What is Global Lithium Battery Lamination Stacking Machines Market?

The Global Lithium Battery Lamination Stacking Machines Market is a specialized segment within the broader battery manufacturing industry, focusing on the production of machines that assemble lithium battery cells through a process known as lamination stacking. This process is crucial for creating efficient and high-performance lithium batteries, which are essential for a wide range of applications, from electric vehicles to consumer electronics. The market for these machines is driven by the increasing demand for lithium batteries, which are favored for their high energy density, long life, and lightweight properties. As industries worldwide shift towards more sustainable and energy-efficient solutions, the need for advanced battery technologies has surged, propelling the growth of the lamination stacking machines market. These machines are designed to enhance the precision and efficiency of battery production, ensuring that the cells are stacked accurately and consistently, which is vital for the performance and safety of the batteries. The market is characterized by continuous technological advancements, with manufacturers investing in research and development to improve machine capabilities and meet the evolving needs of battery producers. As a result, the Global Lithium Battery Lamination Stacking Machines Market is poised for significant growth, driven by the expanding applications of lithium batteries across various sectors.

Z-type Laminating Type, Cutting and Laminating Type, Thermal Laminating Type, Rolling and Laminating Type in the Global Lithium Battery Lamination Stacking Machines Market:

In the realm of the Global Lithium Battery Lamination Stacking Machines Market, several types of laminating processes are employed, each with its unique characteristics and applications. The Z-type Laminating Type is a method where the electrode sheets are stacked in a zigzag pattern, resembling the letter 'Z'. This technique is particularly advantageous for enhancing the energy density of the battery, as it allows for a more compact arrangement of the electrode materials. The Z-type laminating process is often used in applications where space is a constraint, such as in portable electronic devices and compact energy storage systems. On the other hand, the Cutting and Laminating Type involves cutting the electrode sheets into precise shapes before stacking them. This method ensures that each layer is perfectly aligned, which is crucial for maintaining the structural integrity and performance of the battery. The precision cutting also minimizes material wastage, making it a cost-effective solution for large-scale battery production. Thermal Laminating Type is another approach where heat is applied to bond the electrode layers together. This method is particularly useful for creating strong and durable bonds, which are essential for batteries that are subjected to high-stress environments, such as in electric vehicles and industrial applications. The thermal laminating process also enhances the thermal stability of the battery, reducing the risk of overheating and improving safety. Lastly, the Rolling and Laminating Type involves rolling the electrode sheets into a cylindrical shape before stacking them. This technique is commonly used in the production of cylindrical batteries, which are widely used in consumer electronics and power tools. The rolling process ensures that the electrode materials are evenly distributed, which is crucial for maintaining consistent performance and extending the battery's lifespan. Each of these laminating types plays a vital role in the Global Lithium Battery Lamination Stacking Machines Market, catering to the diverse needs of battery manufacturers and enabling the production of high-quality lithium batteries for various applications.

Electric Vehicles, Energy Storage, Consumer Electronics, Medical, Others in the Global Lithium Battery Lamination Stacking Machines Market:

The Global Lithium Battery Lamination Stacking Machines Market finds extensive usage across several key areas, each benefiting from the unique advantages offered by lithium batteries. In the realm of Electric Vehicles (EVs), these machines are indispensable for producing high-performance batteries that power modern electric cars. The precision and efficiency of lamination stacking machines ensure that the battery cells are assembled with utmost accuracy, which is crucial for the performance, range, and safety of EVs. As the automotive industry increasingly shifts towards electric mobility, the demand for advanced battery technologies continues to rise, driving the growth of the lamination stacking machines market. In the Energy Storage sector, lithium batteries are favored for their ability to store large amounts of energy in a compact form. Lamination stacking machines play a critical role in producing batteries that are used in renewable energy systems, such as solar and wind power installations, where efficient energy storage is essential for balancing supply and demand. The Consumer Electronics industry also relies heavily on lithium batteries, which power a wide range of devices, from smartphones to laptops. The precision offered by lamination stacking machines ensures that these batteries are compact, lightweight, and capable of delivering consistent performance, which is vital for the functionality and user experience of electronic devices. In the Medical field, lithium batteries are used in various medical devices, including portable diagnostic equipment and implantable devices. The reliability and safety of these batteries are paramount, and lamination stacking machines ensure that the cells are assembled to meet stringent quality standards. Lastly, in other sectors such as aerospace and defense, lithium batteries are used in applications where high energy density and reliability are critical. The versatility and efficiency of lamination stacking machines make them an essential component in the production of batteries that meet the demanding requirements of these industries. Overall, the Global Lithium Battery Lamination Stacking Machines Market plays a pivotal role in enabling the widespread adoption of lithium batteries across diverse sectors, contributing to advancements in technology and sustainability.

Global Lithium Battery Lamination Stacking Machines Market Outlook:

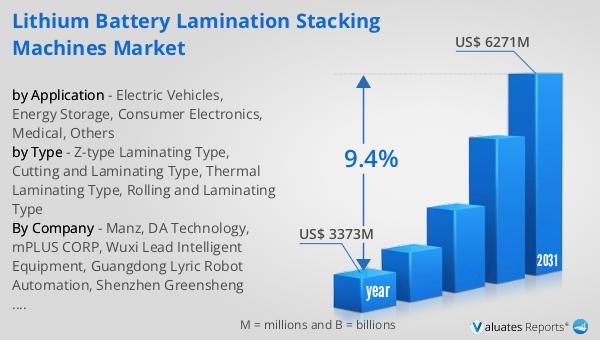

The global market for Lithium Battery Lamination Stacking Machines was valued at approximately $3,373 million in 2024. It is anticipated to expand significantly, reaching an estimated size of $6,271 million by 2031. This growth trajectory represents a compound annual growth rate (CAGR) of 9.4% over the forecast period. This robust growth can be attributed to the increasing demand for lithium batteries across various industries, driven by the global shift towards sustainable energy solutions and the rising adoption of electric vehicles. As industries continue to prioritize energy efficiency and environmental sustainability, the need for advanced battery technologies has become more pronounced. The lamination stacking machines market is poised to benefit from this trend, as these machines are essential for producing high-quality lithium batteries that meet the performance and safety standards required by modern applications. The market's expansion is also supported by continuous technological advancements, with manufacturers investing in research and development to enhance machine capabilities and cater to the evolving needs of battery producers. As a result, the Global Lithium Battery Lamination Stacking Machines Market is expected to witness substantial growth, driven by the increasing applications of lithium batteries across various sectors.

| Report Metric | Details |

| Report Name | Lithium Battery Lamination Stacking Machines Market |

| Accounted market size in year | US$ 3373 million |

| Forecasted market size in 2031 | US$ 6271 million |

| CAGR | 9.4% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| by Type |

|

| by Application |

|

| Production by Region |

|

| Consumption by Region |

|

| By Company | Manz, DA Technology, mPLUS CORP, Wuxi Lead Intelligent Equipment, Guangdong Lyric Robot Automation, Shenzhen Greensheng Technology, Geesun Intelligent Technology, Shenzhen Colibri Technologies, Shenzhen Yinghe Technology, Haimuxing Laser Technology, Yingfukang Industrial Technology, Chaoye Precision Equipment (Funeng Oriental Equipment Technology), Kejing STAR Technology, Fenghesheng Intelligent Technology |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |