, is a crucial component in the production of stainless steel and other alloys due to its corrosion resistance and hardness. This market is characterized by the demand for high-quality chrome with varying degrees of purity, which directly impacts its application and value. The market's growth is influenced by factors such as industrialization, technological advancements, and the increasing demand for durable and corrosion-resistant materials. Additionally, the market is shaped by the availability of raw materials, mining activities, and geopolitical factors that affect supply chains. As industries continue to expand globally, the demand for lump metal chrome is expected to rise, driven by its essential role in enhancing the properties of metals used in construction, automotive, aerospace, and other sectors. The market's dynamics are also affected by environmental regulations and sustainability practices, which encourage the development of eco-friendly mining and processing techniques. Overall, the Global Lump Metal Chrome Market plays a vital role in supporting industrial growth and technological innovation across various sectors.

Purity: 98%, Purity: 98.5%, Purity: 99% in the Global Lump Metal Chrome Market:

In the Global Lump Metal Chrome Market, purity levels are a critical factor that determines the quality and application of the metal. Purity levels such as 98%, 98.5%, and 99% are commonly referenced, each serving distinct purposes based on their chemical composition and physical properties. A purity level of 98% indicates that the chrome contains 98% chromium, with the remaining 2% comprising other elements or impurities. This level of purity is often suitable for applications where high corrosion resistance is required but where the presence of minor impurities does not significantly affect performance. It is commonly used in the production of certain types of stainless steel and in applications where cost-effectiveness is a priority. Moving up the scale, a purity level of 98.5% offers a slightly higher chromium content, which enhances the metal's resistance to oxidation and corrosion. This makes it ideal for more demanding industrial applications, such as in the manufacturing of high-performance alloys and components that are exposed to harsh environments. The increased purity also contributes to improved mechanical properties, making it a preferred choice for industries that require materials with superior strength and durability. At the top end of the purity spectrum, 99% purity represents the highest standard of chrome available in the market. This level of purity is essential for applications that demand the utmost in quality and performance, such as in aerospace and defense industries, where materials are subjected to extreme conditions and must meet stringent specifications. The high chromium content ensures exceptional resistance to corrosion and wear, making it indispensable in the production of critical components like turbine blades, engine parts, and other high-stress applications. Additionally, 99% purity chrome is often used in the production of superalloys, which are essential for advanced engineering applications. The choice of purity level in the Global Lump Metal Chrome Market is influenced by several factors, including cost considerations, specific application requirements, and the desired balance between performance and price. Manufacturers and end-users must carefully evaluate these factors to select the appropriate grade of chrome that meets their needs while optimizing cost-efficiency. As the market continues to evolve, advancements in refining and processing technologies are expected to enhance the availability and affordability of high-purity chrome, further expanding its applications across various industries.

Steelmaking, Casting, Welding Consumables, Others in the Global Lump Metal Chrome Market:

The Global Lump Metal Chrome Market finds extensive usage across several key areas, including steelmaking, casting, welding consumables, and other industrial applications. In steelmaking, lump metal chrome is a vital ingredient in the production of stainless steel, which is renowned for its corrosion resistance, strength, and aesthetic appeal. The addition of chrome to steel enhances its ability to withstand harsh environments, making it ideal for use in construction, automotive, and household appliances. The demand for stainless steel continues to grow, driven by its versatility and the increasing need for durable materials in infrastructure development and consumer goods. In the casting industry, lump metal chrome is used to produce high-quality castings that require excellent surface finish and dimensional accuracy. Chrome's properties, such as its high melting point and resistance to thermal shock, make it suitable for casting applications where precision and durability are paramount. This includes the production of components for the automotive, aerospace, and machinery industries, where cast parts must meet stringent performance standards. The use of chrome in casting also contributes to the production of intricate designs and complex shapes, expanding the possibilities for innovation in product design. Welding consumables represent another significant area of application for lump metal chrome. Chrome is used in the production of welding electrodes and wires, which are essential for joining metal components in various industries. The presence of chrome in welding consumables enhances the weld's strength and resistance to corrosion, ensuring the longevity and reliability of welded structures. This is particularly important in industries such as shipbuilding, construction, and pipeline manufacturing, where welded joints are subjected to extreme conditions and must maintain their integrity over time. Beyond these primary applications, lump metal chrome is also used in other industrial sectors, including the production of refractory materials, pigments, and chemicals. In the refractory industry, chrome is used to manufacture bricks and linings that can withstand high temperatures and corrosive environments, making them suitable for use in furnaces, kilns, and reactors. Chrome-based pigments are valued for their vibrant colors and stability, finding applications in paints, coatings, and plastics. Additionally, chrome compounds are used in the chemical industry for various processes, including electroplating and the production of catalysts. The diverse applications of lump metal chrome underscore its importance as a versatile and indispensable material in modern industry. As technological advancements continue to drive innovation, the demand for high-quality chrome is expected to grow, supporting the development of new products and solutions across multiple sectors.

Global Lump Metal Chrome Market Outlook:

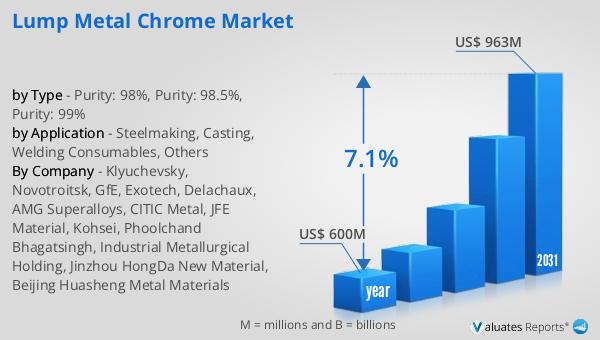

The global market for Lump Metal Chrome was valued at US$ 600 million in the year 2024 and is projected to reach a revised size of US$ 963 million by 2031, growing at a compound annual growth rate (CAGR) of 7.1% during the forecast period. This growth trajectory reflects the increasing demand for high-quality chrome across various industries, driven by its essential role in enhancing the properties of metals and alloys. The market's expansion is supported by factors such as industrialization, technological advancements, and the rising need for durable and corrosion-resistant materials. As industries continue to evolve and innovate, the demand for lump metal chrome is expected to rise, contributing to the market's robust growth. The projected increase in market size also highlights the importance of chrome in supporting industrial growth and technological innovation. With its wide range of applications in steelmaking, casting, welding consumables, and other sectors, lump metal chrome remains a critical component in the production of high-performance materials. The market's growth is further bolstered by advancements in refining and processing technologies, which enhance the availability and affordability of high-purity chrome. As a result, the Global Lump Metal Chrome Market is poised for continued expansion, driven by its indispensable role in modern industry.

| Report Metric | Details |

| Report Name | Lump Metal Chrome Market |

| Accounted market size in year | US$ 600 million |

| Forecasted market size in 2031 | US$ 963 million |

| CAGR | 7.1% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Klyuchevsky, Novotroitsk, GfE, Exotech, Delachaux, AMG Superalloys, CITIC Metal, JFE Material, Kohsei, Phoolchand Bhagatsingh, Industrial Metallurgical Holding, Jinzhou HongDa New Material, Beijing Huasheng Metal Materials |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |