What is Global PD-1 and PDL-1 Inhibitors Market?

The Global PD-1 and PDL-1 Inhibitors Market is a rapidly evolving sector within the pharmaceutical industry, focusing on the development and distribution of drugs that target the programmed cell death protein 1 (PD-1) and its ligand, PD-L1. These inhibitors are a class of immunotherapy drugs designed to block the interaction between PD-1, a protein on the surface of immune cells, and PD-L1, a protein on the surface of cancer cells. By inhibiting this interaction, these drugs help to activate the immune system to recognize and attack cancer cells more effectively. The market for these inhibitors has been expanding due to their effectiveness in treating various types of cancers, including melanoma, non-small cell lung cancer, and renal cell carcinoma, among others. The increasing prevalence of cancer worldwide, coupled with advancements in biotechnology and a growing understanding of cancer immunology, has driven the demand for PD-1 and PD-L1 inhibitors. Pharmaceutical companies are investing heavily in research and development to enhance the efficacy and safety profiles of these drugs, leading to a competitive market landscape with numerous players striving to innovate and capture market share.

Pembrolizumab, Nivolumab, Atezolizumab, Durvalumab, Avelumab in the Global PD-1 and PDL-1 Inhibitors Market:

Pembrolizumab, Nivolumab, Atezolizumab, Durvalumab, and Avelumab are key players in the Global PD-1 and PDL-1 Inhibitors Market, each contributing uniquely to the treatment landscape of various cancers. Pembrolizumab, marketed under the brand name Keytruda, is a PD-1 inhibitor that has gained significant attention for its efficacy in treating melanoma, non-small cell lung cancer, and head and neck cancers. It works by blocking the PD-1 pathway, thereby enhancing the immune system's ability to fight cancer cells. Pembrolizumab has been a game-changer in oncology, offering hope to patients with advanced cancers and those who have not responded to traditional therapies. Nivolumab, known commercially as Opdivo, is another PD-1 inhibitor that has shown promise in treating a range of cancers, including melanoma, renal cell carcinoma, and Hodgkin lymphoma. Its mechanism of action is similar to Pembrolizumab, and it has been approved for use in several countries worldwide. Nivolumab's ability to improve survival rates in patients with advanced cancers has made it a cornerstone in cancer immunotherapy. Atezolizumab, marketed as Tecentriq, is a PD-L1 inhibitor that has been approved for the treatment of urothelial carcinoma and non-small cell lung cancer. By targeting PD-L1, Atezolizumab helps to restore the immune system's ability to detect and destroy cancer cells. Its approval for use in combination with chemotherapy has further expanded its application in oncology. Durvalumab, sold under the brand name Imfinzi, is another PD-L1 inhibitor that has been approved for the treatment of non-small cell lung cancer and bladder cancer. It is often used in combination with other therapies to enhance its effectiveness. Durvalumab's role in the maintenance treatment of certain cancers has been a significant advancement in prolonging patient survival. Avelumab, known as Bavencio, is a PD-L1 inhibitor that has been approved for the treatment of Merkel cell carcinoma and urothelial carcinoma. Its unique mechanism of action and ability to be used in combination with other therapies have made it a valuable addition to the cancer treatment arsenal. The development and approval of these drugs have revolutionized cancer treatment, offering new hope to patients and healthcare providers. The competitive landscape of the Global PD-1 and PDL-1 Inhibitors Market is characterized by ongoing research and development efforts, with companies striving to improve the efficacy and safety profiles of these drugs. As the understanding of cancer immunology continues to evolve, the potential for these inhibitors to treat a broader range of cancers is likely to expand, further driving market growth.

Stomach Cancer, Liver Cancer, Kidney Ccancer, Bladder Cancer, Cervical Cancer, Other in the Global PD-1 and PDL-1 Inhibitors Market:

The usage of Global PD-1 and PDL-1 Inhibitors Market in treating various cancers such as stomach, liver, kidney, bladder, cervical, and others has been transformative in oncology. In stomach cancer, these inhibitors have shown promise in improving survival rates for patients with advanced stages of the disease. By blocking the PD-1/PD-L1 pathway, these drugs enhance the immune system's ability to recognize and attack cancer cells, offering a new line of treatment for patients who have exhausted other options. In liver cancer, particularly hepatocellular carcinoma, PD-1 and PD-L1 inhibitors have been used to improve patient outcomes. The liver's unique immune environment makes it a challenging target for immunotherapy, but these inhibitors have demonstrated potential in overcoming these challenges and providing a viable treatment option. Kidney cancer, specifically renal cell carcinoma, has seen significant advancements with the use of PD-1 and PD-L1 inhibitors. These drugs have been effective in treating advanced stages of the disease, offering patients a chance at prolonged survival and improved quality of life. In bladder cancer, the use of these inhibitors has been a breakthrough, particularly for patients with metastatic disease. The ability of PD-1 and PD-L1 inhibitors to be used in combination with other therapies has further enhanced their effectiveness in treating this type of cancer. Cervical cancer, which has traditionally been treated with surgery, radiation, and chemotherapy, has also benefited from the introduction of PD-1 and PD-L1 inhibitors. These drugs offer a new treatment option for patients with advanced or recurrent disease, providing hope for improved outcomes. Beyond these specific cancers, PD-1 and PD-L1 inhibitors are being explored for their potential in treating a wide range of other cancers. The versatility of these drugs in targeting the immune system makes them a valuable tool in the fight against cancer. As research continues, the potential for these inhibitors to be used in combination with other therapies and for a broader range of cancers is likely to expand, offering new hope to patients and healthcare providers. The Global PD-1 and PDL-1 Inhibitors Market continues to grow as these drugs become an integral part of cancer treatment protocols worldwide.

Global PD-1 and PDL-1 Inhibitors Market Outlook:

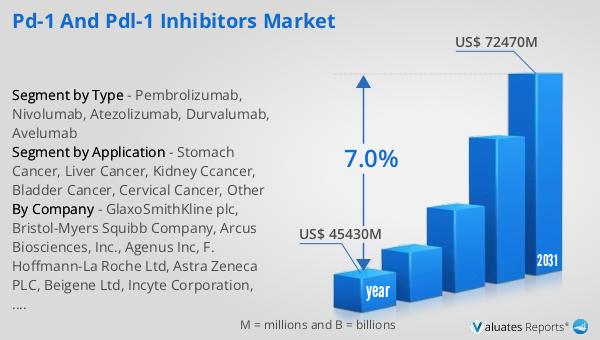

The global market for PD-1 and PD-L1 inhibitors was valued at approximately $45,430 million in 2024, with projections indicating a growth to around $72,470 million by 2031. This growth is expected to occur at a compound annual growth rate (CAGR) of 7.0% during the forecast period. North America stands out as the largest consumer of these inhibitors, accounting for nearly 60.40% of the consumption market share in 2019. This significant market share can be attributed to the region's advanced healthcare infrastructure, high prevalence of cancer, and strong focus on research and development in oncology. The increasing adoption of PD-1 and PD-L1 inhibitors in North America is driven by the growing demand for effective cancer treatments and the availability of advanced healthcare facilities. The region's robust pharmaceutical industry and supportive regulatory environment have also contributed to the widespread use of these inhibitors. As the market continues to expand, companies are investing in research and development to enhance the efficacy and safety profiles of these drugs, further driving market growth. The competitive landscape is characterized by numerous players striving to innovate and capture market share, leading to a dynamic and rapidly evolving market. The global market for PD-1 and PD-L1 inhibitors is poised for significant growth, driven by the increasing prevalence of cancer and advancements in biotechnology.

| Report Metric | Details |

| Report Name | PD-1 and PDL-1 Inhibitors Market |

| Accounted market size in year | US$ 45430 million |

| Forecasted market size in 2031 | US$ 72470 million |

| CAGR | 7.0% |

| Base Year | year |

| Forecasted years | 2025 - 2031 |

| Segment by Type |

|

| Segment by Application |

|

| Consumption by Region |

|

| By Company | GlaxoSmithKline plc, Bristol-Myers Squibb Company, Arcus Biosciences, Inc., Agenus Inc, F. Hoffmann-La Roche Ltd, Astra Zeneca PLC, Beigene Ltd, Incyte Corporation, Biocad, CStone Pharmaceuticals, Ono Pharmaceutical, Merck, Shanghai Junshi Bioscience Co. Ltd, Shanghai Henlius Biotech, Inc., Jiangsu HengRui Medicine Co., Ltd. |

| Forecast units | USD million in value |

| Report coverage | Revenue and volume forecast, company share, competitive landscape, growth factors and trends |