What is Global Professional Wearable Devices in Healthcare Market?

The Global Professional Wearable Devices in Healthcare Market refers to the rapidly evolving sector of technology-driven devices designed to be worn on the body, which are used to monitor, diagnose, and treat various health conditions. These devices are revolutionizing the healthcare industry by providing real-time data and insights into a patient's health, thereby enabling more personalized and efficient care. They encompass a wide range of products, including fitness trackers, smartwatches, and specialized medical devices that can monitor vital signs, detect irregularities, and even administer medication. The market is driven by advancements in technology, increasing health awareness, and the growing demand for remote patient monitoring. As healthcare systems worldwide strive to improve patient outcomes and reduce costs, wearable devices offer a promising solution by facilitating continuous health monitoring and early detection of potential health issues. This market is expected to grow significantly as more healthcare providers and patients recognize the benefits of integrating wearable technology into their daily routines. The convenience, accuracy, and accessibility of these devices make them an essential component of modern healthcare, paving the way for a future where health management is more proactive and personalized.

Wearable Medical Detection Devices, Wearable Rehabilitation Therapy Devices, Wearable Drug Delivery Devices in the Global Professional Wearable Devices in Healthcare Market:

Wearable Medical Detection Devices are a crucial segment of the Global Professional Wearable Devices in Healthcare Market. These devices are designed to monitor and detect various health parameters, providing real-time data that can be used for early diagnosis and intervention. They include devices like heart rate monitors, glucose monitors, and blood pressure monitors, which are often integrated into smartwatches or standalone devices. The primary advantage of these devices is their ability to provide continuous monitoring, allowing for the early detection of potential health issues before they become critical. This continuous data stream can be invaluable for healthcare providers, enabling them to make informed decisions about a patient's care plan. Wearable Rehabilitation Therapy Devices, on the other hand, are designed to assist patients in their recovery process. These devices can track physical activity, monitor progress, and provide feedback to both patients and healthcare providers. They are particularly useful for patients recovering from surgery or injury, as they can help ensure that rehabilitation exercises are performed correctly and consistently. By providing real-time feedback, these devices can help motivate patients to adhere to their rehabilitation programs, ultimately leading to better outcomes. Wearable Drug Delivery Devices represent another innovative application of wearable technology in healthcare. These devices are designed to administer medication in a controlled and precise manner, often through the skin. They can be programmed to deliver specific doses at predetermined intervals, reducing the risk of human error and ensuring that patients receive the correct amount of medication. This is particularly beneficial for patients with chronic conditions who require regular medication, as it can improve adherence and reduce the burden of managing complex medication schedules. Overall, these wearable devices are transforming the healthcare landscape by providing more personalized, efficient, and effective care. They empower patients to take an active role in managing their health, while also providing healthcare providers with the tools they need to deliver better care. As technology continues to advance, the potential applications of wearable devices in healthcare are virtually limitless, promising a future where healthcare is more accessible, proactive, and patient-centered.

Hospital, Clinic, Others in the Global Professional Wearable Devices in Healthcare Market:

The usage of Global Professional Wearable Devices in Healthcare Market extends across various settings, including hospitals, clinics, and other healthcare facilities. In hospitals, wearable devices are increasingly being used to monitor patients' vital signs continuously. This real-time monitoring allows healthcare providers to detect any changes in a patient's condition promptly, enabling timely interventions. For instance, wearable heart rate monitors and oxygen saturation sensors can alert medical staff to potential issues, such as arrhythmias or respiratory distress, before they become critical. This proactive approach can significantly improve patient outcomes and reduce the length of hospital stays. In clinics, wearable devices are often used to enhance patient engagement and adherence to treatment plans. By providing patients with real-time feedback on their health metrics, these devices can motivate individuals to take a more active role in managing their health. For example, a patient with hypertension might use a wearable blood pressure monitor to track their readings throughout the day, allowing them to identify patterns and make lifestyle changes to improve their condition. This data can also be shared with healthcare providers, facilitating more informed discussions during clinic visits. Beyond hospitals and clinics, wearable devices are also being utilized in other healthcare settings, such as home care and telemedicine. In home care, wearable devices enable remote monitoring of patients, allowing healthcare providers to track their health status without the need for frequent in-person visits. This is particularly beneficial for elderly patients or those with chronic conditions, as it allows them to receive continuous care while remaining in the comfort of their own homes. In telemedicine, wearable devices play a crucial role in bridging the gap between patients and healthcare providers. By providing real-time health data, these devices enable virtual consultations that are just as effective as in-person visits. Patients can share their health metrics with their healthcare providers during video calls, allowing for accurate assessments and timely interventions. This is especially important in rural or underserved areas, where access to healthcare facilities may be limited. Overall, the integration of wearable devices into various healthcare settings is transforming the way care is delivered. By providing real-time data and facilitating remote monitoring, these devices are helping to improve patient outcomes, increase efficiency, and reduce healthcare costs. As the technology continues to evolve, the potential applications of wearable devices in healthcare are vast, promising a future where healthcare is more accessible, personalized, and patient-centered.

Global Professional Wearable Devices in Healthcare Market Outlook:

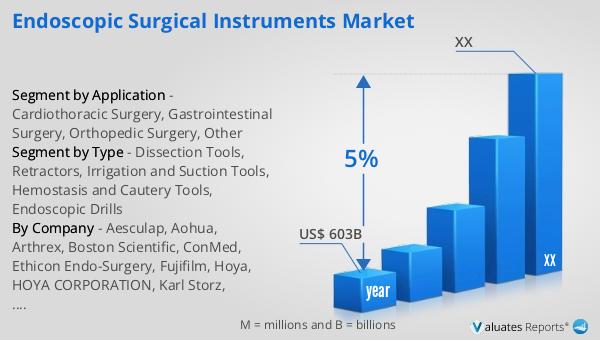

Our research indicates that the global market for medical devices is projected to reach approximately $603 billion in 2023, with an anticipated growth rate of 5% annually over the next six years. This growth is driven by several factors, including technological advancements, increasing demand for innovative healthcare solutions, and a growing emphasis on personalized medicine. As the healthcare industry continues to evolve, the role of medical devices is becoming increasingly important in improving patient outcomes and enhancing the efficiency of healthcare delivery. The integration of advanced technologies, such as artificial intelligence and the Internet of Things, into medical devices is enabling more accurate diagnostics, better patient monitoring, and more effective treatments. Additionally, the rising prevalence of chronic diseases and an aging population are contributing to the increased demand for medical devices, as they offer solutions for managing long-term health conditions and improving the quality of life for patients. As a result, the medical device market is poised for significant growth, with opportunities for innovation and expansion across various segments. This growth trajectory underscores the importance of continued investment in research and development, as well as collaboration between healthcare providers, technology companies, and regulatory bodies to ensure the safe and effective use of medical devices in improving patient care.

| Report Metric | Details |

| Report Name | Professional Wearable Devices in Healthcare Market |

| Accounted market size in year | US$ 603 billion |

| CAGR | 5% |

| Base Year | year |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | Abbott, Alive Technologies, Philips, Garmin, Omron, Dräger, Polar Electro, GE Healthcare, Medtronic |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |